The Correction May Not Be Over, but the Bull Market Should Persist

Key Points

▪ To put the downturn in perspective, the S&P 500 Index has more than tripled since 2009 and is only 7% off its all-time high.1

▪ The S&P 500 has a dividend yield of 2.2%, out-yielding the 10-year Treasury.2 History shows that when equity yields are higher than bond yields, it’s usually a buying opportunity for stocks.

▪ The sharp sell-off has done some technical damage to the markets, which could take some time to repair.

▪ Equities may be currently oversold, but we may not yet have seen the lows of this cycle.

▪ The most important signs to mark a turnaround are likely to be clarity on better corporate earnings results and stabilizing commodity prices.

What Happened? Why?

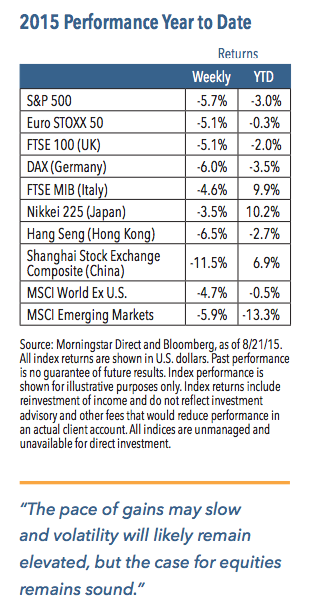

The S&P 500 Index fell 5.7% last week, its biggest weekly pullback since September 2011.1 Equities have been under pressure for some time, and it appears that investors finally gave in. Several factors drove the sharp sell-off: 1) A months-long decline in earnings expectations 2) Widening credit spreads 3) Further evidence of economic weakness in China and the devaluation of the yuan 4) Generally slowing global growth, along with commodity price weakness and deflationary concerns 5) Uncertainty over Federal Reserve policy 6) Technical deterioration over the last few months 7) Investor nervousness and typically thin summer trading volume.

Has the Economic and Market Backdrop Deteriorated?

In our view, sentiment may have taken a hit and will take some time to recover. That may have some near-term negative implications, but we continue to believe that the global economy (and the U.S. in particular) remains sound. Investors have become increasingly concerned about growth prospects, deflation and liquidity trends, with the sharp downturn in oil and commodities being at the epicenter of these worries. The abnormally slow and choppy recovery has also acted as a drag on sentiment over the past few years. Moreover, many are worried that the Fed will make a mistake by raising rates.

We have seen multiple periods of intense but short-lived “risk-off ” phases since the end of the Great Recession, and we believe we are in the midst of another one. We remain relatively upbeat about the global economic growth outlook. Many regions continue to struggle, but we believe forward indicators point to an acceleration in U.S. growth, driven by higher levels of consumer spending. Furthermore, we firmly believe that lower energy prices are a net positive for the U.S. economy and should act as a tailwind for corporate earnings in the coming quarters. Increasing anxiety and the current downturn may delay Fed rate increases. But when the Fed does act, we think a modest rate increase should prove to be a near non-event since policy will remain relatively accommodative. Pessimism remains high, which will likely keep markets unsettled. However, we believe investors will look back on the present time as being little more than a bump in the road during a period of slow and uneven growth.

What Should We Expect from Here?

Market pullbacks of 5% or more are not uncommon during bull markets. We think volatility will remain high, and we may not yet have seen the bottom of this selloff. We expect markets will recover and do not think we are nearing the end of the current bull market.

What will it take for equities to resume their uptrend? For one, we need more consistent and clearer signs that economic growth is on track and that corporate earnings have recovered. We expect the global economy to regain momentum, led by the United States and Europe. We also forecast better earnings growth in the coming quarters. Additionally, we think equities will remain under pressure as long as credit spreads are widening. Many of the same factors that caused the equity market downturn have put pressure on fixed income credit sectors. If oil prices were to stabilize and liquidity concerns to fade, this would go a long way toward helping to ease pressure on both asset classes. Finally, we think investors will require signs that the Chinese economy is not entering a free fall. China’s economy is clearly in trouble, but we think policymakers will engage in additional easing measures to promote growth. This should assuage fears that the country is facing a hard economic landing. None of these factors is likely to emerge quickly or easily, but we do think they should eventually come to pass.

How Should Investors Position Themselves?

Pessimism is on the upswing and equity sentiment has soured in favor of cash and Treasuries. That may not change quickly, but we are leaning against the tide and believe the case to overweight equities remains sound.

So what should investors do? This may present an opportunity for investors sitting on cash waiting for a market pullback. In contrast, locking in profits may benefit those who have enjoyed the tripling of stock prices since the 2009 low. And for all investors, although we do not believe this bull market is over, we think the pace of gains is likely to slow and volatility should pick up.

1 Source: Morningstar Direct, Bloomberg and Standard & Poor’s as of 8/21/15. The S&P 500 Index dropped to 666 in March 2009 and peaked at 2,131 in May 2015.

2 Source: Bloomberg as of 8/21/15. The 10-year Treasury yielded 2.04%.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

©2015 Nuveen Investments, Inc. All rights reserved.