KEY TAKEAWAYS

· As the currency of the world’s largest economy and largest exporter, the dollar naturally plays a dominant role in international transactions.

· We expect the dollar to remain the dominant global currency for the foreseeable future.

· The likelihood that the Fed begins to hike rates by December 2015 suggests continued dollar strength.

The U.S. dollar remains strong, defying some skeptics. As has been the case since late 2008 when the Federal Reserve (Fed) began its quantitative easing (QE) program, there has been a great deal of concern recently among some market participants that the dollar is on the verge of a significant decline. Although the dollar may have lost some market share relative to other global currencies in recent decades, it remains the dominant global currency (often referred to as a reserve currency) and we expect it to remain so for the foreseeable future.

WHY ALL THE ATTENTION?

The U.S. dollar is getting a lot of attention these days for many reasons. The dollar’s strength this year (+7% year to date based on the DXY U.S. Dollar Index) has had a negative impact on earnings for U.S.-based multinationals and contributed to fears of an “earnings recession” (not our expectation). Commodities, which trade in dollars globally, have been under pressure from the dollar’s strength beyond the impact of fundamental factors such as the slowing Chinese economy and oil’s high-profile global supply glut. Finally, some are worried that the dollar may lose its place as the leading reserve currency, which we discuss below.

The dollar matters, as we acknowledged in our Weekly Market Commentary, “Dollar Strength Is a Symptom, Not a Cause” (March 16, 2015), and there are legitimate reasons to pay attention to it. But a look at fundamentals suggests nothing more than a slow, gradual decline for the dollar over a very long period.

RELATIVE GAME

Before making the case for “King Dollar,” as Larry Kudlow and others have referred to it, keep in mind currencies are a relative game. The dollar’s moves are dependent upon the other leading global currencies, which are driven by economic growth, interest rates, and inflation, among other factors, in these various countries and regions.

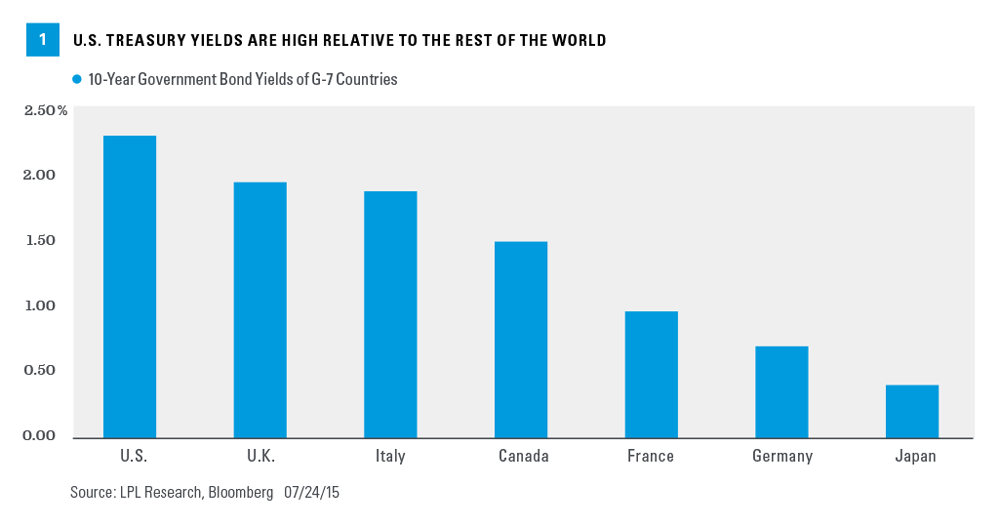

For example, U.S. Treasury yields are very low by historical comparison right now, which could be viewed as bearish for the dollar. But because currencies are relative and U.S. rates are high compared with yields in Europe and Japan [Figure 1], U.S. rates may actually be contributing to dollar strength. Many central banks are pursuing looser policies than the Fed, which, in some respects, is canceling out the impact of the Fed’s monetary support for the U.S. economy on the dollar.

