Investors remained focused on Federal Reserve policy last week. Economic data continue to be mixed, but suggest that Fed action should occur sooner rather than later. U.S. equity markets were dominated by a sharp sell-off in media stocks and continued weakness from Apple and the biotechnology sector.1 Commodity prices also experienced ongoing declines.1 U.S. equities finished the week lower, with the S&P 500 Index falling 1.2%.1 The energy and consumer discretionary sectors were the worst-performing areas, while utilities was the lone sector to experience positive returns.1

Key Points

- U.S. economic data continue to be mixed, but we believe the economy has improved enough that the Fed should raise rates.

- A combination of stronger global economic growth and improved investor sentiment should allow equities to move higher, breaking out of their trading range.

Weekly Top Themes

1. The July employment report was solid and may put additional pressure on the Fed to raise rates in September. The headline numbers showed that 215,000 new jobs were created last month and the unemployment rate remained unchanged at 5.3%.2 However, wage levels are languishing, as average hourly earnings rose by a less-than-expected 0.2%.2

2. The U.S. service sector appears to be surging. The ISM non-manufacturing survey rose to 60.3 in July, its highest level since August 2005.3 Strength was broad-based, with business activity, new orders and employment all coming in well ahead of expectations.3 The strength in employment is particularly welcome and should put upward pressure on consumer spending.

3. The U.S. deficit is falling, but may drift higher over the coming years. The fiscal year 2015 budget deficit should drop to around $425 billion, or 2.4% of U.S. gross domestic product.4 This level would be well below the 40-year average of 3.2%.4 Absent significant entitlement reform (which seems unlikely), we expect federal deficits will rise gradually over the next 10 years as spending exceeds revenues, but not to the levels that will trigger a meaningful crisis.

4. Equities have been trading in a very narrow range in 2015. According to Strategas Research, the S&P 500 Index trading range has been confined to less than 8% this year. That is one of the narrowest bands in the last 90 years.

5. Investor uncertainty remains elevated, but we expect sentiment will improve. Issues such as the Greek debt crisis, a possible hard landing in China, uneven growth in the United States and questions around Fed policy have kept investors on edge. In some ways, we find it surprising that unease is so high considering U.S. stock prices are only a few percentage points below their all-time highs.

We believe defensiveness and uncertainty will be replaced by growing confidence in the coming months as the economic and earnings backdrop solidifies.

Risks Remain, but Positives Outweigh Negatives

Since the end of the Great Recession, investors have enjoyed a combination of weak-but-positive global economic growth and highly stimulative monetary policy. This backdrop has produced an incredibly strong equity bull market, with equities outpacing bonds and other asset classes. At this point, financial markets may have reached a crossroads, with the Federal Reserve poised to begin a cycle of interest rate increases. Investors may wonder if the party is over for the equity markets.

A number of risks could conspire to end the equity bull market. Economic weakness in China and the resulting market volatility remain an issue, as does the path of Greece and the eurozone. Global trade is not as strong as it could be, and many countries are facing mounting debt pressures. Additionally, investors need to be on the lookout for the possibility of a sharp rise in bond yields, which could spook equity markets.

In all, however, we expect the positives will win out. The global economy has proven to be resilient to a number of shocks over the last few years, and we believe the economy is strengthening. In the United States, we think the weakness we saw in the first quarter will prove to be an anomaly and signs point toward an acceleration in economic growth. When the Fed finally acts, we think rising rates will put pressure on bonds. However, as long as rates rise gradually (which we expect), equities should be able to push ahead. Volatility may rise and the pace of gains is unlikely to match what we have seen in recent years, but we remain convinced that investors would do well to hold overweight positions in equities.

1 Source: Morningstar Direct, as of 8/7/15

2 Source: Bureau of Labor Statistics

3 Source: Institute of Supply Management

4 Source: Bank of America/Merrill Lynch Research

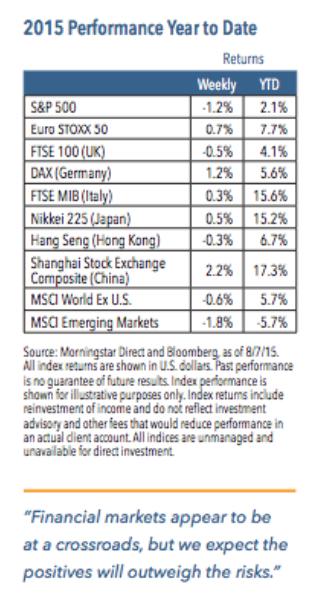

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

©2015 Nuveen Investments, Inc. All rights reserved