The World is a Stage

Like the absurdist play where two characters Vladimir and Estragon wait for a mysterious Godot who never shows up, investors in MLPs continue to wait for definitive answers to the "big questions" facing MLPs: when will interest rates rise and what will happen with future oil production and prices? We have been debating these questions at length, some of them for years. And like the vague apprehension that attends the precarious existence of Vladimir and Estragon, who look to Godot as the possible savior to their ills, the MLP market has slipped into an existential angst as it awaits its own Godot, clarity on these issues. Into this drama, arrives a new actor, a Greek, enmeshed in his own absurdist existence that momentarily commands the attention of the audience and takes the drama into an unexpected direction. How will it end?

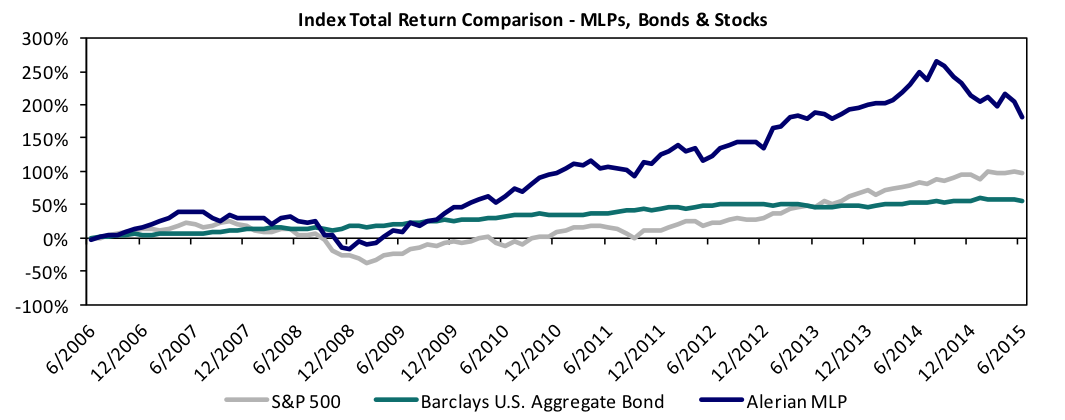

But unlike existential French drama, investors get a daily resolution in the markets of the price of uncertainty. Confusion about these issues facing MLPs and perhaps a rise in risk premia at the end of the quarter due to events in Greece, led the Alerian MLP Index to continue the retreat it began last year. During the quarter, the index fell 6.1% bringing its year-to-date decline to 11.0%. Coupled with the decline in the latter half of last year, the Alerian Index has fallen over 25% from its peak last August, qualifying this as a bona fide correction in the MLP market. This has hurt its comparative return versus U.S. stocks and bonds in the past quarter and trailing twelve months, however, for longer periods MLPs have significantly outperformed other asset classes as shown below.

*The inception of the Alerian MLP Index was June 1, 2006.

The indices shown are for informational purposes only and are not reflective of any investment. As it is not possible to invest in the indices, the data shown does not reflect or compare features of an actual investment, such as its objectives, costs and expenses, liquidity, safety, guarantees or insurance, fluctuation of principal or return, or tax features. Indices do not include fees or operating expenses and are not available for actual investment. Indices presented are representative of various broad base asset classes. They are unmanaged and shown for illustrative purposes only. Data from Alerian and Bloomberg. Past performance is not indicative of future results. The Alerian MLP Index does not represent the Eagle MLP Strategy Fund.

Q2 Performance

Weighing on the performance of MLPs and midstream energy infrastructure companies this quarter was continued uncertainty about the impact of lower energy prices and a robust amount of equity issuance. In this quarter healthy labor market statistics have pointed to the Fed ending its zero interest rate policy potentially in the fall, and longer term interest rates rose in anticipation of this. Uncertainty about the timing and extent of higher interest rates also weighed on the prospects for MLPs this quarter. While interest rates were somewhat higher in the quarter, MLPs remain attractive for yield oriented investors as the combination of lower prices and higher distributions led to a higher yield on MLPs. At quarter end, the yield of the Alerian MLP index stood at 6.44% vs. 2.35% for the 10 year U.S treasury. MLPs continued to increase their distributions in the quarter at a healthy rate, underscoring our long term contention that distribution increases were not much affected by lower energy prices. The weighted average distribution in the second quarter of the Alerian MLP Index was 7.5% above its level a year ago.

Past performance is not indicative of future results. The Alerian MLP Index does not represent the Eagle MLP Strategy Fund.

