Introduction

I have always had a much more interesting job than average in the investment business, with an enviably large chunk of my time to examine what I chose to. But, still, there was quite a bit of boring maintenance work needed to support the brainstorming or pure reflective time. Such time is, in my opinion, the backbone of a creative organization and it should be highly protected, but in real life you have to fight for it and you should, for we all know how quickly maintenance work can eat into our thinking time.

Well, the good news for me is that I now have an ideal job in which almost no maintenance work is required, and I have no routine day-to-day responsibilities. I am consequently free to obsess about anything that seems both relevant and interesting, which for the time being has come down to 10 topics that really matter, at least in my opinion. They can all be viewed as problems: potential threats to our well-being. I admit this is lopsidedly negative, but surely it is more important to obsess about threats, which we often prefer to ignore. Good news, in contrast, will usually look after itself. Trying to keep abreast of all of these topics would be at least a full-time job for the average reader, as it is for me, for some are changing very rapidly indeed. So for this summer’s quarterly, I have decided to very briefly summarize all 10 topics; to cover some interesting new research on several of them; to review one or two older but potentially important research projects that slipped through in the past with much less attention than seems appropriate; to discuss one or two pennies that have recently dropped for me; and, finally, to highlight a few new pieces of interesting data on several of these topics. So, here we go…

1. Pressure on GDP growth in the U.S. and the balance of the developed world: count on 1.5% U.S. growth, not the old 3%

2. The age of plentiful, cheap resources is gone forever

3. Oil

4. Climate problems

5. Global food shortages

6. Income inequality

7. Trying to understand deficiencies in democracy and capitalism

8. Deficiencies in the Fed

9. Investment bubbles in a world that is, this time, interestingly different

10. Limitations of homo sapiens

1. Pressure on GDP growth in the U.S. and the balance of the developed world: count on 1.5% U.S. growth, not the old 3%

Recap

Factors potentially slowing long-term growth:

a) Slowing growth rate of the working population

b) Aging of the working population

c) Resource constraints, especially the lack of cheap $20/barrel oil

d) Rising income inequality

e) Disappointing and sub-average capital spending, notably in the U.S.

f) Loss of low-hanging fruit: Facebook is not the new steam engine

g) Steadily increasing climate difficulties

h) Partially dysfunctional government, particularly in economic matters that fail to maximize growth opportunities, especially in the E.U. and the U.S.

Comments

Mainstream economists, with their emphasis on highly theoretical models, have been perplexed by the recent chain of disappointments in productivity and GDP growth and would disregard all or most of these factors as theoretically unsatisfactory.

I am impressed by how many of these factors intersect with the important problems I obsess about. This might offer a reason for taking them more seriously, for few things could be more important background information for any market analyst than to have been prepared for a steady diet of topline disappointments.

2. The age of plentiful, cheap resources is gone forever

Added Thoughts

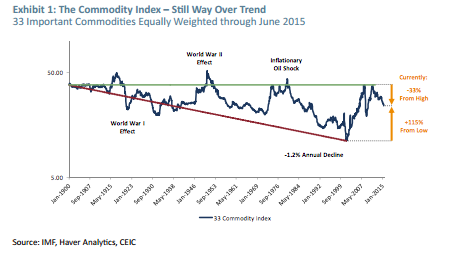

After every historical major rally in commodity prices, there has been the predictable reaction whereby capacity is increased. Given the uncertainties of guessing other firms’ expansion plans, the usual result is a period of excess capacity and weaker prices as everyone expands simultaneously. The 2000 to 2008 price rally was the biggest in history, above even World War II. It was therefore not surprising that the reflex this time was the mother of all expansions and excess capacity. This was further exaggerated by a sustained slowdown in demand from China, which is still playing through. The most dramatic example of this was in China’s use of coal, which had grown from 4% of world use in 1970 to 8% in 1988 and to 50% in 2013, the world’s most remarkable expansion in the use of anything since time began. And yet this remarkable surge was followed in 2014 by a reduction in China’s use of coal! And that in a year in which China was still growing at over 6%.

So, how profound was this supply surge and price decline? Exhibit 1 shows our original index, which is made up of 33 important commodities equally weighted to avoid the data being overwhelmed by oil, which constitutes around 50% of all tradable value in commodities. You can see that although the average price has declined handsomely, it has only given back about one-third of the preceding great price surge. And now with a further sell-off in commodities following China’s recent mini stock bust, the reaction phase may be more or less complete: projects have been cancelled and capital spending plans in general have been savaged. Investment attitudes are extremely negative, which is, as always, a requirement for change. Today’s Wall Street Journal (July 21, 2015) carries a headline: “Investors Flee Commodities.” Promising. From now on it seems likely that prices will be more mixed, with some rising as others continue to fall. What seems extremely unlikely, assuming we have no global depression, is a return to the declining price trend of the 100-year period ending in 2000.

