Mid-Year Outlook: Global Economy Likely to Withstand China, Greece

In this Commentary

We believe:

» The U.S. and global economies will expand during 2H 2015, albeit at a subdued pace

» A hard landing for China’s economy is a less likely outcome

» Beginning in late 2015, the Federal Reserve is likely to embark on a slow and shallow path for raising short-term interest rates

» Globally, equities and convertible securities should perform well, particularly growth-oriented securities

The global markets and economy should be able to move higher for the remainder of the year, with accommodative monetary policy and well-contained inflation providing tailwinds. The U.S. looks set to extend its not-too-hot, not-too-cold recovery, while Japan is benefiting from stimulus and pro-market reforms. Although economic conditions in Europe remain fragile and uneven, growth looks to be accelerating overall, and we believe the European Union has the tools to prevent a broader Europe contagion should the Greek bailout resolution fall apart. Meanwhile, economic reforms and policy shifts in many emerging markets are contributing to improved growth prospects and investment opportunities, but these transitions are long term and challenging, calling for a selective and risk-managed approach. While China has been the focus of recent scrutiny, we believe a hard landing is a less likely scenario, given the arsenal of stimulative tools that could be deployed by the Chinese government.

As we look to the second half of the year, we expect the markets to continue to move away from the risk-on, risk-off tendencies and to shift toward growth. We expect the Federal Reserve to begin its long-telegraphed rate rise by year end. Reflecting this view, we remain constructive on growth equities, convertible securities, and select liquid alternative strategies. Markets are likely to remain volatile due to continued political turbulence in the euro zone and uncertainty surrounding China.

Market Review

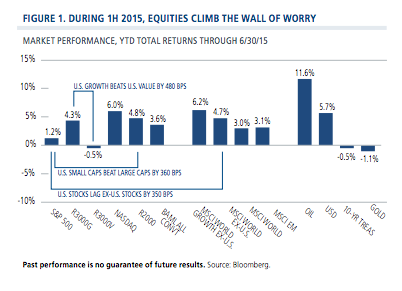

During the first half of the year, non-U.S. equities outperformed the S&P 500 Index, and growth outperformed value globally (Figure 1, page 2). Although markets welcomed the European Central Bank’s decision to move ahead with quantitative easing, familiar uncertainties dogged sentiment: euro zone debts, slower global growth woes, volatile energy prices, and the Fed’s timeline for embarking on rate increases. As the second quarter came to a close, concerns about a Greek departure from the euro zone and China’s market meltdown put investors on higher alert.

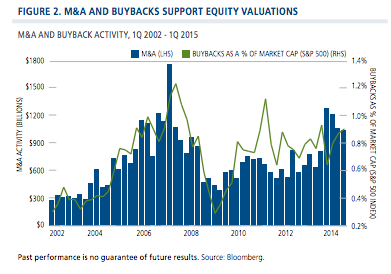

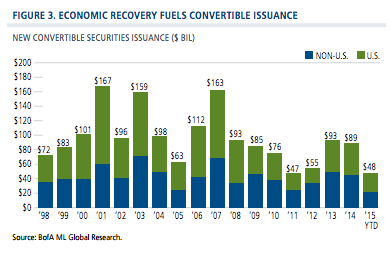

Through the first half of the year, capital market activity remained strong in many areas. The buy-rather-thanbuild investment trend remains intact, as historically wide spreads between earnings yields and after-tax borrowing costs have encouraged record share repurchase and merger-and-acquisition activities (Figure 2), while also supporting equity market valuations. Convertible market issuance has maintained a brisk pace in a growing global economy (Figure 3).

Global high yield issuance has fallen modestly versus yearto-date issuance of a year ago but remains healthy. We believe this drop-off in issuance is attributable to potential issuers’ reduced need for capital, as many companies have already taken advantage of low rates to extend their maturity profiles. Bank loan activity has dropped off more significantly; here again, we believe there is less demand from potential borrowers. Leveraged buyout activity has also been less robust than at comparable points in past cycles, but this is likely the result of the high multiples in the equity market.

Outlook

Consensus estimates for global economic growth for 2015 have come down, and we share the view that the pace of acceleration is likely to slow. Still, we expect the global economy will continue to expand during the second half of the year, albeit at a subdued pace. The most significant potential risks to our outlook for growth include: the Federal Reserve making a policy mistake by raising rates too aggressively and not being able to backtrack if deflationary forces persist, a hard landing for China, and a failure of quantitative easing in Europe to boost GDP and stem deflationary pressures. At this point, we believe it is more likely than not that these risks can be avoided, and accordingly, equities and convertible securities can continue to advance.

