Why We Believe the Eurozone is a Land of Opportunity

Executive Summary

- Valuations in the region are compelling relative to other developed economies.

- Quantitative easing has weakened the Euro and made European goods cheaper as compared to U.S. products.

- Consumer confidence is growing and could fuel an uptick in sales among Consumer Discretionary companies.

- Capital expenditures are at historic lows and a rebound would likely have a widespread positive impact on the region’s economy.

For the past few years Europe, including the European Union (EU), has been a place for value investors to window shop but not necessarily buy.

In the years leading up to the financial crisis, valuations in the region were rich relative to the U.S. and the strength of the Euro created additional headwinds. It wasn’t until Europe’s economy began to falter during the past few years that valuations began to soften relative to the still robust levels domestically. However, the depressed valuations more accurately reflected dim prospects for many companies and not an exploitable discount to domestic equities.

We believe now is the time to rethink that stance. Here is why.

The Greece Effect

The negative reaction surrounding the Greek debt crisis has created buying opportunities for equities elsewhere in Europe. It’s true that risks remain—the fragile bailout plan could still falter, leading Greece to exit the European Union, likely escalating selling pressure and causing market volatility to spike. But even in that scenario, with Greece responsible for just 1.3% of gross domestic product (GDP) in the region, we believe the long-term effects are likely to be limited. We also believe current valuations mitigate the downside potential if fallout from Greece were to spread throughout the European economy.

A Weaker Euro Benefits European Exporters

Quantitative easing (QE) from the European Central Bank (ECB) has weakened the Euro. As illustrated, since hitting a five-year peak in the first half of 2011, the currency has slid and hit a recent low, down nearly 30%. The upshot is goods produced in the EU are cheaper relative to products from the U.S. and elsewhere. We believe weakness in the Euro should remain as the ECB only recently started its QE program and has publicly stated it is committed to the approach until at least September 2016.