In agriculture, we also had a global sell-off following three consecutive years in which extremely hostile grain-growing weather had driven prices to panic levels of triple and quadruple their previous lows. Good, unused arable land was scarce, but most of what could be thrown into battle was. And, as I suggested three years ago (for which I took some grief), investors should have counted on less bad weather inevitably arriving, perhaps even above-average conditions, which for the last two years has occurred. Yet although grain prices are way down (approximately -40%) from their panic shortage highs of 2011, they are still way up (approximately +70%) from their 2000 lows. And bad weather will be back: it has been bad here, there, and everywhere recently (California’s drought, notably) except for major grain-growing areas.

All in all I am still very confident, unfortunately, that the old regime of irregularly falling commodity prices is gone forever.

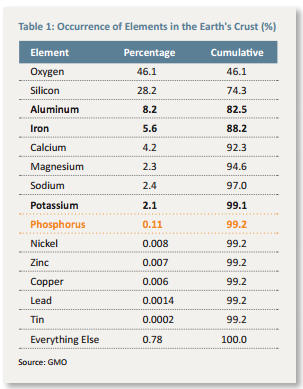

A further change in my thinking on resource availability has to do with their occurrence in the Earth’s crust (see sidebar on page 11). I will no longer worry about the three important commodities that are relatively plentiful: bauxite (aluminum) at 8.2%, iron ore at 5.6%, and potash (potassium) at 2.1%. Even though a relatively plentiful supply in the Earth’s crust does not absolutely guarantee long-term cheap resources – e.g., aluminum is more about the electricity cost to extract it – life is too short to focus on anything but the biggest threats to our well-being. For instance, why worry about the critical-to-life potassium when phosphorus, equally critical, is one-twentieth as common! Similarly, chrome, nickel, zinc, copper, lead, and tin added together are not nearly 1% of iron ore’s occurrence.

3. Oil

Recap

Among commodities, oil has been king and still is. For a while longer. Oil has driven our civilization to where it is today. It created the surplus in our economic system that allowed for scientific research and rapid growth. Now, as we are running out of oil that is cheap to recover, the economic system is becoming stressed and growth is slowing.

A Penny Drops

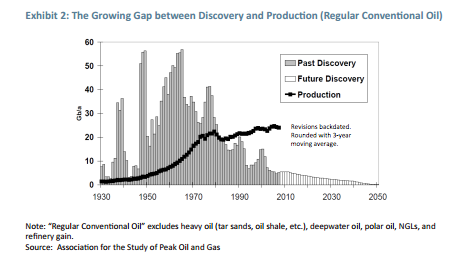

I hope you will remember Exhibit 2. It is used by all peak oilers. It really does show what we might call the first derivative negative: If we keep on pumping more than we find, we will certainly run out of cheap oil. Eventually. But this data is also unsatisfactory. Given this exhibit, how is it possible that since 1982 (the first year we pumped more than we found) global reserve life has risen by 60%, despite oil demand growing by 1.5% a year? (Which dichotomy has led the bulls to ignore all negative data and assume that somehow we will always have enough oil.) Well, this is why. When the original giant Saudi fields were being discovered, the first oil volunteered to bubble to the surface virtually free of cost. Why bother to expensively tease out more with so many new fields being discovered? The ultimately cheap recovery rate was only about 15% of the oil that was there, but who cared? By 1982, U.S. production, for a while the largest in the world, had famously peaked out (in 1970) so there was a modestly growing interest globally in capturing more, and recovery rates had risen to around 20% (all numbers here are rounded). And what are the recovery rates today? Now, in comparison, we torture oil fields with expensive and energy-intensive secondary and tertiary recovery tricks: compressed CO2, water under pressure, high-pressure steam, and, I suppose the ultimate torture, fracking – shocking and fracturing the rock with the encouragement of water, sand, ceramic beads, and an often secret mix of toxic and non-toxic chemicals, a process that is considerably more expensive than actually drilling the original well. With these efforts (and excluding fracking) we now aim for 60% recovery, with a new outlier from Statoil in the North Sea aspiring to 70%. What this means is that all of the oil fields ever discovered could now yield three times the oil originally counted on, as recovery has risen from 20 to 60%. To keep the math simple, this is about equal to a 3.5% a year compounded increase in reserves since 1982. With demand only growing at 1.5% a year, rising recovery rates have increased recoverable reserves to 50 times current global production, up from 32 times in 1982. Not bad. In fact, reserve life would have slightly increased with no new finds at all since 1982.