United States

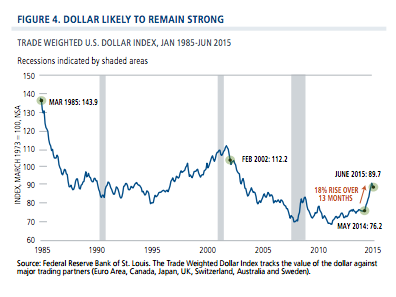

We believe the U.S. will also expand modestly during the second half of the year, with GDP accelerating from the first half of the year. Employment data has been encouraging, corporate earnings growth is healthy, and inflationary pressures are contained. We expect the U.S. dollar will be range-bound through the remainder of the year (Figure 4), with the potential to move slightly higher due to divergent monetary policies.

The energy sector hindered the economy during the first half of 2015, but oil prices have stabilized from their more volatile levels of earlier this year, and the amount of rigs in service continues to decline. Prices will likely be rangebound through year end, as well. The shale industry, rather than OPEC, is now the marginal producer of oil in the global markets. Because of the shale industry’s shorter production cycles, as oil prices rise, shale producers can quickly ramp up capital spending (i.e., production), keeping a cap on oil prices.

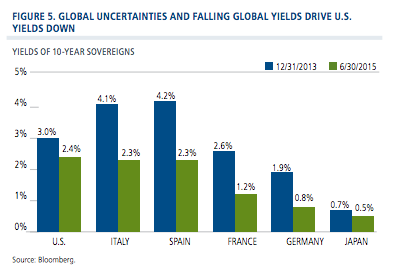

With continued quantitative easing through the balance of the year in the euro zone and Japan, we expect global sovereign yields will remain low, suppressing the 10-year Treasury yield (Figure 5). We believe the Treasury will generally stay in a 2.0% to 2.5% range through year end. If Greece cannot meet the deadlines put forth by its creditors under the proposed bailout plan or if market participants’ view of China becomes more pessimistic, the markets could swing back to a risk-off phase, bringing the yield range back down below 2.0%. Conversely, if global growth and inflationary pressures increase in the second half of the year, 10-year yields could inch back above 2.5%.

While U.S. economic data is favorable on the whole, the Federal Reserve’s timeline for raising rates will also reflect its view of global economic conditions, which remain lackluster. We believe the Fed will begin raising rates before year end, provided that job gains maintain their current pace and absent any acute geopolitical shocks. As noted, we believe that a Fed policy mistake is one of the greatest potential threats to the global economy, although this is not the outcome we anticipate. When increases begin, we expect a more measured pace with intermittent increases rather than the steady rate increases of the Greenspan-led Fed in the early 2000s, consistent with the current Fed leadership’s commitment to a data-driven approach, combined with the Fed’s intent to limit the rise in the U.S. dollar.

Opportunities in the U.S. Markets. We see continued upside in U.S. equities. Although a strong dollar has had a negative impact on 2015 estimated guidance, we expect S&P 500 earnings growth of 5% to 6% for 2016. As we have discussed in the past, the wide spreads between equity yields and borrowing costs should fuel a continuation of the record buyback and merger-andacquisition activity, providing support to equity valuations.

The earnings yields of equities remain extremely attractive relative to U.S. Treasury bond yields. At +370 basis points, the current spread between S&P 500 earnings yields (6.1% on forward 2016 estimates) and a 10-year Treasury yield of 2.4% places equity valuations in the cheapest third since 1950, based on data from Empirical Research.

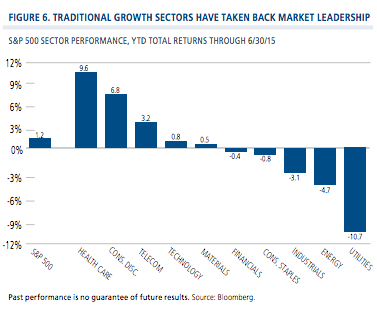

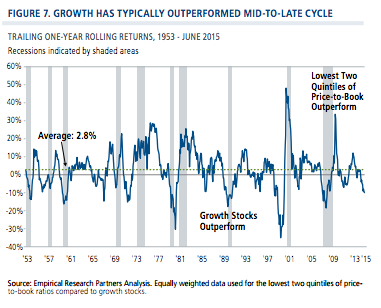

We maintain a particularly constructive outlook on growth stocks. During the first half of 2015, markets rotated to growth sectors (Figure 6), and we believe this rotation has more room to run. We expect growth stocks will continue to outperform value stocks, given narrow valuation spreads, high relative cash flow returns, and a high level of innovation across sectors. Additionally, in our view, the current economic cycle may extend for several more years, and growth has historically outperformed in mid-tolate-cycle periods (Figure 7). In this environment, we are maintaining an emphasis on secular growth companies, including overweights to information technology, health care, and consumer discretionary, while underweighting defensive areas of the market, such as consumer staples, utilities, and telecommunication services.

