The last decade has seen an extraordinary rise in the importance of a unique class of investor. Generally referred to as “price-insensitive buyers,” these are asset owners for whom the expected returns of the assets they buy are not a primary consideration in their purchase decisions. Such buyers have been the explanation behind a whole series of market price movements that otherwise have not seemed to make sense in a historical context. In today’s world, where prices of all sorts of assets are trading far above historical norms, it is worth recognizing that investors prepared to buy assets without regard to the price of those assets may also find themselves in a position to sell those assets without regard to price as well. This potential is compounded by the reduction in liquidity in markets around the world, which has been driven by tighter regulation of financial institutions, and, paradoxically, a greater desire for liquidity on the part of market participants. Making matters worse, in order to see massive changes in the price of a security, you don’t need the price-insensitive buyer to become a seller. You merely need him to cease being the marginal buyer. If price-insensitive buyers actually become price-insensitive sellers, it becomes possible that price falls could take asset prices significantly below historical norms. This is not to suggest that such an event is inevitable, still less is it an attempt to predict in which assets and when it will occur, but anyone conditioned to think that these investors provide a permanent support for the markets should be aware that the support may at some point be taken away.

Who are these guys?

There are a number of different groups of investors that could be characterized as price-insensitive buyers. A less than exhaustive list would include the monetary authorities of emerging countries, developed market central banks, defined benefit pension plans (particularly in Europe), insurance companies, risk parity investors, and single-strategy and index-driven mutual fund managers.

Monetary authorities

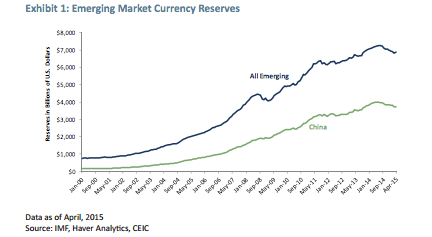

The first group of price-insensitive buyers to confound the markets were, arguably, the monetary authorities of emerging countries, who in the 2000s began to accumulate a vast hoard of foreign exchange reserves. These reserves, which served to both protect against a recurrence of the 1997-98 currency crises and to encourage export growth by holding down their exchange rates, needed to be invested. The lion’s share of the reserves went into U.S. treasuries and mortgage-backed securities, causing Alan Greenspan and Ben Bernanke to muse about the conundrum of bond yields failing to rise as the Federal Reserve lifted short-term interest rates in the middle of the decade. I have to admit that from a return standpoint, those purchases were ultimately vindicated by the even lower bond yields that have prevailed since the financial crisis. But just because the position turned out to be a surprisingly good one, return-wise, doesn’t mean that these central banks were acting like normal investors. Their accumulation of U.S. dollars had nothing to do with a desire to invest in the U.S., in treasuries or anything else, but was rather an attempt to hold down their own currencies. This made them more avid buyers as U.S. interest rates fell, insofar as falling U.S. rates tend to push down the U.S. dollar. The aggregate impact on markets from these price-insensitive buyers has almost certainly been considerable, as can be seen in Exhibit 1. Since 2000, some $6 trillion of currency reserves have had to be invested, and most of that has gone into high quality U.S. fixed income.

Did emerging market currency reserves cause the risk bubble in 2007? It would be hard to lay that at their feet given all of the stupid behavior by a whole variety of market participants, but it is certainly easy to imagine that by both taking high quality assets out of circulation and pushing down yields as they invested a net $3 trillion from 2003-08, they could have pushed demand into the riskier assets that got so mispriced in 2006-08.

After a small blip in 2008, these reserves continued to power higher through 2014. So how do these buyers turn into sellers? Easily. It has already been happening, actually, as commodity-producing countries have been selling down currency reserves to support their domestic economies. The dragon in the room, however, is China, where official reserves have gone from $150 billion in 2000 to $3.8 trillion today, a 25-fold increase that has left it with reserves greater than the next six largest national reserve holders combined. China has seen its official reserves fall by about $260 billion from their peak in mid 2014, as a weakening domestic economy seems to have reversed the pressures that led to their accumulation of reserves in the first place. The impact of these sales has been hard to see, however, probably due to the second group of price-insensitive sellers.

