When policymakers tell you one thing and the data tell you something different, heed the data.

Markets that are in the midst of transition do not behave according to script, despite the best efforts of policymakers to script them. Last week, China loosened control of its currency, resulting in its biggest one-day loss in two decades, compounded by additional losses over the following days. As of this writing, the renminbi (RMB) has depreciated by close to 3 percent since the start of last week. This “surprise” move roiled markets and triggered concern that other central banks would follow suit, but the reality is that the fundamentals were so overwhelming that the People’s Bank of China’s (PBoC) action was practically unavoidable, as I wrote on July 31.

Central banks and policymakers often perpetuate confidence-inspiring narratives in the face of contradictory fundamentals. In this instance, Yi Gang, a vice governor at China's central bank, told investors at a May 22 meeting that given the size of China’s trade surpluses, further currency devaluation would not be necessary. Unfortunately, Mr. Yi’s statement turned out to hold as much water as when then-U.S. Federal Reserve Chairman Ben Bernanke told us in the spring of 2007 that the subprime crisis was a contained and limited event. After allowing the RMB to weaken, the PBoC made the unusual move of hosting a press conference last Thursday to defend its actions and to reiterate that the RMB has made sufficient valuation adjustment that it would not devalue further.

We should know by now that the reality of a situation can be very different to how policymakers package it for public consumption. The problem is they often say exactly what the market wants to hear, not what it needs to know. The lesson to be learned is to trust the fundamental underlying data. In the case of China, the latest weakness in trade data—China’s July exports declined by 8.3 percent year over year, much worse than the 1.5 percent decline expected by the market—would suggest the RMB faces more downward pressure. When policymakers are telling you one thing and the data are telling you something different, heed the data.

Right now, the Fed is telling us that it is going to raise rates soon. I don’t know what the definition of “soon” is, but most players in the market think that soon means sometime this year. Of course, the Fed is conspicuously retaining its data-dependency clause, affording it the privilege to change its mind. Unlike in China, the economic data in the United States is much more aligned with and supportive of policymaker guidance. We are on course for a Fed rate increase this year. Whether the Fed acts or doesn’t act in September or December doesn’t matter—we know it is coming. For investors, there are more pressing matters at hand in almost every other major global market. On top of a slowdown in consumer activity, Europe faces the prospect of a slowing economy due to export demand falling off in China and the uncertainty created by Greece, which probably means that rates in Europe will go lower. Similarly, Japan’s economy will suffer as China, its largest trading partner, loses steam and the devaluation of RMB makes Japanese exports less competitive. The depreciation of the RMB will put more downward pressure on commodity prices, so we are not at the end of the road for industrial metals or energy price declines. Regardless of a Fed rate hike, demand for safe-haven U.S. Treasuries as a result of all this global turmoil could push yields meaningfully lower, even as low as 1 percent. While the data on the U.S. economy is clearly showing softness, which seems to correlate with a drop off in exports of capital equipment to Europe and China, the U.S. economy is nowhere near recession territory.

Uncertainty eventually yields to opportunity, and while it would probably be premature to jump in today, there are places in the world where things are getting cheap enough that they deserve a look. The bottom line is we are now into the dog days of summer. Markets have little new information upon which to act. Given the light volumes and lack of new buyers, risk assets will continue to languish. Risks remain to the downside (lower prices) as new data, especially from overseas, seem more likely to disappoint than to support improvement in economic activity. Negative surprises like the sudden decline in the Malaysian ringgit will continue to put downward pressure on commodity prices, which will probably spill over into both stocks and corporate debt, especially those of commodity companies like energy and mining. We are likely to see credit spreads widen (ground zero will continue to be in the energy sector), stock prices decline, and long-term interest rates rally.

I do not believe the swirling uncertainty portends a giant bear market for risk assets, but we have not had a U.S. equity market correction in over four years—it has been 1,471 days since the last correction started, more than double the historical average since 1928 of 706 days—so we are well overdue. In short, I doubt we have seen the worst. We should not be surprised at this seasonally challenging time to see a meaningful selloff in equities. I would expect that the current downward pressure on risk assets will abate sometime in late September or early October. Until then, the environment should be supportive for longer duration U.S. Treasury notes and bonds. Caution is the watchword.