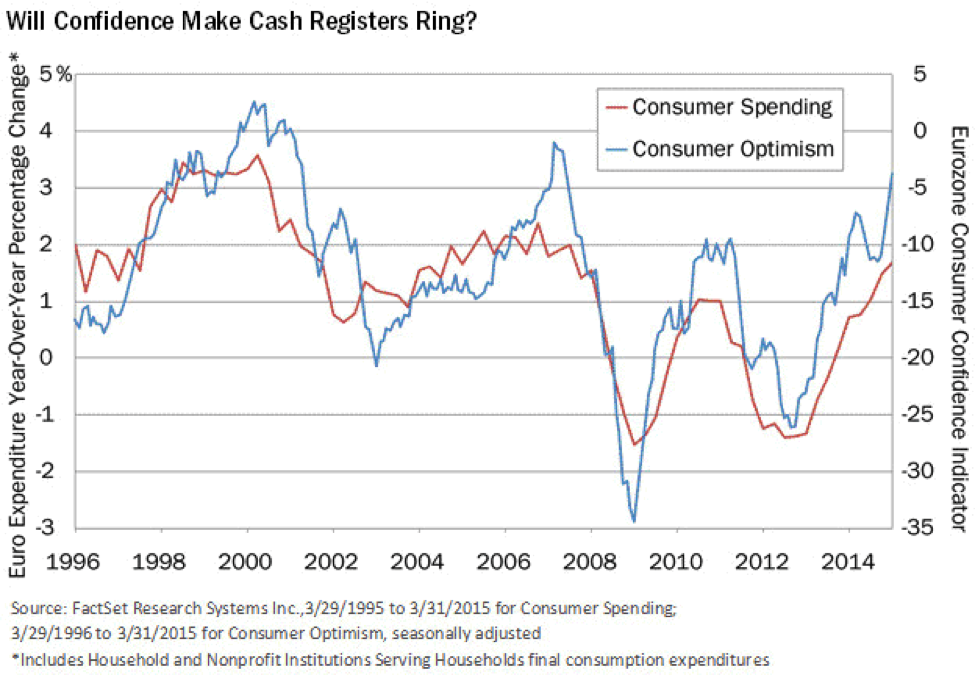

Consumers in a Shopping Mood

While EU products should be better able to compete on price abroad due to the softer currency, they could also benefit at home from upbeat consumers ready to open their wallets for the first time in years. This chart shows consumer confidence is nearing its highest level in five years and spending is inching up. The region is also seeing population growth with an average of 1.3 million new inhabitants each year. The growth is primarily related to immigration meaning many of the new residents of the region are already at the age where they are joining the ranks of consumers. The steady population increase means that consumer spending should enjoy a natural rise even if the rate of purchasing by individuals does not return to previous highs.

D’Ieteren SA (DIE BB) is an example of a Consumer Discretionary name we expect will benefit from an uptick in consumer spending. The company operates in 34 countries through its replacement windshield business and has a market leading position in new car dealerships in Belgium. It also provides auto loans through its dealerships.

At 1.02x 2015 book value, the company is trading at just 75% of its 10-year average rate. We believe investors aren’t fully valuing the benefits of a recent restructuring nor what we believe will be an uptick in sales as the outlook for consumers continues to brighten.

Consumer confidence is also reflected in a growing appetite for bank loans. As unemployment in the region has ebbed, lending activity has picked up, particularly in consumer credit and mortgages. The use of debt often bodes well for consumer durable companies such as furniture and appliance makers but also for retailers that benefit from increased sales tied to credit card usage.

Corporate Borrowing Poised to Expand?

Corporate borrowing continues to lag demand from consumers, but we think that is likely to change. At less than 15% of GDP for the eurozone, capital expenditures (capex) are near a 20-year low and below the long-term average. As the economy picks up, we believe companies will replace old equipment and buildings and expand their operations to capitalize on growing demand. Many of the businesses will tap credit lines to pay for the retooling. The nature of business investment should also be appealing to investors. Unlike in the U.S., where nearly a third of capital expenditures are tied to Energy, the sector represents a much smaller portion in Europe. Instead, construction and real estate make up the greatest portion of fixed investment meaning the level of capex activity is less dependent on a single industry. As business spending rebounds, the moves will likely benefit companies in Industrials, Materials, and Information Technology (IT), among other sectors.

For example, we expect holding KSB Group (KSB GR) will build on its recent uptick in revenue. The maker of pumps and valves for use in building services, water utilities, and the Energy and Mining sectors, reported 5% top line growth in its most recent report. With nearly half of its revenues tied to industry and building services, an increase in capital expenditures could have a dramatic effect on company sales. In its earnings release, management noted that demand was beginning to rise and that it continues to target significant sales growth for the year.

Depressed Valuations Relative to U.S. Counterparts

While we believe there are several avenues that could lead to an uptick in prospects for companies in the eurozone, for prudent investors, the names only represent an opportunity if they are trading at compelling valuations. Using two widely followed indices as a proxy for valuations, we believe stocks in the region satisfy the requirement.

The Russell® Developed Eurozone Index, which reflects large- and mid-cap companies in the ten largest countries in the European Economic Monetary Union, trades at 2.1x book value and 9.5x 2016 weighted average enterprise value to earnings before interest, taxes, depreciation and amortization (EV/EBITDA). By contrast, the Russell 3000® Index trades at 3.4x book value and 12.0x EV/EBITDA for 2016. The upshot is that eurozone stocks are trading at a 39% discount to counterparts in the U.S. based on book value and more than 20% discount based on EV/EBITDA.

Looking at small-cap stocks—where we focus much of our attention—the numbers tell a similar story. On a price-to-book basis the Russell® Small Cap Developed Eurozone Index is trading at a 22% discount to the Russell 2000® Index and a 30% discount based on 2016 EV/EBITDA.

In many ways, we view opportunities in Europe similar to those seen domestically a few years ago. We anticipate economic growth will be measured and persistent and that the recovery could last for an extended period. Valuations do not, in our view, accurately reflect future prospects and, as a result, we view the region as a source of sound investment ideas.

Disclosure:

Past performance does not guarantee future results.