Developed market central banks

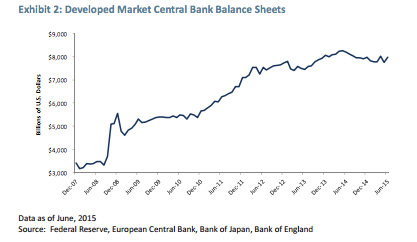

The financial crisis itself created the second group of price-insensitive buyers, developed market central banks. Quantitative easing policies by a wide array of central banks have had the explicit goal of pushing down interest rates and pushing up other asset prices. While one can argue that the central banks were anything but price-insensitive in that they cared quite deeply about the prices of the assets they were buying, they certainly were not buying assets for the returns they delivered to themselves as holders, and their buying has been driven by an attempt to help the real economy, not an attempt to earn a return on assets. Since 2008, the sum of the U.S., U.K., Eurozone, and Japanese central banks have expanded their balance sheets by over $4 trillion USD, as shown in Exhibit 2.

At the moment, the most active central banks in the developed world have been the European Central Bank and Bank of Japan, who between them are buying north of $100 billion a month of government bonds.

Defined benefit pension plans

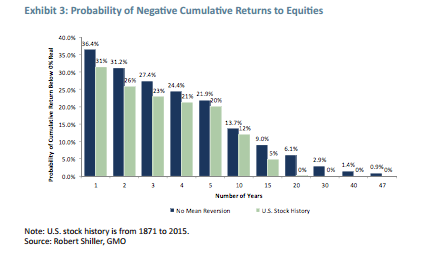

Considerations of profit and loss on their portfolios are seldom at top of mind for central bankers, making them obvious candidates as price-insensitive buyers. But regulatory pressure can push otherwise profit-focused entities in similar directions. Successive tightening of the regulatory screws on defined benefit pension funds, particularly in Europe, have forced many of them into the role of price-insensitive buyers of certain assets as well. Some of the first to push down that path were U.K. plans, where mandatory cost-of-living adjustments to pensions made U.K. inflation-indexed bonds a required holding, even as rates moved into hitherto unthinkable negative real rates. These were soon followed by other European funds such as the Dutch, where the Dutch central bank forced the plans into owning very large portfolios of liability-matching assets, largely high quality long-term bonds. It’s not that it is silly for investors to consider the nature of their liabilities in building their asset portfolios, and it also makes perfect sense for regulators to step in when there is the kind of agency problem that exists for defined benefit pension plans.1 The trouble is that in order to avoid the sponsors from doing inappropriately risky things, gray areas and matters of valuation are generally dealt with poorly, if at all. As an example, inflation-linked bonds are certainly a low-risk asset against an inflation-linked liability of a similar duration. But real estate, infrastructure, and equities are also long-duration inflation-linked assets. While their cash flows are less certain than a government bond, the relative yields available on these assets would be a crucial consideration for a rational asset allocation. In the U.K., however, regulations declare that the index-linked bond is an inflation hedge in a way that others are not, and the regulations require hedging the portfolio. The real yield on long-term inflation-indexed bonds in the U.K. has been close to zero or negative for most of the last decade, yielding far less than other assets that can be plausibly thought of as inflation hedges. The funny thing about the regulatory pressure is that it pushed hardest on the long-term inflationlinked bonds due to the long-term nature of the pension liability. The U.K. issues a 50-year inflationlinked bond. The bond maturing in 2062 yields -0.8% as of July 3. But it references RPI as its inflation adjustment and this tends to be 0.5 to 1.0% higher than CPI, so let’s assume this is equivalent to 0% over inflation. An investor interested in earning returns between now and 2062 can lock in a guaranteed zero return instead of the uncertain return from assets like stocks and real estate. So what are the odds that stocks do worse than 0% real over the next 47 years? Exhibit 3 shows the likelihood of stocks underperforming an asset guaranteeing a 0% return as a function of time horizon. It shows both the probabilities if stocks return +5.7% real with a volatility of 16% and do not mean revert and the probabilities given the actual historical returns of stocks in the U.S. since 1871.

