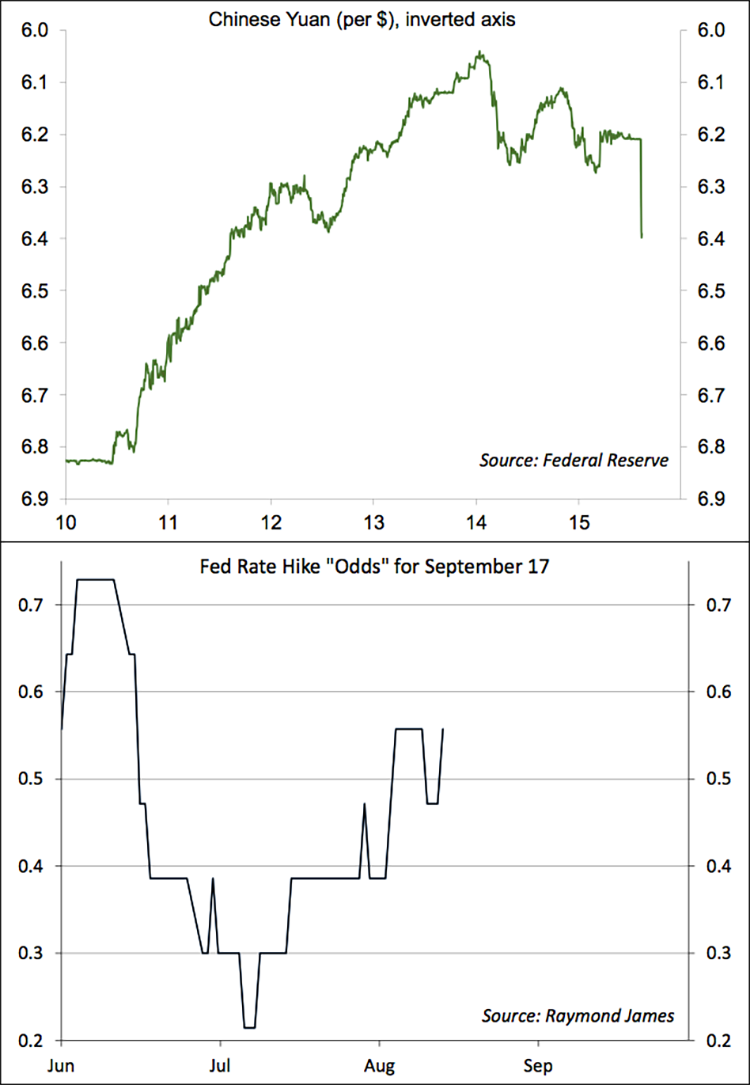

The People’s Bank of China, the country’s central bank, moved to allow its exchange rate to be determined by market forces. After two sharp declines in the yuan, the PBOC apparently had had enough and declared that the currency adjustment was “basically completed.” The news from China added to uncertainty about what the Fed will do in September. Concerns about the pace of global growth have put downward pressure on commodity prices, which may keep the Fed on hold.

China’s leadership wants the yuan to become one of the premier reserve currencies, but that means that the exchange rate will have to be set by the free market. The PBOC allows the currency to trade in a 2% range around a level announced before the market open. The PBOC said it would begin setting that level at the previous session’s close (rather than picking it out of thin air). Investors took the currency down 1.9% after the news and the exchange rate dipped further in the following session, before the PBOC intervened to prop it back up.

The decision to move toward a free market confused global financial market participants. The financial press described it as “a devaluation” and some viewed it as “the start of a currency war.” Granted, China’s currency has had a strong tie to the U.S. dollar, which has become harder for the country’s exporters as the greenback has strengthened over the last year. However, the decision to intervene suggests that the PBOC had badly misjudged market forces and the likely reaction to the change. The U.S. market reaction to China’s currency debacle (and to its recent stock market correction) seems way overdone. The more important issue is the slowing in China’s economy.

The market odds of a September 17 rate hike from the Fed have varied considerably in recent weeks. Note that the market odds of a Fed move are not directly observable, because the FOMC will announce a target range for the federal funds rate rather than a specific level. However, if we assume that federal funds will trade around the midpoint of that range, we can use the federal funds futures market to calculate “odds” (I’ll put quotes around that to emphasize the fuzziness of the estimate).

If the trend of improvement in the job market continues, we should be close to normal conditions in late 2016 or in early 2017. Policy is extraordinarily accommodative now and will still be very accommodative after the first few rate hikes, so the Fed would appear to be justified in beginning a gradual process of normalization. However, officials have indicated that they need to be “reasonably confident” that inflation will move toward the 2% goal. Lower commodity prices, lower import prices, and the lack of meaningful wage growth ought to give pause.

Most likely, the FOMC will err on the side of caution and delay. The Fed does not want the initial move to be a surprise for the markets. Fed Chair Yellen will not attend the Kansas City Fed’s annual monetary policy symposium next week, but expect her to add a speech to calendar in the next few weeks.