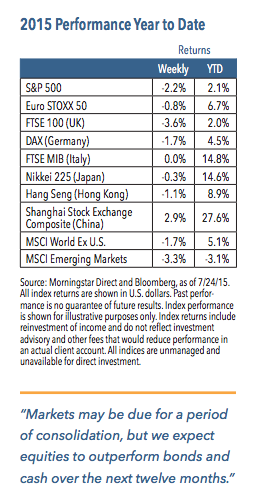

At the beginning of July, it became clear that Greece and European policymakers would come to at least a temporary debt agreement. Since that time, U.S. equity prices jumped, with the S&P 500 Index climbing more than 4% by the beginning of last week.1 That trend reversed last week, however, and the S&P lost about half of those gains, falling 2.2%.1 Some of the pullback can be blamed on the usual suspects — concerns over economic growth and corporate earnings, as well as worries over a pending shift in Fed policy. We would also argue that market technicals are starting to look uneven, suggesting equities may be due for a period of consolidation.

Key Points

▪ Equities may be stuck in a trading range until uncertainties over Fed policy and global growth diminish.

▪ Improving economic growth should allow corporate earnings to improve, helping stock prices to grind unevenly higher.

Weekly Top Themes

1. Corporate earnings have been mixed, but more positive than negative trends have emerged. To date, 35% of S&P 500 companies have reported secondquarter earnings.2 The good news is that earnings are beating expectations by 5.8%, which is above the average pace since the end of the Great Recession.2 Revenues, however, remain stuck in neutral, and are only exceeding expectations by 0.3%.2 The industrials sector has been hit by lower energy prices and slowing growth in China and has been trailing the rest of the pack.

2. Evidence continues to point to improvements in the jobs market. The latest weekly jobless claims reading shows the number dropped to 255,000.3 This marks the lowest level since 1973.3

3. We are not expecting significant news to come from this week’s Federal Reserve policy meeting. The Fed will probably reiterate there is ongoing progress in economic growth and suggest interest rate increases remain on the horizon. We don’t think the Fed will provide a specific timeframe, but September still seems to be the most likely starting point for the Fed’s first rate hike.

4. Issues in Greece and China have faded from the headlines, but structural problems remain. While investors may no longer be focused on the day-to-day drama, at some point these concerns may well resurface.

5. Market technicals appear stretched. In our view, signs such as the advance/ decline line and upside/downside volume have started to trend in a negative direction over the past few weeks. This may mean nothing, but our experience suggests it may also mean that equities are due for a period of consolidation that may last several weeks or longer.

When Uncertainty Fades, the Outlook Should Brighten

There are a number of issues causing investor unease to remain high. Questions over Fed policy, concerns over whether issues in China and Greece will lead to broader contagion and worries about the recent downshift in energy and commodity prices top the list. The last six months have been bumpy for equities, but we believe the landscape should improve over the next year, helping equities to outperform bonds and cash.

The trend of a rising dollar/falling oil dominated the investment landscape at the end of last year before fading in the spring. But more recently, we have a witnessed a return of these issues and the recent firming of the dollar and downtick in oil prices have caused some renewed concerns. Some of the moves have to do with easing geopolitical issues (such as signs of progress in negotiations with Iran) as well as slowing growth in China. But long-term structural issues should also keep upward pressure on the dollar and downward pressure on oil prices. The good news is that unlike what happened last year, recent moves have not triggered deflationary fears and massive downward moves in global government bond yields.

Looking ahead, we expect equity prices will be driven by a better corporate earnings environment and upward movement in U.S. interest rates. Rising rates have the potential to be disruptive in the near term for equities, but should the rate increase occur in an orderly manner, we think it will be perceived as an acknowledgement of improved economic conditions. This should provide a solid backdrop for earnings.

Equities may not be particularly inexpensive compared to their own history, but we think they appear attractive relative to bonds and cash. And although markets may churn until the outlook becomes more clear, we remain cautiously optimistic toward equity markets.

1 Source: Morningstar Direct, as of 7/24/15

2 Source: RBC Capital Markets

3 Source: Labor Department

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

©2015 Nuveen Investments, Inc. All rights reserved.