In a world of no mean reversion, there is indeed a chance of stocks underperforming the 2062 indexlinked bond over the course of its life – approximately a 1% chance. For what it’s worth, the average shortfall relative to 0% real for that 1% of the time is 24%. And this means that if you are actually interested in wealth in 47 years, you can either guarantee to maintain your wealth exactly by owning the index-linked Gilt, or invest in stocks and have a 99% chance of doing better than 0%, with an average terminal wealth of 13.5x your initial amount. In the unlikely event that you are in the 1% that falls short, you would expect to have lost 24% of your initial amount. If the odds were even on that trade – a 50% chance of making 13.5x your money and a 50% chance of losing 24%, – you should take that trade all day long. With 99% odds of winning, it seems you’d have to be insane not to.2

And yet, in the last decade, managers of U.K. pension funds have basically doubled the percent of their portfolio that they had put into long-term IL Gilts while cutting their allocation to equities by a similar amount. And they are not insane. They are doing what they are forced to do by a wellintended regulatory framework. And the point to recognize about their willingness to buy the IL Gilts and sell equities, given the pricing, is that managers choosing to buy the bond in that situation are clearly unlikely to change their buying decision based on a change in the yield on the bond. It is not as if they bought them saying “at zero real I’m a buyer of the bonds, but -0.5% real would make me a seller.” So if yield won’t do it, what else could? Actually, the answer is very simple and leads to our concern about the index-linked Gilt market. If a class of investor is forced to buy a type of security irrespective of price, the thing that can change that behavior is the cash flow of that class of investor. When cash is flowing into U.K. defined benefit pensions, the marginal buyers of index-linked Gilts are almost certainly those pensions. When cash begins to flow out, they basically cannot be buyers of the index-linked Gilts anymore, and could easily become sellers.3 The next set of buyers is less likely to be as price-insensitive as the pension funds. While bonds are finite life instruments, a 2062 bond will be around for a long time, and it is a truly mystifying investment for anyone who is not forced to own it.4

Risk parity

Another group of price-insensitive investors are managers of risk parity portfolios. These portfolios make allocations to asset classes not with regard to pricing of assets, but rather their volatility and correlation characteristics. Their price-insensitivity comes out in a couple of ways. First, as money flows into the strategies, they are levered buyers of bonds and inflation-linked bonds in particular. Like most strategies, if the money flows out, they are forced sellers of a slice of their portfolio. Second, unlike many other investors, they will also tend to buy and sell based on changes in volatility. As the volatility of an asset falls, these strategies will tend to lever it up further, and as the volatility rises they will sell. Given that low volatility tends to be associated with rising markets and high volatility with falling markets, this gives their buy and sell decisions a certain momentum flavor. If bond prices are moving up in a steady fashion, they will tend to buy more and more as volatility falls, and in a disorderly sell-off that sees yields and expected returns rise along with rising volatility, they will sell the assets due to their higher “risk.” In fact, rising volatility in bond markets could cause a general delevering of risk parity portfolios, causing them to sell assets unrelated to bonds in order to keep their estimated volatility stable. With hundreds of billions of dollars under management in risk parity strategies and large holdings in some of the less deeply liquid areas of the financial markets such as inflation-linked bonds and commodity futures, it is easy to imagine their selling in unsettling markets under certain circumstances, such as a repeat of 2013’s “Taper Tantrum.”

Traditional mutual funds

While the levered nature of risk parity portfolios may cause them to punch above their weight in potentially disrupting markets, in the end it isn’t clear that they are more likely to cause trouble than the managers of traditional mutual funds.

The mutual funds are at the mercy of client flows. As money has flowed into areas such as high yield bonds and bank loans, they have had little choice but to put it to work, and given their mandates, prospectus restrictions, and career risk, they are largely forced to buy their asset classes whether or not they think the pricing makes sense. But to an even greater degree, when redemptions come, they have no choice but to sell. This is nothing new. But what has changed is the extent to which mutual funds have seen large flows into increasingly illiquid pieces of the markets, particularly in credit, where bank loan mutual funds are 20% of the total traded bank loan market and high yield funds make up another 5%. That may not sound particularly large, but almost half of that market is made up of CLOs, which are basically static holders of loans. This makes the “free float” of the bank loan market perhaps half of the total, and should the bank loan mutual funds sell, there are not a lot of investors for them to sell to.