Absurdist French drama does hold lessons for investors in MLPs. Like the two who wait for a Godot that never comes, investors who wait for all questions to be resolved about MLPs may be disappointed. Once the current set of uncertainties is resolved, new ones are expected to arise and command our attention. When rates start to rise, questions will of how far and how fast may arise. If oil production starts to fall and prices rise, the questions again may be how much and how high. We continue to believe the real crux of the story of MLPs and midstream energy infrastructure companies that started many years ago is not finished; North America has significant needs for new midstream infrastructure investment that is many years from being sated. Accepting that there is always near term uncertainty, we view the recent sharp sell-off in the midstream segment as an attractive buying opportunity, with our long term evaluation of the total return prospects of MLPs and midstream energy infrastructure companies to be good, especially on a risk adjusted basis.

MLPs Continue to Build Out U.S. Midstream Infrastructure

Confounding bears, early in the second quarter midstream companies generally reported good first quarter financial results, distribution outlooks, and new project prospects. Kinder Morgan Inc. maintained their previous guidance of 10% distribution growth through 2020 and highlighted a project backlog of $15-18 billion of capital spending in various projects across North America. Enterprise Product Partners reconfirmed their plans to spend $2.5 billion this year and noted a project backlog of almost $7 billion through 2017. As part of that backlog, the company announced its plans to build an ethane export facility on the Texas Gulf Coast as well as increase capacity at its existing LPG export facility. Export focused projects are gaining more momentum as the abundant supply of natural gas liquids in North America needs increasing infrastructure support to get to market. Plains All American Pipeline Partners, known for their cautious approach, still reiterated distribution growth guidance of 7% for 2015 and outlined plans to spend almost $9 billion over the next 5 years on crude oil infrastructure. The management team highlighted on their call and subsequently at their analyst day that they are cautious on crude oil supply/demand fundamentals near-term but expect that longer term prices may trend higher as global demand continues to grow.

Other companies were also active in announcing new projects during the quarter. Energy Transfer Partners is working with independent producers in the Marcellus to increase its scale in the Northeast by building a processing plant, associated gathering, and pipe to support producer drilling activity. The company has stated that the $1.5 billion capital cost will be supported by long-term fee based agreements with expected start-up in mid-2017. Cheniere Energy announced its plans to increase capacity at its Corpus Christi liquefied natural gas export facility. While this was widely anticipated, the company also announced its intentions to develop two more mid-scale projects in partnership with another entity along the Louisiana coast. Sunoco Logistics formally announced its interest in the Dakota Access Pipeline project being built by Energy Transfer Partners. Sunoco will own 30% of the $5 billion pipeline that will transport crude oil from the Bakken shale to the Gulf Coast. In addition, the company stated its intentions to move forward with the Mariner East 2 project to transport natural gas liquids from the Marcellus/Utica producers to Marcus Hook, an export facility on the east coast. While the project is currently being sized for producer interest, management is leaving flexibility for meaningful expansion if the demand is there to support it. SemGroup Corporation will build crude oil and refined products pipelines for $500 million. The new pipelines are scheduled to be in service in the fourth quarter of 2016 and will support Motiva’s Louisiana refining complex. More importantly, the company believes that expansion opportunities exist around this build out.

We have discussed the importance of parent/sponsor relationships that certain MLPs have and how that contributes to sustained cash flow growth that is not necessarily predicated on the state of the commodity markets or available organic opportunities. During the quarter, Enbridge Inc. enacted the first part of its simplification strategy by transferring Canadian liquids pipelines and renewable energy assets to the Enbridge Income Fund for $30.4 billion. Enbridge Inc. has stated its intent to drop down its U.S. pipelines to Enbridge Energy Partners.

Shipping companies were also active in dropping down assets this quarter. Navios Maritime Midstream Partners acquired two crude carriers from a drop down by its parent Navios Maritime Acquisition Corp. for $100 million. This increases the partnership’s fleet by 50% to 6 vessels in total. The two ships are expected to support 10% distribution growth through 2016. GasLog Partners acquired 3 LNG carriers from its parent GasLog Ltd. for $483 million bringing its fleet size to 8 ships. The ships are operating under long-term contracts and expected to support 10% distribution growth for the MLP. At their combined analyst day earlier in the year, the two companies outlined a plan to own 40 ships in aggregate by 2017.