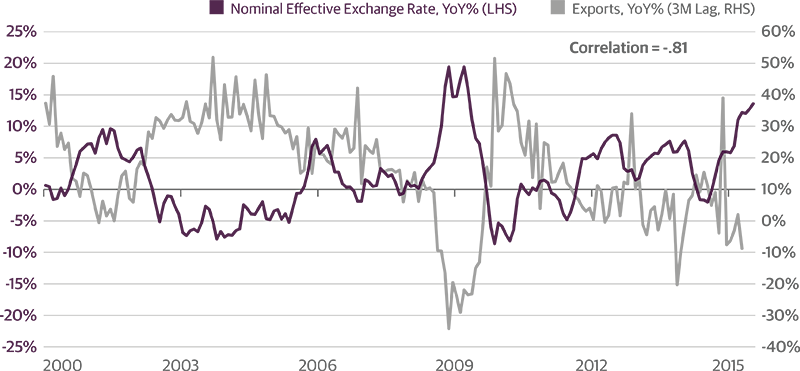

Weaker RMB Is Necessary to Stimulate Chinese Exports

China’s devaluation of its currency may have come as a surprise to some, or interpreted as a market-friendly reform and not a cyclical policy tool. However, the tepid performance of exports over the past year was a clear signal that Chinese policymakers had to take action. With the de facto peg to the dollar, the Chinese currency had appreciated by over 13 percent from July 2014 to July 2015 on a trade-weighted basis. This led to a major slowdown in export growth, an action that the PBoC is now attempting to reverse by letting the RMB depreciate. The graph below shows the strong, inverse correlation between changes in the nominal effective exchange rate and Chinese exports (on a three-month lag).

Nominal Effective Exchange Rate and Exports

Source: Haver, JPMorgan. Data as of 7/31/2015.

Economic Data Releases

Retail Sales Bounce Back in July

- Retail sales came in as expected in July, rising 0.6 percent. Motor vehicle sales were strong, gains in other areas were broad-based, and revisions to prior months suggested stronger activity than previously thought.

- NFIB Small Business Optimism rebounded slightly in July to 95.4 from 94.1. Plans to hire and plans to raise wages both increased.

- Industrial production beat estimates in July, increasing 0.6 percent. Gains were concentrated in auto manufacturing.

- Job openings declined in June, down to 5.249 million from 5.357 million. The hire rate rose to 3.7 percent, the highest this year.

- Initial jobless claims rose by 5,000 for the week ending Aug. 8, up to 274,000.

- The NAHB Housing Market Index ticked up to a new post-recession high of 61 in August, up from 60.

- Productivity growth remained sluggish in the second quarter, rising just 1.3 percent at an annualized rate, following negative readings the prior two quarters.

- Inventories rose 0.8 percent in June, the largest build since January 2013.

- The producer price index rose for a third straight month in July, up 0.2 percent. The year-over-year rate was -0.8 percent.

Euro Zone GDP Disappoints, Chinese Activity Slows

- Euro zone industrial production was weak in June, falling for a second consecutive month, down 0.4 percent.

- Second quarter euro zone real GDP growth was under expectations at 0.3 percent. The disappointment may be attributable to sluggish investment.

- Germany’s real GDP rose 0.4 percent, falling short of the consensus forecast of 0.5 percent.

- The ZEW survey in Germany showed an improved assessment of the current situation in August, rising to a 14-month high of 65.7. The expectations component, however, unexpectedly dropped to a nine-month low.

- French second quarter GDP registered no growth, missing estimates. Consumer spending was weak and business investment contracted.

- Retail sales in China maintained a mostly steady pace in July, inching down to 10.5 percent growth from 10.6 percent.

- Chinese industrial production decelerated in July, falling to 6 percent growth year over year after accelerating for the past three months.

- Japan’s second quarter real GDP contracted at a 1.6 percent annualized rate. Private consumption fell and net exports dragged on growth.

Important Notices and Disclosures

This article is distributed for informational purposes only and should not be considered as investing advice or a recommendation of any particular security, strategy or investment product. This article contains opinions of the author but not necessarily those of Guggenheim Partners or its subsidiaries. The author’s opinions are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC. ©2015, Guggenheim Partners. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information.