Europe

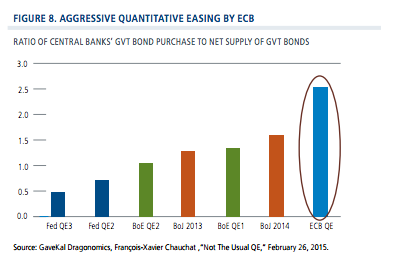

The economic recovery remains fragile and we expect continued volatility over the next several months. We may see pronounced market dislocations due to concerns, including not only those centered on Greece, but also elsewhere, such as Russia. Nonetheless, we believe a number of factors can support core Europe over the next nine to 12 months, including the liquidity provided by the ECB (Figure 8), reasonable valuations, and stabilizing-to-improving fundamentals. To capitalize on these cyclical tailwinds, we have sought to identify companies that are beneficiaries of QE (such as asset reflation and exporters). We have also maintained our focus on secular growth opportunities throughout the region.

The growing focus on the political divide in the euro zone has contributed to rising apprehension about the longterm sustainability of a single currency union. We also view the emphasis on monetary policy, rather than fiscal policy, as contributing to long-term growth headwinds. However, even if Greece fails to meet the conditions put before it—whether over these next weeks or in the years to come—the probability of an economic or market contagion is far less than in years past.

Compared with just a few years ago, the euro zone is in a much better position to contain Greece’s economic woes. The total private investor and bank exposure to Greece has fallen to €34 billion versus nearly €250 billion in 2012. The ECB has more firepower and a range of tools at its disposal, including quantitative easing, outright monetary transactions (OMT) and targeted long-term refinancing operations (LTROs). Meanwhile, countries like Spain, Portugal, Ireland and Italy have made progress on austerity and fiscal reform measures and are now starting to see economic green shoots. The euro zone’s economy has also benefited in recent quarters from weaker commodity prices, a weaker euro, and improved liquidity conditions.

Japan

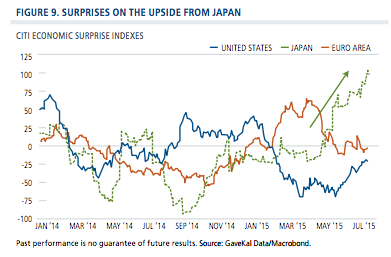

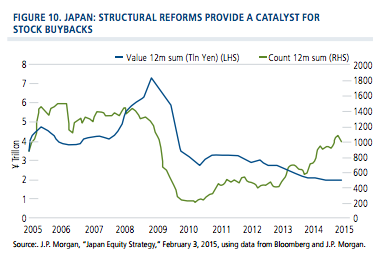

Although Japanese economic data remains mixed, activity continues to surprise on the upside (Figure 9), with the weak yen supporting exports and overseas corporate profits. As we discussed in our recent blog, “Japan at an Inflection Point,” we are particularly optimistic about trends in corporate governance, including a focus on increased shareholder transparency and a pickup in stock buyback activity (Figure 10, page 6). Japan’s growing ties with the U.S. are also positive, reflecting U.S. vested interest in a strong Japan to counter the growing geopolitical reach of China (not unlike the U.S.–European partnership forged following WWII). At the same time, data increasingly suggests Japan is well positioned to benefit from Chinese tourism and related consumption.

Japanese equities have outperformed on a relative basis year to date, and while valuations look comparatively less attractive as a result, we still see significant upside in many bottom-up opportunities among companies that are allocating capital more efficiently for the first time in several decades. Equity purchases by the Government Pension Investment Fund should provide continued support to Japanese stocks, as should increased participation from smaller public funds. Looking longerterm, we are closely monitoring the shift from domestic household saving to equity investing, which could provide an even more powerful tailwind. Japanese households have approximately $7 trillion in savings deposits—nearly one-and-a-half times the size of the domestic equity market. (For perspective, households in Japan have more than 50% of their assets in deposits, compared to 35% in Europe and less than 10% in the U.S.)