In addition to drop downs, mergers & acquisitions were active continuing the trend started in the first quarter. At the end of the quarter, a mega merger that would rival last year's Kinder Morgan transaction was proposed. Williams Companies received an unsolicited offer from Energy Transfer Equity to be acquired in an all stock deal valuing the company at $53.1 billion including liabilities. The offer from Energy Transfer Equity, however, is contingent on Williams Companies abandoning the process to acquire Williams Pipeline Partners (which the company had initiated earlier in the quarter). As it stands for the moment, the Williams Companies board of directors has rejected the initial offer from Energy Transfer Equity and has hired advisors to explore strategic alternatives. The ensuing tug of war that will now unfold is expected to take some time to play out as Energy Transfer Equity is very committed to closing a deal with Williams and the management of Williams is currently exploring other options. Williams Companies was a substantial position in the Fund during the quarter and the unsolicited offer from Energy Transfer Equity has lifted the stock significantly since the offer was made public.

A number of smaller acquisitions were announced where energy producers continue to shed midstream assets to raise funds in this stressed environment. Enterprise Product Partners bought $2.15 billion of gathering and processing assets from producers in the Eagle Ford. Hess Corp sold 50% of its midstream holdings located in the Bakken for $3 billion to privately held Global Infrastructure Partners. While the Hess Corp. assets did not go to an MLP, Global Infrastructure Partners is no stranger to the space and previously held an interest in Access Midstream Partners before they sold to Williams Pipeline Partners.

During the quarter, new equity capital raised for MLPs and related securities amounted to $7.2 billion versus $8.6 billion raised in the first quarter. In addition to a smattering of follow-ons and secondary’s, there were some very large IPOs. The general partner of EQT Midstream raised over $700 million in an IPO. The general partner is expected to grow its distribution at a very robust pace over the next five years as it stands to benefit from the large growth capital and existing inventory of assets to be acquired by EQT Midstream from its producer sponsor EQT Corp. Another large general partner IPO occurred during the quarter when the general partner of Tall Grass Energy Partners raised close to $1.4 billion. Similar to the general partner of EQT, Tall Grass Energy GP is expected to benefit from large scale organic projects driving distribution growth at the underlying MLP. Black Stone Minerals LP raised more than $400 million in the public markets for their mineral royalty interests business. PennTex Midstream Partners raised $225 million in an IPO to support its gathering and processing MLP with assets in northern Louisiana. The company is closely supported by its producer sponsor Memorial Resource Development Company as they ramp up production in the Terryville field. Rising interest rates did not impact the ability of MLP companies to raise debt capital during the quarter. Companies raised an estimated $12 billion including Energy Transfer Partners who raised $3 billion of new debt capital at varying rates and maturities.

Fund flows as measured by open-end/closed-end funds, ETFs, and ETNs declined quarter over quarter. We estimate that products saw inflows of $1.7 billion in the first quarter of the year versus $1.3 billion in the second quarter. Inflows year-to-date have been well below the 2014 average of $5.1 billion per quarter. June was a particularly slow month for inflows with less than $100 million of new money added to products during the month.

Recently we have seen many companies with renewable power generation assets (mainly wind and solar) adopt a model very similar to the MLP’s in terms of payout of cash flows and growth through acquisitions. These companies have adopted the moniker “YieldCo’s”. First Solar and Sunpower together created a portfolio of solar power generation assets. They raised proceeds of $420 million for this venture called 8point3 Energy Partners LP. They expect to further drop down assets into this YieldCo vehicle to support dividend growth going forward. We believe that this asset class will continue to grow as more renewable assets are built and existing assets pursue this type of structure. The team is dedicating resources to take advantage of what could be more opportunities in this space in the foreseeable future.

IRS Clarifies Rules; EPA Presents "Fracking" Report

Last quarter we reported that the IRS ended their moratorium on Private Letter Rulings for MLPs and in late May, the IRS issued specific guidelines for what they believe to be “qualifying income”. (In order to maintain status as a MLP, a company must have 90% of its income derived from qualifying activities.) For the most part, the proposed regulations are in-line with what we were expecting. Assets supporting the distribution and recycling of water, compression, and wholesale fuel distribution will still be considered qualifying income. However, petrochemical assets have been proposed for exclusion from the qualifying assets definition. These assets include steam crackers which covert ethane to ethylene and propane dehydrogenation units which covert propane to propylene. There is a 90 day review period from May when the guidelines were announced for companies to make comments and provide feedback to the IRS. Even still if these rules stand, companies that have received PLR’s for these assets will be grandfathered for a 10 year period. Nonetheless, Eagle’s portfolios did not have any material negative effects as a result of these announcements and in fact the clarification surrounding the water assets will help certain companies in our portfolio.