Currency risk is a form of risk that arises from the change in price of one currency against another. Whenever investors or companies have assets or business operations across national borders, they face currency risk if their positions are not hedged.

In the near term, monetary policies of several other major economies contrast with that of the U.S. and may continue to provide support for the value of the dollar in world markets. The Fed is preparing to raise interest rates, while many central banks around the globe are doing the opposite and lowering interest rates, or are clearly focused on maintaining interest rates at very low levels. Among our largest trading partners, both the European Central Bank (ECB) and Bank of Japan (BOJ) are aggressively easing and, in the case of Japan, may do more. The Bank of England (BOE) maintains a zero interest rate policy and may not begin to raise rates until well into 2016. The central bank of our largest trading partner, the Bank of Canada, looks to be on hold for the foreseeable future with a bias toward more easing, as Canada’s economy struggles along with other commodity-producing nations. The likelihood that the Fed begins to hike rates by December 2015 suggests continued dollar strength.

STRONG TRADE POSITION

Another concern raised by those worried about the U.S. dollar is that countries with large holdings of Treasuries (and therefore dollars) like China, Japan, and, to a lesser extent, Russia, will suddenly sell all of these holdings in the open market for either political reasons (disagreements with the U.S.) or economic reasons (loss of confidence in the U.S. economy, the Fed, Congress, etc.). Our view remains that a major shift in China’s, Japan’s, or even Russia’s holdings of dollars and Treasuries is unlikely given the tight trade linkages between the countries. In addition, some countries fear the impact on their own currencies and export markets if they sell dollars, especially where growth is uncertain. Over years and decades, foreign economies are likely to continue to move away from the dollar and Treasuries — a trend that has already been in place for some time now, the dollar losing ground against major trading partners since the early 1970s — but a move out of dollar holdings all at once would not be in the best economic interest of the selling country.

In addition, as the world’s largest exporter, the U.S. produces many goods and services the rest of the world wants to buy, and they ultimately need dollars to do it. The U.S. does run a trade deficit, but the trade deficit is narrowing, helped by increased U.S. energy production (as is the budget deficit, reducing the U.S. borrowing needs on the margin, which also provides incremental support for the dollar). The U.S. is still the world’s largest economy by a wide margin, so most global trade is denominated in dollars, making the dollar the world’s “reserve currency.”

RESERVE CURRENCY STATUS

As the currency of the world’s largest economy and largest exporter, the dollar naturally plays a dominant role in international transactions. The dollar has been a stable currency and the U.S. a politically stable nation, with large, liquid, and open debt markets. The dollar remains a “safe-haven” currency, as are dollar-denominated U.S. Treasury notes and bonds. In times of economic and political uncertainty around the globe, the dollar normally rises in value, as investors must use dollars to purchase Treasuries, the ultimate safe-haven asset.

Other candidates for the dominant reserve currency all have important deficiencies. The British pound and the Swiss franc have the stability but not the size; the Japanese yen and euro do not have the same stability. Countries that have authoritarian regimes (China, Russia) lack political stability, currency stability, and liquid open financial markets. Although the Chinese government is working to boost the acceptance of the Chinese yuan globally (and would like to see its currency added to the International Monetary Fund’s [IMF] Special Drawing Rights program), it has yet to gain acceptance as a reserve currency. China’s interest in increasing the profile of its currency at this point may be a matter of national pride but has little economic impact.

====================================================================================================

SIDEBAR: What are IMF Special Drawing Rights (SDR)?

SDRs represent a claim on a basket of currencies and its value comes from the currencies that back it. At present, currencies backing SDRs are the dollar, the yen, the euro, and the pound. These four currencies are, or have characteristics of, reserve currencies. SDRs are not a currency. Private individuals and corporations cannot hold SDRs or use them to make transactions of any kind. Countries can use SDRs, but their only value comes from the willingness of IMF member countries to accept and use them. They represented just 2.4% of global reserves as of April 2015.