But, here is the problem. The cost rises exponentially as one moves up the recovery curve, and somewhere between 75 and 85% recovery we are unlikely to be able to afford the cost. In fact, the energy required to recapture more starts to overtake the energy produced. Checkmate. A move from 60% recovery to 80% (to be friendly) in the next 35 years would represent a 33% increase, or about 0.9% a year. This is obviously a big step down from the previous 3.5% a year, but it is still good news and bad news. The bad news for oil bulls is that this recovery game, which we might call the second derivative negative to production, is playing itself out quite fast. The good news is that with slower global growth and more emphasis on energy efficiency and a probability of some carbon tax increases, global oil demand may settle down to around 1% a year for the next 10 to 15 years. At that level of increase in demand, even modest continued increases in recovery rates will keep us in oil even if no new oil is found for the next 15 years. However, here’s the snag: Increased recovery rates will take steadily increasing prices, which we may or may not be able to afford. And if these price rises occur, they will act as a continuous drag on global growth rates. Beyond 15 years, the resource and environmental news gets better because cheaper electric vehicles and changes in environmental policy will enable steady decreases in oil demand, and the remarkable insight of Sheik Yamani, Saudi Arabia’s oil minister, three decades ago will prove to be right: We will not run out of oil any more than the Stone Age ran out of stone – we will simply find better fuels.

Yet more bad news on tar sands

No one took in my main point in an earlier quarterly regarding the pipelining of tar sands. (As in Nobody!) The point was that while tar sands oil may not leak any more than regular crude, when it does, diluted bitumen, as it is called, releases poisonous benzene gas and then sinks if it hits water, unlike crude, and costs over 10 times more to clean up.

There is now another good reason to hope tar sands stay where nature put them and that we skip the XL Pipeline: A recent detailed study1 of 30 important global oils (different by type and location) looked at how much carbon dioxide is created at every stage, including, in the case of tar sands, the loss of arboreal forest, which occurs before squeezing and heating the sands begins. The study measured the differentials in refining and transportation all the way to end-use. We had all heard that products from tar sands caused only 10 or 12% more CO2 to be released than from regular oil, and I for one twitched skeptically, having an image of their colossal operations, which look like they chew energy relentlessly. Well, it turns out that when burned, because their products are on average heavier than those from lighter, more typical oils, they do release only 10 or 12% more CO2 than average. But that only counts when burning the product. When clearing the forest, squeezing out the oil, shipping and refining, and all of the other activities are included, tar sands products release fully 40% more CO2 than the median oil in the study!

Now, the economy is going to need to use as much oil as it can safely use during the transition to renewables. To use unnecessarily CO2-intensive products and thereby limit our safe allotment is just bad for the economy, needlessly risky for the environment, and benefits only the principal players in the tar sands business. A leading producer of tar sands, Koch Industries, has enormous influence with Congress, so there will be relentless effort exerted to back what is for all the rest of us a truly suboptimal use of a resource that is currently vital to our economy but extremely dangerous cumulatively to our environment. This is particularly the case when we are producing so much of our own light, sweet crude in the Bakken and elsewhere.

4. Climate Problems

Both the actual climate and the associated politics seem to be changing more rapidly these days, with the seriousness of the situation becoming better appreciated. Visible changes in the climate have also been accelerating, with many more records than normal of droughts, floods, and, most particularly, heat. Last year was the hottest year ever recorded, and this year, helped by an El Niño, has gotten off to a dreadful start. January was the second hottest January ever. February and March were outright records. April was in third place, but both May and June were back in first place. This consistency with volatile climate is unusual and ominous. If kept up, 2015 will be the hottest by a lot. Angela Merkel, a chemist by University training, arm-twisted the G7 countries, especially Japan and the recently rogue Canada, into a statement committing their countries to decarbonizing their economies completely by 2100 and making some increased effort by 2050, a respectable improvement but still very insufficient for the long term. It was probably the first time for several decades, by the way, that it was reasonably clear that someone other than a U.S. President was the natural leader: at least on some issues.

Pope Francis weighed in with a brave encyclical, which was bound to cause trouble with his flock, making the clear case that it is a Catholic’s duty to help protect our home planet and that manmade climate change from excessive burning of CO2-producing fossil fuels is an urgent problem. He was advised by the Pontifical Academy of Sciences, which includes several Catholic, as well as non-Catholic, Nobel Prize winners and several of the world’s leading scientific authorities on climate change. How did he arrange this? If only our politicians had such advisors and availed themselves.

Several developed and developing countries, including Ethiopia and Brazil, made unexpected unilateral commitments to reduced CO2 targets. Imagine a country as poor as Ethiopia and with so small a carbon footprint making any commitment without a clear recompense. Things really are changing.

There was also an unusual number of important scientific articles, summaries of which follow.

A) A very silent spring

Climate damage is proceeding far faster than predicted 5 or 10 years ago, as regards deteriorating farming conditions, sea level rises, ocean acidification, and species die-off. A recent report2 estimates the disastrous decline in total animal life: In general it has halved in the last 40 years, with bird populations down 40%. Based on the loss of almost all megafauna in North America shortly after humans arrived and of millions of buffalo and billions (down to the last one) of passenger pigeons (perhaps the most numerous bird that ever existed), not to mention the stories of the quantities of fish in the oceans and salmon in the rivers in Colonial times, it is reasonable to guess that we humans have already at least halved it once before in our history. And the negative effects of climate change are only now kicking in. See the new report from the Audubon Society3 on the damage likely to be inflicted on future bird populations by climate change. It is easy to imagine that in another 40 years we will have springs that are very silent indeed.

