Why International Now?

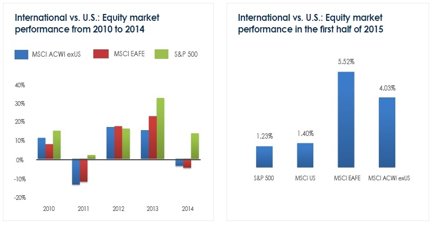

At the end of 2014, “why international?” was the prevailing investor sentiment. After all, foreign stocks had lagged U.S. equities yet again, underperforming four out of the five years between 2010 and 2014. The consensus outlook was that U.S. markets would outperform their foreign peers in any case, and so, would it really serve any purpose to hold international equities in a portfolio? Many investors followed the crowd.

Then the tide turned. With foreign equity indices starting to climb, the first half of this year saw a rush to re-enter international markets, and eventually, foreign indices more than tripled the return of the S&P 500 between January and June. Portfolios that were still underweight international stocks most likely failed to fully capture this market movement, yet again underlining the attractiveness of holding globally diversified portfolios even when the environment is uncertain.

And now, given the events in China and Greece, the wisdom of remaining exposed to international markets is once again being questioned. Region or sector reallocations driven by market sentiment

Long-Term Growth Potential Appears More Attractive for Overseas Economies

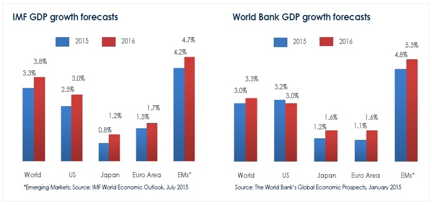

While the World Bank and the IMF have estimated that the U.S. economy will likely grow faster than all its large developed market peers over the medium term , the pace of U.S. GDP expansion is projected to be slower than aggregate global growth. This is due to a fairly simple equation — developing countries are a sizeable component of the global economy today and these economies are forecast to grow faster than advanced economies. Indeed, emerging economies now account for more than 50 percent of global GDP and nearly three-quarters of global growth.

There are several factors at play which will most likely strengthen these trends over the long term. For one, the larger emerging economies, such as China and India, have a middle class that is not just growing rapidly but increasing its earning and spending power. What’s more, emerging economies have a significant advantage over developed countries in the form of younger populations. Many developing countries are also progressively freeing up their economies and removing controls, which is creating even better growth opportunities for their industries.

Nevertheless, it may be argued that economic expansion and stock market returns are not always perfectly correlated. While this is true, it cannot be denied that across the globe, nearly a third of the companies that have a market capitalization of over $1 billion are based in the emerging economies. Robust growth in these countries typically provides more opportunities for financially healthy and prudently managed businesses. Sustained domestic growth also helps firms build economies of scale and financial resources, which in turn enables these companies to seek opportunities in overseas markets as well.

Current Valuations Appear More Appealing Outside the U.S.

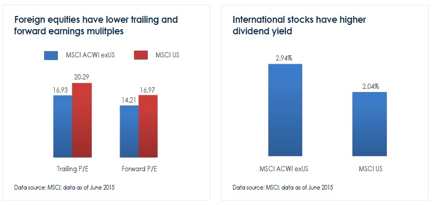

Although international equity prices have been in an uptrend since the beginning of this year, we believe that foreign stocks continue to appear more attractively valued compared to their peers in the U.S. market. For instance, as of June, international stocks had not just lower trailing and forward earnings multiples but also higher dividend yields compared to U.S. equities. In our opinion, the current relative attractiveness and higher yields of foreign stocks may benefit investors in two ways — offer a larger upside potential as well as provide downward protection in the event of any unexpected deterioration in market sentiment.

The Downside in Chinese Markets Presents Opportunities, and Concerns about Other Foreign Markets are Easing

We see the current downside in the Chinese markets as an opportunity to seek attractive long-term investment prospects. The Chinese indices have fallen after a phenomenally strong and swift uptrend over the past year and, notably, they are still higher than they were at the beginning of this year. Further, the country’s economic fundamentals do not appear to have undergone any dramatic change to warrant a market crash. China’s GDP growth rate has moderated from its record highs while the country makes a complex transition from an export-driven growth model to one that is centered on domestic consumption. There are signs that the Chinese economy is on track to achieve this transition and settle at a more sustainable pace of growth in the long term.

We believe that the market decline is unlikely to affect the overall economy in a significant way because economic activity in China is not generally linked to financial asset prices as much as it is in the developed markets. Equity accounts for a significantly smaller portion of financing for the real economy and makes up only a small part of Chinese household assets. Encouragingly, the country’s banking sector, which is largely government owned, is seemingly holding up well.