This is particularly true given the changes to the regulatory landscape for the dealer community. Banks are much less likely to take bonds and loans on their balance sheet for any length of time in the course of their market-making activities. This is true for all sorts of securities – given new regulations such as the Supplementary Leverage Ratio Rule, which started coming into effect early in 2015, even very safe securities such as Treasury Bills can require expensive capital charges for dealers to hold onto. The banks’ willingness to hold significant inventory of low-rated, less liquid instuments such as high yield bonds and bank loans is a fraction of what it was prior to the financial crisis.

Conclusion

The size of the price-insensitive market participants is impressive. Monetary authorities and developed market central banks have each bought on the order of $5 trillion worth of assets for reasons that ultimately have nothing to do with earning an investment return on them. Regulatory pressures have caused pension funds, insurance companies, and banks to do likewise. While it is somewhat harder to put precise numbers to the size of these investments, it seems a safe bet that the total is in the trillions as well. Other investors are in analagous positions for different reasons, as strategies such as risk parity and the exigences of life as a mutual fund portfolio manager push such investors to also buy assets for reasons other than the expected returns those assets may deliver. To date, these investors have tended to be buyers, and given their lack of price-sensitivity, they have pushed up prices of assets beyond historically normal levels.

At the same time, a natural buffer for many markets against a temporary imbalance between buyers and sellers, the dealer community has been forced to significantly curtail its activities due to the regulatory regime. So if circumstances cause these price-insensitive buyers to turn around and become price-insensitive sellers, there are not a lot of candidates to take the other side. As instrumentagnostic, price-obsessed value investors, we stand ready to buy should the virtuous cycles turn vicious and prices in some disrupted market become compelling to us. However, our paltry few billions of firepower pales in comparison to the trillions of dollars that have pushed markets up, and might, just possibly, push them back down. Be prepared for the possibility that some of the same assets that have again and again risen to prices that many investors said were impossible show more downside volatility than investors have bargained for.

So, what are we doing today in our portfolios to prepare for this possibility? In an “offensive” sense, not a lot, as it is very difficult to position a portfolio for an uncertain future event occurring in one or more asset classes at an undetermined time. But a couple of things are clear. First, to paraphrase my colleague James Montier, when you are uncertain about the future, don’t position your portfolio as if you were certain. Today we are making sure not to be so large in any asset class that we would not be comfortable increasing our exposure to it if its valuation fell significantly. Beyond that, we are trying to retain our flexibility to react to market gyrations by holding a significant amount of cash as dry powder. In a world where we could be confident that the price-insensitive buyers would stay buyers and valuations stay high, that cash would feel like a painful drag on performance. Today it feels like prudent flexibility in a world where the pressures on markets might well reverse in a way few are banking on.

1 The problem is a straightforward one. The sponsor of the plan is primarily interested in providing the pension at the lowest possible expected cost, which generally means running a portfolio with plenty of risk relative to the liability stream. Should things go badly wrong, the ultimate bearer of that risk can easily wind up being the pensioner or the taxpayer

2 In a world where equity prices do mean revert in a fashion similar to U.S. stock market history, the odds of winning versus 0% real are 99.999998%, for what it’s worth, which goes some way to explaining why we have not yet seen a 47-year period in which equities lost money in real terms. You’d expect a loss in stocks relative to 0% real in 1 in every 41 million 47-year periods.

3 If the pension funds literally had ladders of IL Gilts in line with their cash flows, this would not be the case as the bonds would expire in line with the payouts. However, it seems likely that their holdings are less accurately targeted than that, both because of the limitations of what is available in the market and the fact that their actuarial liabilities aren’t really the same as their true cash flows. They are generally focused on the regulations around the former than truly immunizing the latter.

4 Data from the U.K. Investment Association and Bank of England suggest that U.K. defined benefit pension funds own about 40% of the IL Gilt market. One presumes their holdings are concentrated at the long end, though, where they are quite likely the majority of the market. Who else owns these bonds? Probably some are owned by insurance companies, which face some of the same regulatory issues as pension funds. Other holders are likely speculators for whom the very long duration of the bonds gives them a lot of bang for the buck as a speculative instrument.

Disclaimer: The views expressed are the views of Ben Inker through the period ending July 2015, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2015 by GMO LLC. All rights reserved.

© GMO