B) Irreversibility

Disturbingly, some changes look likely to last forever. It was recently announced, for example, that the Thwaites Glacier4 in the Antarctic has “gone irreversible,” as I like to say. It will apparently collapse in the next century (or several centuries if we are lucky) even if we never burn another gallon of gas. Fortunately, the sea level rise from this event may take up to hundreds of years, but it just might be much quicker. It should be noted that this is explicitly not accounted for in the United Nations’ reports (IPCC). There is something especially disturbing about irreversible events, and other dangerous, irreversible or self-sustaining changes are likely to occur: When arctic sea ice melts, the dark ocean absorbs more sunlight than reflective ice had and therefore more ice melts, etc. Potentially far worse, the melting of frozen tundra gives off methane, which in the near term (20 years) is over 80 times worse than CO2 as a greenhouse gas. And the ultimate worst is the possible melting of the frozen undersea methane clathrates, notably on the Siberian continental shelf. These deposits are said to contain as much greenhouse gas potential as all fossil fuels combined. This could, at worst, make for a very finite lifetime for our very favorite species, homo not so sapiens.

C) The effects of climate change on extreme weather events

Two new articles appeared this past June on this topic in Nature Communications5 and Nature. 6 They both deal with the direct thermodynamic effects of a warming climate, which account for most of the increase in extreme temperature events. Their argument, simplified, is that climate change may not cause more hurricanes or more droughts, but when they do occur, the higher ocean and air temperatures will guarantee that these events will be worse than they would have been in a lower-temperature world. (Hurricane Sandy had warmer water supplying more energy and California’s drought has near-record temperatures further drying up waters already reduced by a near-record lack of precipitation, with the combined effect exceeding any such event in over 1,000 years.)

The Nature article adds a second variable: the shifts caused by climate change to air and ocean currents. These changes cause a minority of extreme weather events, mostly hot extremes, but a few of them cold extremes, due mainly to “blocking,” wherein extreme weather patterns can be sticky and last longer than normal as was the case of the infamous “Arctic Vortex.”

D) Oceans under stress

In the July 3, 2015 issue of Science, 22 scientists led by Jean-Pierre Gattuso made the case that even relative to the substantial land-based problems of climate change, oceans were not receiving their appropriate share of concern. Ocean life, they say, is diminishing at the fastest rate since the so-called Great Dying of 250 million years ago. The oceans have absorbed 90% of all of the extra heat generated, and this makes it harder to hold oxygen in their waters. They also have absorbed 30% of the extra carbon dioxide, which forms a mild acid in water and makes life more difficult for shell-forming creatures, many of which are critical food supplies at the bottom of the chain. Their main addition to the field from this report, though, is this: a species might be able to adapt to less oxygen, or to a higher temperature, or to more acidity, but it is the three stresses arriving together that is the killer. In a different context (e.g., coral reefs and mangrove swamps, which act as critical nurseries for fish), they could have added that if those three factors don’t get you, overfishing, coastal pollution, and reef destruction will.

For coastal and ocean-going fish alike, the stresses increase and populations fall. Wild fish from the oceans will decline as a source of protein, further threatening the global food supply situation. Our future behavior will decide whether the declines are catastrophic or merely painful.

E) Water, stress, and the Middle East

Outside of the world of scientific papers, Andy Lees, a financial analyst in London, wrote a disturbing paper on the particular stress that insufficient overground water and rapidly declining water tables, exacerbated by warming temperatures, is putting on Middle Eastern countries from Syria and Iraq to the Yemen. These stresses are destabilizing these societies and several others as you read. The full article can be read at http://us2.campaign-archive1. com/?u=3137408ede7caf09677250e66&id=7355a4b3ec&e=c44cfbd9ab.

5. Global food shortages

Recap

The world’s population continues to grow, and the increasing middle class of the emerging countries, especially China, is rapidly increasing its meat consumption. Both trends put steady pressure on our grain and soy producing capabilities at a time when productivity gains have been irregularly slowing for several decades and show every sign of continuing to slow.7 Both overland and underground water supplies are stressed. Weather for farming becomes increasingly destabilized with increased droughts and radically increased flooding events. Flooding particularly increases soil erosion, which still continues at 1% a year, close to 100 times natural replacement rates. Insects and weeds are apparently becoming resistant to chemicals faster than chemists can respond.