====================================================================================================

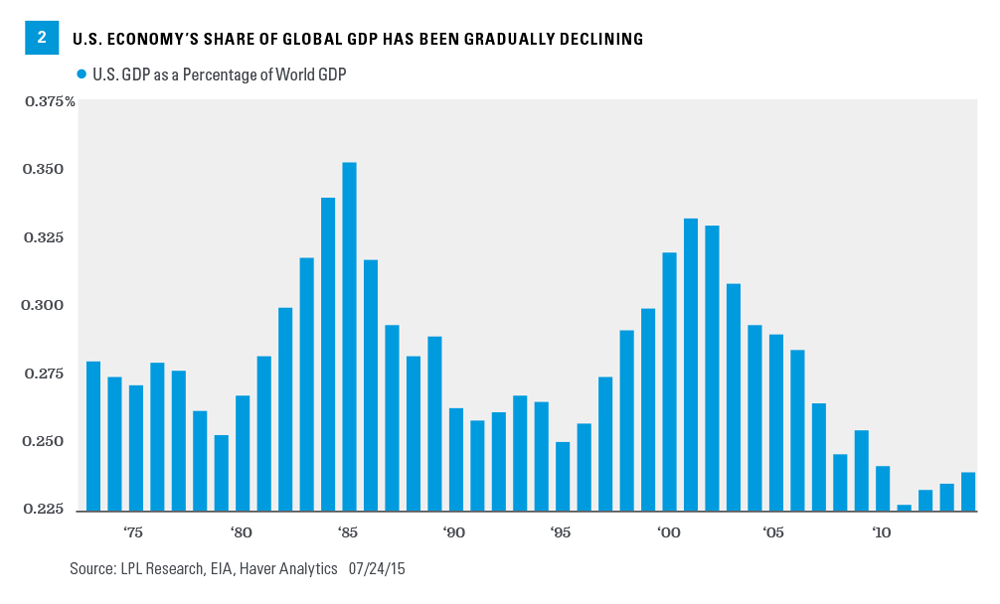

Although the size of the U.S. economy relative to the global economy has shrunk [Figure 2], U.S. share of global GDP has not moved much in 40 years even as China’s economy grew, and those changes have already been having an impact on the global importance of the dollar, despite its still dominant role. While these changes will continue over time, the process will be slow, as it has been, and sudden changes in the size, importance, or stability of the U.S. economy are extremely unlikely.

CONCLUSION

The U.S. dollar has been getting a lot of attention recently for many reasons. Although the rise of the Chinese economy, along with the size of the Eurozone economy, may have slightly eroded the dollar’s “reserve currency” status in recent years, the U.S. still plays a preeminent role in the global economy and our “good old American know-how” knowledge-based service sector remains a world leader. As the currency of the world’s largest economy and largest exporter, the dollar naturally plays a dominant role in international transactions, and we expect it to remain the dominant currency for the foreseeable future.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

Investing in foreign and emerging markets securities involves special additional risks. These risks include, but are not limited to, currency risk, geopolitical risk, and risk associated with varying accounting standards. Investing in emerging markets may accentuate these risks.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond and bond mutual fund values and yields will decline as interest rates rise and bonds are subject to availability and change in price.

Government bonds and Treasury bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

Commodity-linked investments may be more volatile and less liquid than the underlying instruments or measures, and their value may be affected by the performance of the overall commodities baskets as well as weather, geopolitical events, and regulatory developments.

DEFINITIONS

Quantitative easing (QE) refers to the Federal Reserve’s (Fed) current and/or past programs whereby the Fed purchases a set amount of Treasury and/or Mortgage-Backed securities each month from banks. This inserts more money in the economy (known as easing), which is intended to encourage economic growth.

The U.S. Dollar Index (DXY) indicates the general international value of the U.S. dollar. The DXY Index does this by averaging the exchange rates between the US dollar and six major world currencies