Emerging Markets

Many investors remain concerned that when the Fed begins raising interest rates, a repeat of the “taper tantrum” will inevitably follow. While there will likely be volatility, we believe emerging markets can perform well, provided rates rise because global growth is improving. (Emerging markets have historically provided higherbeta exposure to global economic growth.) Higher U.S. rates could negatively impact a carry trade that has provided capital to emerging markets by putting pressure on liquidity and valuations, but a number of emerging markets are arguably better positioned today. The taper scare of 2013 provided several emerging markets with the impetus to begin fiscal and economic reforms, and many have been successful in positioning their economies for an eventual rise in global rates. Increased currency reserves and lower inflationary pressures (including lower oil prices) have equipped several emerging markets with more monetary flexibility to manage short-term dislocations in domestic liquidity.

We also would note the 2013 taper tantrum was a “shock” to the financial markets, as investors did not know the timing or magnitude of future Fed policy. With the Fed now telegraphing a slow and shallow rate path, the markets should be better prepared for an eventual change in monetary conditions. Finally, with both the Bank of Japan and the ECB engaged in aggressive quantitative easing, the carry trade is likely more diversified and less dependent on low U.S. rates.

China. Although the Chinese economy is decelerating and near-term negative momentum is a concern, China is still growing at a faster rate than most of the world. The policy backdrop is positive, with accommodative monetary policy and government policies supporting asset reflation. Of course, we are closely watching what happens in the wake of the recent sell-off in Chinese equities. At this point, we believe a hard landing is a lower probability outcome. The Chinese government has many tools at its disposal to support near-term stability and economic growth, and we view it as a favorable sign that the People’s Bank of China did not need to step in during the market sell-off. As we have discussed in recent blogs (including “Perspectives on China’s Market Meltdown: Long-Term Opportunity Remains”), the Chinese government is fully committed to expanding its economic and military influence across Asia and globally. It is also dedicated to transitioning the Chinese economy from investment-led growth to consumption-led growth and from the public sector to the private sector. Also, while recent equity losses have been very steep, the net wealth created in the Chinese equity market over the past year remains positive.

Reflecting this view, we continue to invest in Chinese and Hong Kong companies with growing franchises that are selling at reasonable valuations. While there are pockets of overvaluation in segments of the market (particularly those traded primarily by local investors), the multiples of other Chinese stocks are far more palatable—even attractive— when compared to our long-term earnings growth and sales estimates. Valuations are quite compelling for a number of stocks in which non-local investors participate, such as shares traded on the Hong Kong exchange and other select larger-cap issues.

Fragile Five. We are closely monitoring our exposure to the “fragile five” economies (Brazil, India, South Africa, Turkey, Indonesia). All are highly dependent on capital flows given their fiscal and current account deficits, but there are important fundamental differences that influence our country-specific outlooks and positioning.

We continue to favor India given its ongoing progress in economic reforms and its improved monetary flexibility. The market correction in India this spring can be attributed to a combination of factors: market expectations that got ahead of fundamentals, a pause in policy momentum, and growing concerns regarding the monsoon season and other technical factors. Looking forward, we see a number of positives. The monsoon season does not appear to be as bad as feared, we see the reform agenda getting back on track during the second half of 2015, and we are hopeful about a ramp up in government investment spending.

The Philippines. We remain positive on the Philippines as the strong business process outsourcing industry, U.S. dollar remittances and lower commodity prices should continue to support domestic liquidity. We also expect the election cycle to drive a more meaningful ramp up in pro-growth policies.

Navigating the Headwinds of Rising Rates

While we believe the case remains strong for U.S. and non-U.S. growth equities, our outlook for traditional fixed income securities is far more cautious. Convertible securities and select alternative strategies are likely to prove more effective than traditional fixed income investments in this environment, given our expectation that the Fed moves to raise short-term rates before the year is out.

Convertible Securities. We maintain a constructive outlook for convertibles. We expect issuance to remain healthy, supported by economic growth. In our view, the benefits of convertibles may become even more pronounced when interest rates move higher. As we have discussed in the past, convertible securities have been less vulnerable to rising interest rates than traditional fixed-income securities. (For more, see our post, “Convertibles Address Multiple Investor Needs”). Additionally, convertibles have tended to perform well during periods of upwardly rising but volatile equity markets. We believe convertible securities with a balanced blend of equity sensitivity and credit sensitivity will be better positioned in this environment. While many of the most equity-sensitive convertibles have performed well of late, we remain concerned about their potential downside.

