Equities, Dividends & Rising Interest Rates

Risk of Rising Rates

With interest rates at generational lows and what is likely an improving US economy, it is natural to contemplate or even worry about the possibility of rising interest rates. Common perception is that rising interest rate environments are generally not favorable to equities and income oriented investments. This is certainly true for bonds1 whose prices move directly and inversely with changes in interest rates. But is it true for equities in general and for dividend paying stocks in particular?

Not necessarily. A review of empirical data suggests that the link between interest rates and equities, including dividend paying equities is tenuous at best.

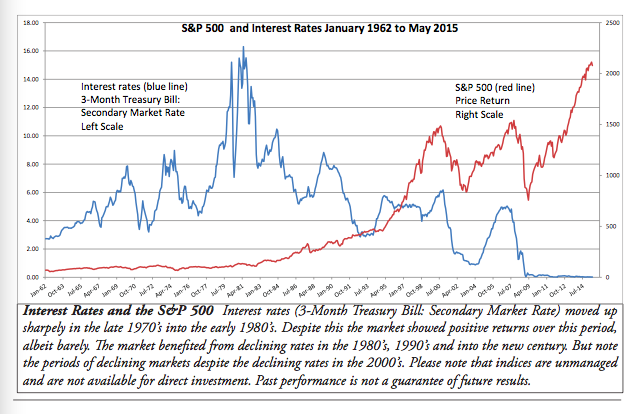

The accompanying graph shows the 3-Month Treasury Bill:2 Secondary Rate from January of 1935 through May of 20153 and the price value of the S&P 5004 over that same period. For expediency when we refer to the “market” we are referring to the S&P 500.

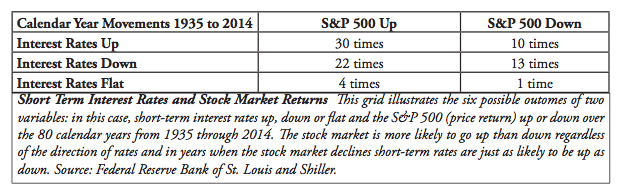

There are 80 calendar years over this time period. Over these 80 calendar years the S&P 500 index (price) advanced 56 times or 70% of the time, and declined 24 times, or 30% of the time.

Rates on the 3-Month Treasury Bill rose in 40 of the 80 calendar years, declined in 35 of the years and were flat in five of the years.

In the 40 years where interest rates rose during the year the market was up 30 times (75%) and only down ten times (25%). Historically, a rising rate environment has been three times more likely to coincide with a rising market than a declining market.

Counterintuitively, a declining rate environment isn’t quite as bullish as a rising rate environment. In the 35 years of declining rates the market rose 22 times (63%) and declined 13 times (37%).

For completeness, in the five years where interest rates were flat the market rose four times and declined once.

In summary, based on empirical data from 1935 through 2014, the market is more likely to be up than down; is more likely to be up than down when interest rates rise and more likely to be up than down when interest rates decline. And, a rising rate environment is more likely to coincide with a rising stock market than a declining rate environment.

Dividend Paying Stocks & Interest Rates

If the link between interest rates and the market as a whole (S&P 500) is tenuous it is important to separately consider to what extent the subset of dividend paying stocks are sensitive to interest rates. Specifically, do dividend paying stocks behave differently from the market as a whole; are they more sensitive to changes in interest rates than non or low dividend paying equities?

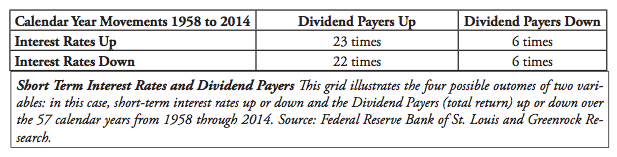

For the purposes of our analysis we are using the top 20% dividend paying companies in the S&P 500. For the sake of simplicity we’ll refer to these as “Dividend Payers.” Because our data series for this subset begins in 1958 we will be examining the period 1958 through 2014. In the period studied the total return for the Dividend Payers was negative only 12 times5 out of 57 years (exactly the same for the entire S&P 500).