New Research

“In this scenario, global society essentially collapses as food production falls permanently short of consumption.”8

The IPCC report from the U.N. last year made the point that humanity is risking “a breakdown of food systems linked to warming, drought, flooding, and precipitation variability and extremes.” This was relatively outspoken for a conservative organization that needs to find consensus involving dozens of scientists on every issue. I have aired my disgruntlement with the typical timidity of scientists when they are dealing with the public. But on this point I was completely gruntled by a report9 last month from the Global Sustainability Institute of Anglia Ruskin University in the U.K. This unit is backed by Lloyds of London, the U.K. Foreign Office, the Institute of Actuaries, and the Development Banks of both Africa and Asia – a grouping with a very serious interest in the topic of food scarcity and societal disruptions to say the least. The team of scientists used system dynamic modeling, which uses feedbacks and delays, to run the business-as-usual world forward 25 years. Without any new and improved responses from us, the results are dismaying: Prices of wheat, corn, soybeans, and rice were all predicted to be at least four times the levels of 2000. (They are currently about double.) The team concluded, “The results show that based on plausible climate trends and a total failure to change course, the global food supply system would face catastrophic losses and an unprecedented epidemic of food riots. In this scenario, global society essentially collapses as food production falls permanently short of consumption.” And you thought my argument on food problems of the last three years was way over the top! But what they could have added was that this year’s 800,000 refugees trying to get into Europe and already stressing finances, organizational skills, and, one must admit, liberal attitudes, would likely become an intolerable flow of millions in 25 years. They could also have waxed more eloquently on the guaranteed and simultaneous loss of food from the oceans (covered previously) unless we change our fishing and pollution habits as well as our fossil fuel use.

6. Income inequality

Recap

Over the last few years, we have been presented with data showing that the U.S. is the most unequal society (or one of the two or three worst) in both income and wealth in the developed world. It is also one of the less economically mobile ones, especially for mobility out of the poorest quintile. Neither situation applied or even nearly applied 40 years ago. (Thomas Piketty’s book Capital in the 21st Century presents particularly detailed data on this topic at rather painful length, although it did serve very well in drawing necessary attention to it.)

Academic economists such as Robert Gordon have begun to make the case that extreme and growing inequality is holding growth back in the U.S. When it comes to economics these days, common sense usually produces more reliable conclusions than do mainstream economists, and on this topic, common-sense logic also seems compelling, doesn’t it? If the broad middle class makes little or no progress for 40 years in real wages earned in an hour – as the official U.S. statistics show – then it would not be surprising if: a) debt became a problem from time to time as the median earner attempted to make modest improvements in lifestyle; and b) that consumption and growth rates were persistently a little disappointing, as indeed they have been.

Underappreciated research

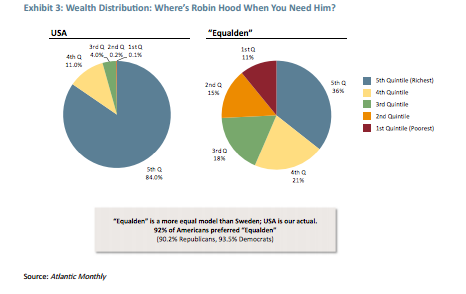

Dan Ariely, the James B. Duke Professor of Psychology and Behavioral Economics at Duke University, presented some particularly user-friendly data on the topic of income inequality in the Atlantic Monthly. 10 (Such populism presumably cost him a few points with mainstream economists.) The title of the article pretty much says it all: “Americans want to live in a much more equal country (they just don’t realize it)”. The guts of the data is a survey of over 5,000 Americans, carefully selected to be a balanced representation of the population. They were first asked how equal they believed a society should be in income and capital, and then asked how equal they believed it was in real life. Exhibit 3 reproduces the key data. Self-identification as Republican or Democrat made surprisingly little difference. The exhibit’s real shocker is the actual distribution of wealth, which is far worse than the participants believed and far, far worse than they believed to be fair. In fact, when presented a choice between our actual distribution of wealth in the U.S. (although deliberately mis-identified as purely theoretical) and an idealized fairer-than-Sweden model, well over 90% of both Republicans and Democrats preferred the fairer model! Remarkable! It is good material with which to ponder the question as to how our current misbegotten, adversarial political system has drifted so far away from what the ordinary voters actually think would be fair.

7. Trying to understand deficiencies in democracy and capitalism

Democracy

“The central point that emerges from our research is that economic elites and organized groups representing business interests have substantial independent impacts on U.S. government policy, while mass-based interest groups and average citizens have little or no independent influence.” [Emphasis added.] This is the killer conclusion of a paper last fall by Gilens and Page.11 Based on the study of almost 1,800 policy issues for which income breakdowns were available, and defining the “Elite” generously as those above the 90th percentile, it finds that “majoritarian electoral democracy” is largely a thing of the past.

To keep the review of this study short, it is probably only necessary to point out that the average bill in the U.S. Congress has a 31% chance of passing; this chance falls to 30% when the proposed legislation is hated by average citizens and rises to 32% when they love it! In contrast, love from the economic elite, although not absolutely guaranteeing success, raises the chances of its passing to 60%. But when the elite truly detest an issue, it is like passing a death sentence: About 1% of these bills pass!