An investor should consider the Fund’s investment objectives, risks, and charges and expenses carefully before investing or sending money. This and other important information can be found in the Fund’s prospectus. To obtain a prospectus, please call 800-432-7856 or visit heartlandadvisors.com. Please read the prospectus carefully before investing.

The International Value Fund invests primarily in small foreign companies selected on a value basis. Such securities generally are more volatile and less liquid than those of larger companies. Foreign securities have additional risk, including but not limited to, exchange rate changes, political and economic upheaval, and relatively low market liquidity. These risks are magnified in emerging markets. Value investments are subject to the risk that their intrinsic values may not be recognized by the broad market.

The statements and opinions expressed in this article are those of the presenter(s). Any discussion of investments and investment strategies represents the presenter’s views as of the date created and are subject to change without notice. The opinions expressed are for general information only and are not intended to provide specific advice or recommendations for any individual. The specific securities discussed above, which are intended to illustrate the advisor’s investment style, do not represent all of the securities purchased, sold, or recommended by the advisor for client accounts, and the reader should not assume that an investment in these securities was or would be profitable in the future. Any forecasts may not prove to be true. Certain security valuations and forward estimates are based on Heartland Advisors’ calculations. Economic predictions are based on estimates and are subject to change.

As of June 30, 2015, D’Ieteren SA and KSB Group represented 2.64% and 1.57% of the International Value Fund’s net assets, respectively. Statements regarding securities are not recommendations to buy or sell. Portfolio holdings are subject to change. Current and future holdings are subject to risk. Portfolio holdings are subject to change.

Industry and sector classifications are generally determined by referencing the Global Industry Classification Standard Codes (GICS) developed by Standard & Poor’s and Morgan Stanley Capital International.

Heartland Advisors considers large-cap companies to be larger than $15 billion in market cap, mid-cap companies to be between $2 billion and $15 billion, small-cap companies to be between $300 million and $2 billion, and micro-cap companies to be less than $300 million. The above breakdown does not include short-term investments.

Definitions: Book Value: is the sum of all of a company’s assets, minus its liabilities. Eurozone is the geographic and economic region that consists of all the European Union countries that have fully incorporated the euro as their national currency. Eurozone Consumer Confidence Indicator is the arithmetic average of the balances (%) referring to the questions on the financial situation of households, general economic situation, unemployment expectations (with inverted sign) and savings; all over next 12 months. Enterprise Value (EV): is the entire economic value of a company. Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA): measures a company’s financial performance. It is used to analyze and compare profitability between companies and industries because it eliminates the effects of financing and accounting decisions. Gross Domestic Product (GDP): is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. Price/Book Ratio: of a company is calculated by dividing the market price of its stock by the company's per-share book value. Quantitative Easing: is a government monetary policy occasionally used to increase the money supply by buying government securities or other securities from the market. Russell 3000® Index: is a market capitalization weighted equity index maintained by the Russell Investment Group that seeks to be a benchmark of the entire U.S. stock market and encompasses the 3,000 largest U.S.-traded stocks, in which the underlying companies are all incorporated in the U.S. Russell® Developed Eurozone Index: measures the performance of the investable securities in developed countries in the Euro Zone, is constructed to provide a comprehensive and unbiased barometer for this market segment, and is completely reconstituted annually to accurately reflect the changes in the market over time. Russell Small Cap Developed Eurozone Index: offers investors access to the small-cap equity universe of developed countries across the Eurozone. All indices are unmanaged. It is not possible to invest directly in an index.

Data Sourced from FactSet: Copyright 2015 FactSet Research Systems Inc., FactSet Fundamentals. All rights reserved. There is no guarantee that a particular investment strategy will be successful.

Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of the Frank Russell Investment Group.

Robert Sharpe and Mike Jolin are registered representatives of ALPS Distributors, Inc. The Heartland Funds are distributed by ALPS Distributors, Inc.

CFA is a trademark owned by the CFA Institute.

©2015 Heartland Advisors heartlandadvisors.com

HLF4906/1015