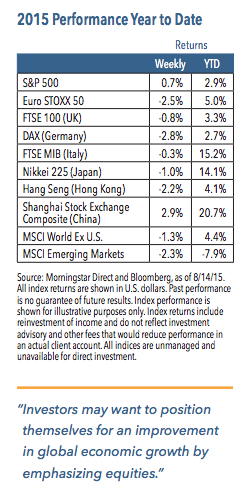

U.S. equities endured high levels of volatility last week, dropping sharply in the first few days of trading before recovering to end the week slightly higher. The main focus was China’s surprising decision to devalue the yuan, which raised concerns about a weaker global growth backdrop, deflationary trends, the prospects of a currency war and what the move would mean for the U.S. Federal Reserve and U.S. monetary policy. Sentiment improved by the end of the week as these concerns faded, and the S&P 500 Index managed to gain 0.7%.1 The energy sector outperformed despite continued downward pressure on oil prices, while the consumer sectors, health care and financials lagged.1

Key Points

▪ The devaluation of the yuan roiled financial markets, but we do not believe it will trigger a currency war or widespread deflation.

▪ Global growth continues to decouple, with the U.S. economy looking healthier than other regions.

▪ We think investors should hold overweight positions in equities, with an emphasis on domestically-oriented companies.

What Does Slower Growth in China Mean for Investors?

China’s currency devaluation came as a surprise, and caused a broad “risk-off ” move across financial markets as equity prices fell, bond yields declined and credit spreads widened.1 Chinese economic growth has been slowing for some time, and in our opinion, the country’s economy is not growing as quickly as officially-reported results. Chinese corporate profits are down, consumer spending is slowing, excess inventories are building and China is experiencing net capital outflows.2 The devaluation of the yuan is the latest evidence that growth is weakening.

We expect Chinese officials will engage in further action to stimulate their economy, with rate cuts and fiscal stimulus moves likely on the horizon. China is slowly de-linking its currency from the U.S. dollar (possibly creating the basis for an Asian currency bloc), which should put upward pressure on the dollar and downward pressure on commodity prices. Weakness in China may also put a damper on multinational corporate earnings. As far as Fed policy, the situation may provide ammunition for those who want to delay rate increases, but we lean toward the view that it is more likely than not that the Fed will raise rates next month.

Weekly Top Themes

1. Retail sales are accelerating. Sales increased by 0.6% in July and data for June and May were revised upward.3 We expect consumer spending levels to increase in the months ahead.

2. U.S. economic growth looks healthier than most other regions. In our view, European growth is improving but remains mixed, Japan is struggling with anemic wage levels, China’s economy is faltering and both Russia and Brazil are experiencing sharp economic declines.

3. We believe domestically-oriented corporations should benefit from global economic decoupling. Outside of the energy industry, we expect U.S. companies will benefit from lower oil prices and relatively solid U.S. economic growth. In contrast, multinationals and companies that derive more of their revenues from overseas may be hurt by slowing growth in other regions. We have been seeing these trends reflected in earnings results and expect this divergence to persist.

Despite Ongoing Deflation Scares, Global Growth Continues to Slowly Improve

China’s currency devaluation is the latest event to raise fears about deflationary risks. Uneven global growth and recessions in some regions, debt crises, the recent implosion in oil prices and the corresponding surge in the U.S. dollar have all triggered these concerns. In our view, however, the global economy is gradually and unevenly improving, and we think it will be able to overcome the latest deflationary road bump. Policymakers around the world are focused on promoting economic growth, and global monetary policy remains extraordinarily supportive.

We acknowledge that periodic growth scares are likely to persist, but we would also recommend that investors position themselves for continued economic growth. The turmoil in China and the corresponding renewed drop in oil prices is a legitimate concern, but it is not one that we expect will derail the equity bull market. Government bond yields around the world are priced for a very bearish economic environment and in our view appear unattractive, which is one reason we think it makes sense to hold overweight positions in equities. Equities may no longer be as inexpensive as they were a few years ago, but we believe they are reasonably attractive and offer better value than other asset classes. Investor sentiment remains depressed, but we think pessimism has been slowly fading for some time. Looking ahead, we expect confidence levels to rise.

1 Source: Morningstar Direct and Bloomberg, as of 8/14/15

2 Source: Cornerstone Macro

3 Source: Commerce Department

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

©2015 Nuveen Investments, Inc. All rights reserved.