It would be helpful to know one day whether it is the 1%, the .01%, or only the top 2,000 or so who really drive this data, for it is surely not the top 10%. Other than that, the data speaks for itself: It would seem that “government of the people, by the people, for the people” has indeed, for practical purposes, “perish(ed) from the Earth.” Lincoln would no doubt urge us to try to resuscitate it.

Capitalism: a failure to be inclusive (and feathering the corporate officers’ nests)

I have previously gone on at length about the critical, perhaps even deadly, deficiency in capitalism in dealing with long-term issues of the commons – damages to our common air, water, and soil. I would now like to take a swipe at capitalism’s increasing failure to be inclusive. Capitalism has steadily dropped its baggage of stakeholders, with the exception of senior corporate officers in first place and stockholders in second. Interest in local communities, cities, states, and countries of origin has been largely put aside as has the previous jewel in the crown of responsibilities to workers, the defined benefit pension fund. At a time of provable abnormally high corporate profits as a percent of GDP, corporations have argued that defined benefit pensions are not affordable. That they are dropping them should come as no surprise, for defined contribution plans (in general less attractive to employees than defined benefit plans) are much cheaper and easier on accounting predictability. What is surprising is why they adopted defined benefit plans in the first place, when they did not have to. And why did they have, in the 1935 to 1985 window, a sense of a social contract, suggesting that other things mattered besides maximizing short-term profits? Good ethics but bad capitalism? Actually, my colleague, James Montier, argues that a single-minded emphasis on relatively short-term share value maximization is a bad business idea; and I agree. Loyalty from workers, community, and country and an image as a company with worthwhile values is very probably a better business proposition. A longer-term focus certainly is. The best strategy, as Montier argues, is probably to concentrate on the highest possible customer satisfaction at a reasonable profit.

A particularly expensive development for society and GDP as a whole is the current corporate fad for rewarding senior executives with a compensation mix that is almost 80% bonus, most of which is comprised of stock option awards. These options are typically badly accounted for and not tied to average industry performance. In fact, there is usually no performance target for these “incentive” awards. This pattern has meshed very well with the policy of the current Fed regime – now internationalized – of encouraging higher stock prices so that the resulting wealth effect can help the economy. Since Greenspan’s early days, this has led to long, drawn-out six- to eight-year bull markets, interrupted with short bear markets. What could possibly be better for a stock option culture (as Andrew Smithers calls it)? In a decline, they rewrite their options. In a market advance, senior corporate officers cash in again and again, basically diluting stockholders’ value. They do this, all the time knowing that the Fed’s well-known asymmetry is on their side: Stumble and we at the Fed (and the Treasury, if necessary) will immediately help out – interest rate declines in early 2000 and 2008 and the giant 2008-09 bailouts are great examples – but succeed and we will not interfere, even in the midst of the most extreme housing or tech bubble.

This near-perfect synergy between Fed policy and the stock option culture has, not surprisingly, resulted in most of the corporate cash flow of public companies being used for stock buybacks – a record $700 billion annualized rate this year at the expense of corporate investments in expansion. Thus, well into the seventh year of economic expansion, we have uniquely had no hint of a surge in capital spending, which remains well below average. And why should we be surprised? For how risky it is to build new factories and shake them down in a world where things can go wrong and corporate raiders lurk. How safe it is to buy your own stock and how likely that doing so will push prices higher, thus increasing option values (making it easier for CEOs to go from earning 40 times the average worker in 1965 to over 300 times today) and enlarging the Fed’s wealth effect at the same time!

But the downside is less corporate expansion; less GDP growth; lower job creation, and hence lower wages. Pretty soon, Mr. Ford, there will be no one to buy your cars. The economy becomes persistently disappointing for yet one more reason.

The good news is that this is all easily corrected. Bonus payments over 30% of remuneration could be made non-tax-deductible to the corporation. All options could be five plus years and all tied to actual outperformance, not simply to a rising tide that lifts all incomes. And life could be made really simple by having corporations buy actual offsetting options at market price and then expensing that actual known cost. (Currently they deduct the cost of buying an option without actually buying one. This introduces a fictional charge if the option expires worthless, but dramatically understates the cost to stockholders if the stock soars.) You can mix and match and add your own improvements. It is not difficult. But if not addressed, this problem could be another Achilles heel for capitalism, which is beginning to look like Achilles the Centipede. Fortunately, it does not apply to private companies, which continue to capital spend and therefore will gain market share. But that is a long, slow arbitrage process.

I realize that those of us capitalists who would like to be proud of our capitalist system are not going to get back the glory days of the 1960s when there was over 4% productivity growth per year and roughly the same substantial growth in all incomes, from CEOs to floor sweepers. But we should complain, I think, when the capitalist machine starts to malfunction. And it is.