Alternatives. We also hold a favorable outlook for select alternative strategies, such as market neutral and long/short strategies. For those concerned about traditional fixed income securities but who seek to diversify their portfolios away from equity and duration risk, these strategies may prove attractive.

Conclusion

Global equities and convertibles are likely to move higher through year end, given highly accommodative global monetary policy, moderate economic growth, corporate earnings growth, reasonable valuations, and robust M&A and buyback activity. While we are generally optimistic about global growth equities, we remain cautious about traditional fixed income, given the likelihood of higher U.S. rates by year end. Convertibles and select alternative strategies may prove a more effective way to hedge against rising rates and diversify equity exposure.

With the Fed likely to raise rates only modestly in the near term and the path likely to be gradual, we expect U.S. long-term rates to remain range bound over the next year. The growing political divide around austerity and an emphasis on monetary policy rather than fiscal policy are likely to add to Europe’s long-term growth challenges, but we believe that Europe can navigate the current Greece situation. We are closely analyzing the ramifications of the China equity meltdown and the pace of China’s growth trajectory, but Beijing has many tools at its disposal to stabilize economic and market conditions.

We believe we are well equipped for this environment, viewing it as one in which fundamentally driven research and active, high-conviction investing will be rewarded.

-----------

The U.S. Dollar Index measures the value of the U.S. dollar relative to a basket of foreign currencies, including Euro Area, Canada, Japan, United Kingdom, Switzerland, Australia, and Sweden. The CRB Commodity Index is a measure of the price movements of 22 sensitive basic commodities. The S&P 500 Index is considered generally representative of the U.S. equity market. The MSCI World ex-U.S. Index is a market capitalization weighted index composed of companies representative of the market structure of developed market countries in North America (excluding the U.S.), Europe and Asia Pacific regions, while the MSCI World Growth ex-U.S. Index tracks the performance of growth stocks in these regions. The MSCI Emerging Markets Index is a free float adjusted market capitalization index cited as a measure of the performance of emerging market equities. The Russell 3000 Growth Index is considered generally representative of the U.S. growth stock market. The Russell 3000 Value Index is considered generally representative of the U.S. value stock market. The Russell 2000 Index is considered generally representative of the U.S. small-cap stock market. The BofA Merrill Lynch VXA0 Index is considered generally representative of the U.S. convertible market. Oil is represented by the West Texas Intermediate Cushing Crude Oil Spot Price. The Citi Economic Surprise Indexes are objective, quantitative measures of economic news that measure the difference between actual releases and the median of Bloomberg survey data. The Hong Kong Hang Seng Index is generally considered representative of the Hong Kong equity market.

Price-to-earnings ratio (P/E) is a valuation ratio of a company’s current share price compared to its per-share earnings.

Earnings-per-share (EPS) is the portion of a company’s profit allocated to each share of common stock. Earnings yield is earnings divided by stock price. Quantitative easing refers to central bank bond buying activities. Outright Monetary Transactions is an ECB program in which the ECB purchases bonds of euro zone members in the secondary market. Long-term refinancing operations is an ECB mechanism for financing supporting to euro zone banks.

Duration is a measure of interest rate risk.

This material is distributed for informational purposes only. The information contained herein is based on internal research derived from various sources and does not purport to be statements of all material facts relating to the information mentioned, and while not guaranteed as to the accuracy or completeness, has been obtained from sources we believe to be reliable.

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be suitable for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

Outside the U.S., this presentation is directed only at professional/sophisticated investors and it is for their exclusive use and information. This document should not be shown to or given to retail investors.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

Unless otherwise noted, index returns reflect the reinvestment of income dividends and capital gains, if any, but do not reflect fees, brokerage commissions or other expenses of investing. Investors may not make direct investments into any index.

Calamos Investments LLC 2020 Calamos Court | Naperville, IL 60563-2787 800.582.6959 | www.calamos.com | [email protected]

Calamos Investments LLP 62 Threadneedle Street | London EC2R 8HP Tel: +44 (0)20 3744 7010 | www.calamos.com/global

©2015 Calamos Investments LLC. All Rights Reserved. Calamos® and Calamos Investments® are registered trademarks of Calamos Investments LLC.

OUTLKCOM 18087 0715Q O C