The quarter also included some meaningful developments on “fracking” regulations and their environmental impact. In a win for energy producers, the EPA concluded a 4-year study which stated that it could not find any evidence of systematic impacts from "fracking" on drinking water. Many states including New York have outright banned fracking on this basis. While this report will be debated, it should help existing energy friendly states to continue drilling activity with minimal disruption. In May, Texas Governor Greg Abbott signed into law legislation to prohibit municipalities from instituting bans on fracking. Again, this is an example representative of currently energy friendly states maintaining their ability to effectively regulate the process without instituting laws to impede the industry.

Long Term Outlook: Positive

We continue to be positive on the outlook for total returns for MLPs and midstream energy infrastructure companies. Valuations, after the 25%+ decline in the Index since August of last year, are much more attractive today, in our opinion. Relative valuations to other asset classes have also become more attractive despite the rise in bond yields this quarter as spreads of MLP yields versus Treasuries, REITS, corporate bonds, and high yield bonds have widened out to historically large levels. The yield of the Alerian MLP Index is now approximately 6.4%. Although we may see select companies being more conservative with their payouts this year and reduce their distribution growth rates, we still expect high single digit growth from our portfolio of companies, and indeed saw that in the first quarter. Combined with current distribution yields, we believe MLPs and midstream energy infrastructure companies still have the potential for attractive total returns.

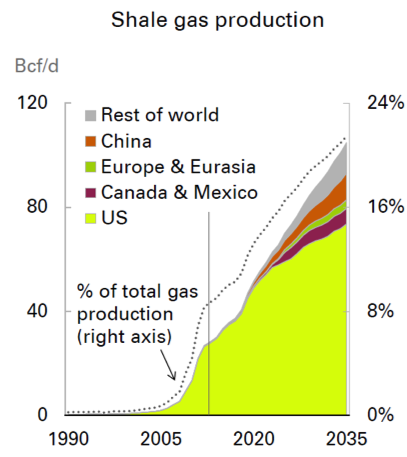

Crude oil supply may be outpacing global demand for the moment, however, recent statistics from the Department of Energy are showing a strong summer driving season in terms of vehicle miles traveled and gasoline demand. This is helping to drive refining utilization higher as we work through elevated crude oil inventories in North America in the short term. While we talked about the global shift to use natural gas in electricity and power generation in last quarter’s update, we believe it is still a relevant reminder for MLP investors and one of the brighter aspects of the longer-term positives for the sector. BP sees significant growth in global demand for natural gas in the next decades; to meet this demand, it forecasts that U.S. shale gas production growth needs to rise an average of 4.5% per year for the next 20 years.

Source: BP Energy Outlook 2035

For oil and natural gas liquids, BP expects world demand to grow from approximately 92 million barrels per day (bpd) today to 111 million bpd by 2035; of this 19 million bpd increase, BP sees almost 50% or 9 million bpd coming from North America: 6 million bpd from the U.S. and 3 million bpd from Canada. Needless to say, if these forecasts are anywhere close to the mark, the need for new midstream infrastructure in North America is a multi-decade story.

David Chiaro

David Chiaro is Co-Head of MLP Strategy for Eagle Global Advisors, LLC

Co-Advisor of the Eagle MLP Strategy Fund

Disclosures:

Investors should carefully consider the investment objectives, risks, charges and expenses of the Eagle MLP Strategy Fund. This and other important information about the Fund is contained in the prospectus, which can be obtained by calling 1-888-868-9501 or visiting www.eaglemlpfund.com. The prospectus should be read carefully before investing. The Eagle MLP Strategy Fund is distributed by Northern Lights Distributors, LLC member FINRA/SIPC. This is an actively managed dynamic portfolio. There is no guarantee that any investment (or this investment) will achieve its objectives, goals, generate positive returns, or avoid losses. The information provided should not be considered tax advice. Please consult your tax advisor for further information. Eagle Global Advisors, Princeton Fund Advisors, LLC and Northern Lights Distributors, LLC are not affiliated.

A master limited partnership (MLP) is a limited partnership that is publicly traded on a securities exchange. It combines the tax benefits of a limited partnership with the liquidity of publicly traded securities. To qualify for MLP status, a partnership must generate at least 90 percent of its income from what the Internal Revenue Service (IRS) deems "qualifying" sources, generally relating to the production, processing or transportation of natural resources, such as oil and natural gas.

The Alerian MLP Index is a composite of the 50 most prominent energy master limited partnerships calculated by Standard & Poor's using a float-adjusted market capitalization methodology.

A real estate investment trust (REIT) is a security that sells like a stock on the major exchanges and invests in real estate directly, either through properties or mortgages. REITs receive special tax considerations and typically offer investors a regular distribution, as well as a highly liquid method of investing in real estate.