(My new hero, Pope Francis, had some fairly stinging comments to make on the subject of capitalist failings as well as on climate change. All popes have had defending the poor and the downtrodden and prodding the rich as part of their job description, but this pope has taken to this aspect of his job with particular zeal. His comments on capitalism, income inequality, and mistreating the poor were so vigorous that many right wingers in the U.S., including quite a few Catholics, have called him a Marxist. Pretty soon, if he keeps this up, they will be calling him a Christian.)

P.S. I was invited in the spring of last year to a conference in London on this very topic – “Inclusive Capitalism” – and initially turned it down on the grounds that I thought it was likely to be a celebration of the less bad capitalists (and even in one or two cases, quite good ones). Later on, being told that my more critical views would be welcomed, I agreed to participate. My reception was interesting. The good news was that I was enthusiastically applauded, contrary to the protocol of waiting for all panelists to finish. “Damn it, that was brilliant. Someone had to say it,” said one NGO leader. The bad news was that the enthusiasm came from only 5% or so of the audience. Perhaps much of the remaining 95% of the audience, and certainly the authorities involved, were less than impressed. In fact, as used to happen with Stalin’s photographs, I was disappeared and, alone amongst the speakers, could not be found in the book of the conference. Perhaps I was really never there. It was in any case an effective demonstration that the criticism of capitalism is a sensitive issue and that “inclusivity” has its limits. (For those who can stand even more criticism of capitalism, my speech is reproduced at www.granthamfoundation.org/our-blog.)

8. Deficiencies in the Fed

Recap

A counter-productive job description, badly executed.

9. Investment bubbles in a world that is, this time, interestingly different

Two significant items seem to be different this time. First, profit margins in the U.S. seem to have stopped mean reverting in the old, normal way, and second, some real estate markets have bubbled up and then stayed there at high prices. Both seem surprising events, even against what I would call “the laws of nature,” or at least the usual laws of capitalism. What is going on?

Tentative thesis

When capitalism is left in a pure form, capital, like water, seeks its natural level: Higher than average profits attract more capital and a glut eventually develops, pushing margins back down. Low profits deter capital flows until shortages develop and margins rise. It’s the very essence of capitalism. I used to say that profitability was the most dependably mean-reverting series in finance, and it used to be. When it stops, capitalism is broken, at least partially, and needs fixing as quickly as possible. The process occasionally gets jammed up, but not on its own – it needs some maladjusted, non-free market interference. Let’s start by looking at housing bubbles.

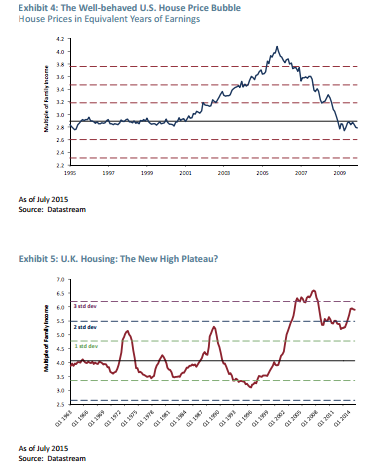

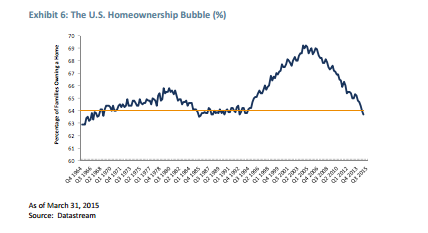

The housing markets are a good example of how the capitalist process can easily be gummed up. In this case, by zoning. As prices rose in the U.S., Spain, and Ireland, home building was allowed to respond. And respond it did, with Ireland and Southern Spain practically sinking under the weight of new housing and the U.S. building up to a million extra homes a year. This will break any bubble, and it did in all three cases. The U.S. bubble (see Exhibit 4) was particularly well-behaved. In contrast, in the U.K. there was no such response to much higher prices as home building was largely unchanged, and the influx of foreign buyers in London sustained the new higher prices. Over the last 10 years or so this has increasingly pushed new buyers out of the inner city and into doubling up, with bad consequences for the local availability of cheap labor (see Exhibit 5). There is always a level of increased housing density that will bring house prices down, and no doubt this will eventually happen in London when the people and businesses are exasperated enough to get politicians, both in central and local politics, to act. But this type of governmental arbitrage is much slower than the unconstrained working of supply and demand, and has far more unintended consequences. A classic example of unintended consequences when policy – not too well thought out – gets in the way of markets is revealed in Exhibit 6, which shows the increase in home ownership in the U.S. The growth in this ratio was artificially stimulated by low rates and low down payments, but now looks set to fall to new lows, below those of the stable 1990s. It looks like a parable on the consequences of interfering with the laws of nature, or at least with a market equilibrium. (The Australian housing situation – very probably a bubble – is very interesting and different from both the U.S. type and the U.K. type and I will cover it another time.)