As with the S&P 500 as a whole, there is no correlation between interest rate changes and the performance of the Dividend Payers. Interest rates rose in 29 of the 57 years. In these 29 years of rate rises the Dividend Payers produced a positive total return 23 times and a negative total return six time. Rates declined in 28 of the 57 years examined and Dividend Payers produced a positive total return in 22 of those years and a negative total return in six of those years. In short, years with interest rate increases are nearly four times as likely to coincide with positive returns for the Dividend Payers than negative returns.

Conclusions

What conclusions might we draw from this data? First, over the period studied, the data show that the market is more likely to rise than fall during rising rate environments and that it is more likely to rise than fall during declining rate environments. Further, interest rates are just as likely to be down as up during years the stock market declines.

These findings shouldn’t be too surprising. Rising rates may mean the economy is strong and that may be good for corporate profits which is good for the stock market. Further, a declining interest rate environment might be the result of economic weakness which may be bad for corporate profits and equities.

Is the Current Environment Different?

Might the current environment be different than the periods studied? Might a more accommodative Federal Reserve and extremely low interest rates be a major contributor to the current bull market? If so wouldn’t that mean equities may be more vulnerable to increasing interest rates than normal? Perhaps. But several points are worth noting.

First, corporate earnings and dividend payments have increased since 2008, meaning the rise in equities since then has not been about multiple expansion. In fact, the S&P 500 price earnings multiple in July 2015 is estimated to be 20.796. In 2008 it was 21.46. The earnings for the S&P 500 for 2014 were a record $103.61 and up from 2007’s $74.93.7

Second, one of the benefits of dividend paying stocks is that dividends have a tendency to grow. From January 1958 through 2014 the S&P 500 dividend payment grew from $1.79 to $39.44, an annualized growth rate of 5.68%.8 Included in this period were six years of negative dividend growth.9 If we are about to enter a period of rising rates it may well be that the objective of the interest rate increase is to normalize interest rates in light of a growing economy. Presumably that will mean in- creasing corporate profits and dividend growth, both of which should provide some support for dividend paying equities.

And, finally, a rising interest rate environment will, by definition, be detrimental to fixed-income instruments and (as we’ve seen based on empirical data) will not necessarily be negative for dividend paying equities. Even with a headwind for dividend paying stocks in a rising rate scenario, the ability for dividends to grow over time has historically meant that dividend paying stocks out perform fixed income instruments.

Footnotes

1 Under certain circumstances low credit quality, or junk bonds, may experience price movements in the same direction as interest rates.

2 We’ve chosen a short-term interest rate as our proxy for interest rates generally and presume most observers would do the same. However, we did also examine longer term interest rates, specifically the 10-Year Constant Maturity Treasury Bond yield and the comparison to the S&P 500 to changes in this rate were nearly identical to the comparison with the 3-Month Treasury Bill yield. The data series for the 10-Year Constant Maturity Treasury Bond, available from the Federal Reserve Bank of St. Louis, begins in 1962 so the period examined wasn’t perfectly analagous.

3 Source: Federal Reserve Bank of St. Louis.

4 Source: Robert Shiller Online Data. www.econ.yale./edu/~shiller/data.htm.

5 Source: Robert Shiller Online Data and Greenrock Research.

6 Source: mutpl.com http://www.multpl.com/table

7 Source: Robert Shiller Online Data.

8 Source: Robert Shiller Online Data. and Guinness Atkinson Asset Management.

9 Source: Robert Shiller Online Data.

Mutual fund investing involves risk and loss of principal is possible. Investments in foreign securities involve greater volatility, political, economic and currency risks and differences in accounting methods. These risks are greater for emerging markets countries. The Fund also invests in smaller companies, which will involve additional risks such as limited liquidity and greater volatility.

The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. The statutory and summary prospectus contains this and other important information about the investment company, and it may be obtained by calling 800-915-6566 or visiting gafunds.com. Read it carefully before investing.

Opinions expressed are those of Guinness Atkinson Funds, are subject to change, are not guaranteed and should not be considered investment advice.

Past performance is no guarantee of future results.

The S&P 500 is a market capitalization weighted index based on the 500 largest publicly traded American companies as determined by Standard & Poor’s. You cannot invest directly in an index.

Price Earnings Multiple (or Price Earnings Ra- tio), often referred to as a PE Multiple, is the current market per share price of a company divided by the current per share earnings.

Distributed by Quasar Distributors, LLC