Risk Factors:

Credit Risk: There is a risk that note issuers will not make payments on securities held by the Fund, resulting in losses to the Fund. In addition, the credit quality of securities held by the Fund may be lowered if an issuer’s financial condition changes.

Distribution Policy Risk: The Fund’s distribution policy is not designed to guarantee distributions that equal a fixed percentage of the Fund’s current net asset value per share. Shareholders receiving periodic payments from the Fund may be under the impression that they are receiving net profits. However, all or a portion of a distribution may consist of a return of capital (i.e. from your original investment). Shareholders should not assume that the source of a distribution from the Fund is net profit. Shareholders should note that return of capital will reduce the tax basis of their shares and potentially increase the taxable gain, if any, upon disposition of their shares.

ETN Risk: ETNs are subject to administrative and other expenses, which will be indirectly paid by the Fund. Each ETN is subject to specific risks, depending on the nature of the ETN. ETNs are subject to default risks. Foreign Investment Risk: Investing in notes of foreign issuers involves risks not typically associated with U.S. investments, including adverse political, social and economic developments, less liquidity, greater volatility, less developed or less efficient trading markets, political instability and differing auditing and legal standards.

Interest Rate Risk: Typically, a rise in interest rates can cause a decline in the value of notes and MLPs owned by the Fund.

Liquidity Risk: Liquidity risk exists when particular investments of the Fund would be difficult to purchase or sell, possibly preventing the Fund from selling such illiquid securities at an advantageous time or price, or possibly requiring the Fund to dispose of other investments at unfavorable times or prices in order to satisfy its obligations.

Management Risk: Eagle’s judgments about the attractiveness, value and potential appreciation of particular asset classes and securities in which the Fund invests may prove to be incorrect and may not produce the desired results. Additionally, Princeton’s judgments about the potential performance of the Fund’s investment portfolio, within the Fund’s investment policies and risk parameters, may prove incorrect and may not produce the desired results.

Market Risk: Overall securities market risks may affect the value of individual instruments in which the Fund invests. Factors such as domestic and foreign economic growth and market conditions, interest rate levels, and political events affect the securities markets.

MLP Risk: Investments in MLPs involve risks different from those of investing in common stock including risks related to limited control and limited rights to vote on matters affecting the MLP, risks related to potential conflicts of interest between the MLP and the MLP’s general partner, cash flow risks, dilution risks and risks related to the general partner’s limited call right. MLPs are generally considered interest-rate sensitive investments. During periods of interest rate volatility, these investments may not provide attractive returns. Depending on the state of interest rates in general, the use of MLPs could enhance or harm the overall performance of the Fund.

MLP Tax Risk: MLPs, typically, do not pay U.S. federal income tax at the partnership level. Instead, each partner is allocated a share of the partnership’s income, gains, losses, deductions and expenses. A change in current tax law or in the underlying business mix of a given MLP could result in an MLP being treated as a corporation for U.S. federal income tax purposes, which would result in such MLP being required to pay U.S. federal income tax on its taxable income. The classification of an MLP as a corporation for U.S. federal income tax purposes would have the effect of reducing the amount of cash available for distribution by the MLP. Thus, if any of the MLPs owned by the Fund were treated as corporations for U.S. federal income tax purposes, it could result in a reduction of the value of your investment in the Fund and lower income, as compared to an MLP that is not taxed as a corporation.

Energy Related Risk: The Fund focuses its investments in the energy infrastructure sector, through MLP securities. Because of its focus in this sector, the performance of the Fund is tied closely to and affected by developments in the energy sector, such as the possibility that government regulation will negatively impact companies in this sector. Energy infrastructure entities are subject to the risks specific to the industry they serve including, but not limited to, the following: Fluctuations in commodity prices; Reduced volumes of natural gas or other energy commodities available for transporting, processing, storing or distributing; New construction risk and acquisition risk which can limit potential growth; A sustained reduced demand for crude oil, natural gas and refined petroleum products resulting from a recession or an increase in market price or higher taxes; Depletion of the natural gas reserves or other commodities if not replaced; Changes in the regulatory environment; Extreme weather; Rising interest rates which could result in a higher cost of capital and drive investors into other investment opportunities; and Threats of attack by terrorists.

Non-Diversification Risk: As a non-diversified fund, the Fund may invest more than 5% of its total assets in the securities of one or more issuers. Small and Medium Capitalization Company Risk: The value of a small or medium capitalization company securities may be subject to more abrupt or erratic market movements than those of larger, more established companies or the market averages in general. Structured Note Risk: MLP–related structured notes involve tracking risk, issuer default risk and may involve leverage risk. Mutual Funds involve risk including possible loss of principal.