Now, let’s go back to the similar stickiness in U.S. profit margins, also bouncing along on a seeming new high plateau. I have discussed the interplay of the new stock option culture with its high level of buybacks and how this has reduced the level of capital spending and growth in the economy. Well, here also there are long-winded alternative arbitrage mechanisms, like a heart with clogged major arteries slowly developing a host of widened minor arteries. Private companies with more focus on the long term and more aggressive expansion will have a growing market share. Private equity will also have an incremental long-term advantage: they are already doing more capital spending than traded companies. Venture capital will also have more opportunities than they had previously, when public companies scooped up more of the opportunities. But perhaps slightly faster than this slow capitalist adjustment, businessmen, politicians, and perhaps even some of the more real-world economists will increasingly complain of the current consequences of the stock option culture, especially low growth and low productivity. (Not that this factor will be the only contribution.) And here again, the problem is easy to fix at the corporate level, at least on paper, as already discussed. And what of the current Fed regime – the Greenspan-Bernanke-Yellen Regime – that promotes higher asset prices and lower borrowing costs, which facilitate stock buybacks amongst other speculative forces? Well, this regime, too, will change. Regression of regime, if you will. Painfully, politicians, the public, businessmen, and possibly even some economists will recognize the current regime as a failed experiment. Come back in 30 years and we will of course have a different regime (perhaps even the third or fourth different one), and we can be pretty sure that short interest rates will be between 1 and 2% after inflation once again; asset price manipulation will be seen as a spectacularly painful dead end; and the embedded return on virtually all asset classes up to and including farms and forests will yield 2% a year or so more than they do today, as they have averaged since time immemorial before the Greenspan-Bernanke-Yellen era. But as regressions go, I certainly prefer the easy and quick old-fashioned way of high profits being naturally competed away.

10. Limitations of homo sapiens

Recap

After reading all of this you may think that I am particularly pessimistic. It is not true: It is all of you who are optimistic! Not only does our species have a strong predisposition to be optimistic (or bullish) – it is probably a useful survival characteristic – but we are particularly good at listening to agreeable data and avoiding unpleasant data that does not jibe with our beliefs or philosophies. Facts, whether backed by 97% of scientists as is the case with man-made climate change, or 99.9% as is the case with evolution, do not count for nearly as much as we used to believe. For that matter, we do a terrible job of planning for the long term, particularly in postponing gratification, and we are wickedly bad at dealing with the implications of compound math. All of this makes it easy for us to forget about the previously painful market busts; facilitates our pushing stocks and markets on occasion to levels that make no mathematical sense; and allows us, regrettably, to ignore the logic of finite resources and a deteriorating climate until the consequences are pushed up our short-term noses.

10.5. The good things in “The Race of our Lives”

In the interest of full disclosure, I do obsess also about the remarkable acceleration in helpful technologies – mainly in alternative energy but also in agriculture – that may just save our bacon. It would be a shame, however, to spoil the uniform tone of this quarter’s discussion, so I will wait a quarter to update the many positive developments.

Have a good summer.

1 Deborah Gordon et al., “Know Your Oil,” Carnegie Endowment.org/pubs (no cost!)

2 World Wildlife Fund, “Living Planet Report,” September, 2014.

3 National Audubon Society, “Audubon’s Birds and Climate Change Report: A Primer for Practitioners,” Contributors: Gary Langham, Justin Schuetz, Candan Soykan, Chad Wilsey, Tom Auer, Geoff LeBaron, Connie Sanchez, and Trish Distler, Version 1.2, New York, 2014.

4 Science Magazine, “Marine Ice Sheet Collapse Potentially Under Way for Thwaites Glacier Basin, West Antarctica,” Vol 344, no. 6185, pp 735-738, May 12, 2014.

5 Kevin Trenberth et al., Nature Communications, April 26, 2015.

6 David Horton et al., Nature, April 30, 2015.

7 P. Grassini, K.M. Eskridge, and K.G. Cassman, "Distinguishing Between Yield Advances and Yield Plateaus in Historical Crop Production Trends," Nature Communications 4, Article #2918, December 17, 2013, http://www.nature.com/ ncomms/2013/131217/ncomms3918/full/ncomms3918.html.

8 Aled Jones, Global Sustainability Institute of Anglia Ruskin University.

9 Ibid.

10 Dan Ariely, “Americans want to live in a much more equal country (they just don’t realize it),” Atlantic Monthly, August 2, 2012.

11 Martin Gilens and Benjamin Page, “Testing Theories of American Politics: Elites, Interest Groups, and Average Citizens,” Perspectives on Politics, September, 2014.

Disclaimer: The views expressed are the views of Jeremy Grantham through the period ending July 2015, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2015 by GMO LLC. All rights reserved.

© GMO