Following Fed Chair Janet Yellen’s monetary policy testimony in mid-July, the odds of a September rate hike seemed about even. That doesn’t mean that the Fed’s decision would be a toss-up at the time of the meeting. When the September 16-17 policy meeting rolls around, it should be pretty clear what the Fed will do (or not do). Rather, that policy outlook reflected the uncertainty in the economic data that would arrive between now and the September FOMC meeting. However, just two weeks later, the evidence is pointing to a likely delay.

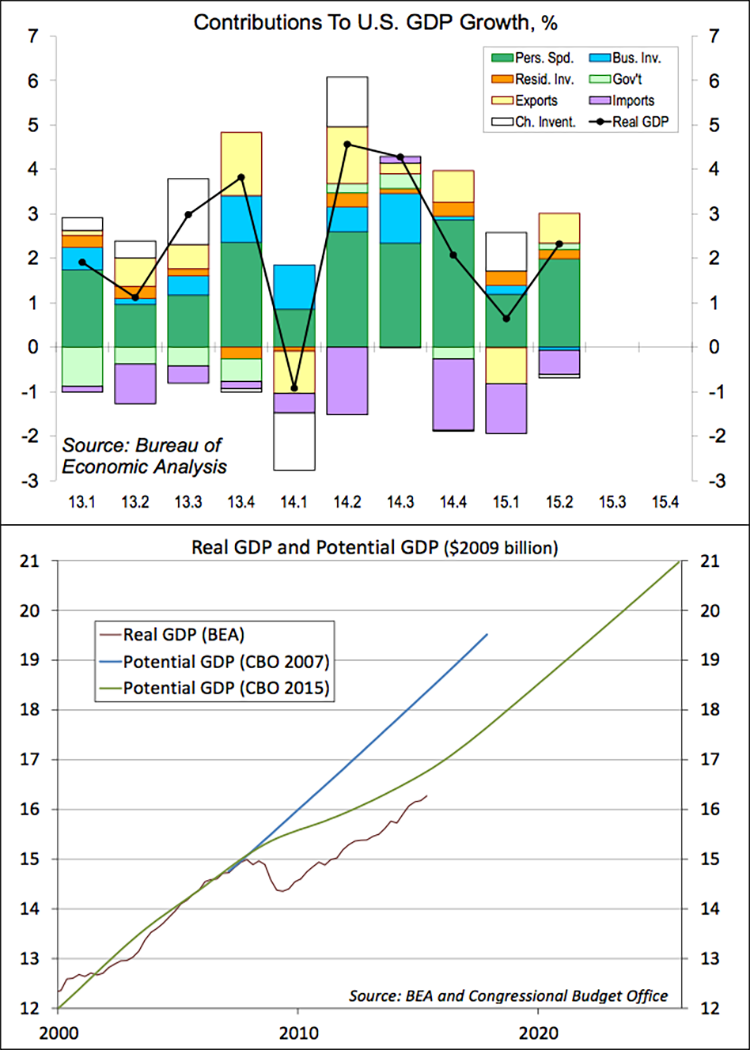

Real GDP rose at a 2.3% annual rate in the advance estimate for 1Q15. No surprise, consumer spending was strong (led by strength in durables) and business fixed investment was soft (partly reflecting a further drop in energy exploration). The Bureau of Economic Analysis introduced a new aggregate: final sales to domestic purchasers (a 2.5% pace in 2Q15). This is simply GDP less net exports, the change in inventories, and government. These components are normally noisy, but did not make much of a contribution either way in the second quarter.

Annual benchmark revisions reduced the reported pace of growth over the last few years, with most of that concentrated in 2013 (coincidentally, that was when tighter fiscal policy subtracted about 1.5 percentage points from growth). As a result, GDP is currently 2.9% below the Congressional Budget Office’s estimate of potential GDP. The CBO’s estimate of potential GDP is a bit fuzzy. However, GDP is still over 11% below the trend that was in place before the recession. The output gap (the difference between GDP and potential GDP) is being reduced, but it is still relatively high – more importantly, higher than it appeared to be before the GDP revisions.

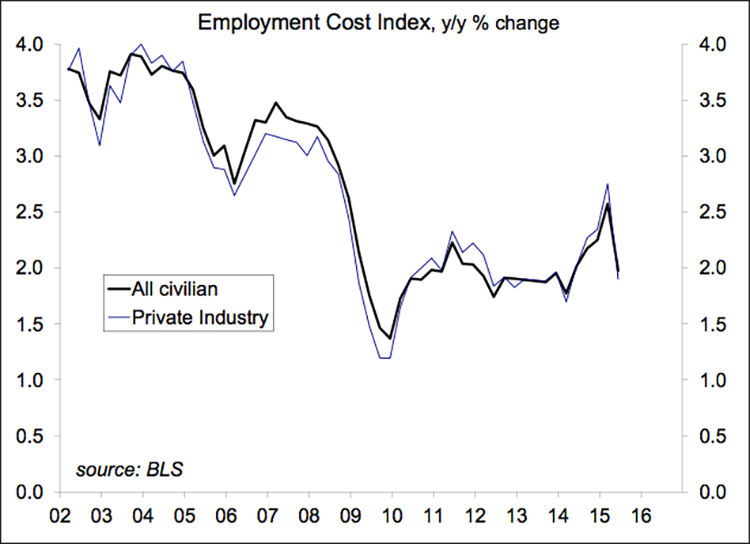

Clearly, the Fed is not going to rely solely on estimates of the output gap in setting policy. The focus has been on the underutilization of labor resources. While the unemployment rate has come down, improvement has been exaggerated due to low labor force participation. There are other signs that the slack in the job market is being reduced, and we should see further evidence in Friday’s employment figures for July. However, a considerable amount of slack remains. This slack is reflected in labor compensation. The Employment Cost Index is the best measure (although one still has to factor in labor productivity growth to calculate the inflationary impact). The ECI popped higher in the first quarter, but the second quarter gain was mild, bringing the year-over-year gain back below 2%. A year ago, Fed Chair Yellen highlighted the “lackluster” growth in labor compensation as evidence of labor market slack. The pace still appears to be relatively lackluster.

The ECI data should put the odds of a September hike well below 50%. Still, the more important issue is the pace of tightening over the next few years. In June, the Fed inadvertently posted staff projections on its website. The Fed staff forecasted a 1.26% federal funds target rate average for 4Q16 and a 2.12% in 4Q17 – in other words, “gradual.”