Given the combination of factors working in its favor — record low interest rates, a depreciated euro and depressed oil prices — the Euro-zone recovery finally appears to have become more robust and broad-based. Between January and March, Germany, France, Italy and Spain all recorded growth simultaneously for the first time in many quarters. Encouragingly, the preliminary agreement to offer additional financial support to Greece showcased European leaders’ resolve to preserve the economic union and to prevent further crises. What’s more, the European Central Bank’s quantitative easing program is serving its primary purpose — that of suppressing deflationary conditions and improving business and consumer confidence.

With the Japanese central bank maintaining its massive stimulus program, private consumption has been growing steadily over the past few quarters. In fact, between January and March, the Japanese economy expanded at its fastest pace in a year on the back of only a modest increase in private consumption. Private consumption, which accounts for 60 percent of the Japanese economy, was hit hard by a sales tax hike last year. So, if the current uptrend in consumption continues, Japan is likely to gain further momentum.

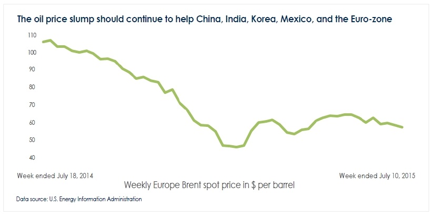

India and Korea, along with China, are expected to continue seeing a steady growth in domestic consumption due to lower oil prices. In fact, as oil prices remain depressed, export-driven countries like China and Mexico should also gain from consumption growth in the U.S. and other developed economies. What’s more, countries such as India that import a significant portion of their energy requirements now have a better current account position due to reduced import costs, which has eased investor worries about the large current account deficits of these nations.

Fears about the Potential Impact of Fed Rate Hike on Emerging Markets are Likely Unwarranted

As far as the emerging markets are concerned, many investors fear a repeat of the 2013 ‘taper tantrum’ scenario when the U.S. Federal Reserve eventually begins hiking rates. We believe that these fears are unwarranted because unlike the situation in 2013, the Fed has declared that this time the hikes would be gradual, conveyed to the markets well in advance, and spread over several years. Besides, investors have already depressed several emerging markets currencies in anticipation of the rate hikes.

In fact, the U.S. Dollar’s strength against emerging market currencies is another lingering worry for investors. They feel that, even if emerging markets do well, the dollar returns from these markets will be unattractive. Indeed, this argument is valid, but it is also true that given the steady depreciation of these currencies vis-à-vis the dollar, the risk of further steep declines appears limited. What’s more, owing to their depreciated currencies, emerging markets equities are much cheaper now, making it easier for investors to consider increasing their allocation to these markets. In addition, several overseas firms that have a significant market in the U.S. and that compete with U.S.-based companies are now in a position to garner higher profits when their dollar revenues are converted into their home currencies.

Conversely, a rise in interest rates could be bad news for U.S. firms that have been benefiting from being able to borrow very cheaply in a low-interest-rate environment. Even worse for these companies, the strong U.S. Dollar is likely making it more difficult for them to compete in the global marketplace. A strong dollar is also expected to hurt the profits of U.S. firms that operate abroad, as their overseas incomes would be worth less when converted from other international currencies.

To sum up, we feel that three common investor biases have played out amid the volatility in global equity markets in recent years — the tendency to prefer the perceived safety of domestic assets over relatively less familiar international securities, the inclination to use past returns as an indicator of future performance and the propensity to base investment decisions on the prevailing sentiment.

But historically, no single market has stayed at the top consistently and over the long term globally diversified portfolios exposed to a wider set of opportunities typically succeed in not just absorbing market volatility but also providing relatively consistent returns. We believe that this time-tested trend, combined with the better long-term growth prospects of emerging economies as well as the relatively attractive valuations overseas, make a compelling case for international equities NOW.

This article is for informational purposes only. This article is not intended to provide tax, legal, insurance or other investment advice. Unless otherwise specified, you are solely responsible for determining whether any investment, security or other product or service is appropriate for you based on your personal investment objectives and financial situation. You should consult an attorney or tax professional regarding your specific legal or tax situation. The information contained in this article does not, in any way, constitute investment advice and should not be considered a recommendation to buy or sell any security discussed herein. It should not be assumed that any investment will be profitable or will equal the performance of any security mentioned herein. Thomas White International, Ltd, may, from time to time, have a position or interest in, or may buy, sell or otherwise transact in, or with respect to, a particular security, issuer or market on our own behalf or on behalf of a client account.

FORWARD LOOKING STATEMENTS

Certain statements made in this article may be forward looking. Actual future results or occurrences may differ significantly from those anticipated in any forward looking statements due to numerous factors. Thomas White International, Ltd. undertakes no responsibility to update publicly or revise any forward looking statements.