Weighing the Week Ahead: What Are the Lessons from the Market Turmoil?

Dramatic events reset agendas. People re-evaluate probabilities about what is possible as well as the personal implications. Because the recent market story is so big and so fresh the week will start with the punditry asking:

What are the lessons from the market turmoil?

Prior Theme Recap

In my last WTWA I predicted that everyone would be asking whether the recent market decline was the start of something big. Monday’s 1000 point opening decline in the Dow underscored the theme. The next day the story continued with a failed rally. At that point, few would have guessed that the market would finish in the plus column for the week.

As he does each week, Doug Short’s recap explains this dramatic story and his great weekly snapshot lets you see it at a glance. With the ever-increasing effects from foreign markets, you should also add Doug’s World Markets Weekend Update to your reading list.

As Doug notes, the rebound stalled at the end of the week. CNBC quit running the “Markets in Turmoil” special report and went back to reruns of American Greed. Attention then turned to my secondary theme – the early reports from the Fed conclave at Jackson Hole.

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead. You can try it at home.

Last week some advance planning was especially important. There was little time to react intelligently.

This Week’s Theme

Big events refocus attention and redefine the public agenda. They change our minds about what is possible, what is likely, and what to worry about. This week will start with more discussion about the meaning of the market turmoil and what, if anything, individual investors should do about it. The question for each producer or editor in financial media will be:

What are the lessons from the market turmoil?

It is a fertile topic and worth exploring. It should keep interest piqued until late in the week when the jobs report and Fed implications regain center stage.

So what were the lessons?

The Viewpoints

What you “learned” from the market turmoil seems to vary based upon your starting viewpoint. See Josh Brown’s recap of editorial cartoonist’s take on the market.

The conclusions once again cover a wide spectrum, with authorities lining up on all sides. Here are contrasting takes on several different topics.

On the Overall Economic and Market Health

- Steep declines revealed the inherent weakness in the economy, stock valuations, and Fed policy. Worldwide weakness will drag developed countries into a global recession. Central banks will have no bullets left. The selloff and rebound provided a big warning to the wise.

- The “correction” was over. That is what we have all been waiting for. Economic growth and the stock market rally can resume.

On China

- We can now see how important the weakness in the Chinese economy really is. (Typical piece on this theme from Bloomberg, also running a bearish cover this week).

- The Chinese threat has been examined and the effects analyzed. The impact is limited.

On the Fed

- The Fed can finally see the error of its ways, but really has nowhere to turn.

- The Fed is ready to move, but acknowledging some concern about worldwide markets.

On Personal Finance

- It is time to sell. Major investors who had hedges in place last week showed significant profits while everyone else was crushed.

- The volatility did not matter if you held firm. Hedges were difficult to cash in.

As always, I have my own ideas in today’s conclusion. But first, let us do our regular update of the last week’s news and data. Readers, especially those new to this series, will benefit from reading the background information.

Last Week’s Data

Each week I break down events into good and bad. Often there is “ugly” and on rare occasion something really good. My working definition of “good” has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially – no politics.

- It is better than expectations.

The Good

There was some good economic news, especially GDP revisions.

- GDP revisions were strong, raising the bar for expectations. The change was so great that the “old news” had a market effect. Scott Grannis notes that recent growth of 2.7% is significantly better than the former trend of 2.2%. Despite this, it is still $2.8 trillion per year below trend. Few are thinking about the effects of a return to trend, not to mention an overshoot.

- Consumer confidence is very strong according to the Conference Board survey. The Michigan survey was a slight miss, but see below.

- New home sales show a solid y-o-y gain of more than 21%, despite showing a slight miss for the month. Calculated Risk has the full story, including this chart:

-

Sentiment on many fronts

- Negative among short-term market timers (Mark Hulbert highlights this contrarian indicator)

- The best market timers, by contrast, are bullish. (Also from Mark Hulbert). They have an equity exposure 84% higher than the worst performers in Hulbert’s database.

- Insider buying was at the highest level since 2011 (Bloomberg)

The Bad

There was also some negative data last week.

- Personal income and spending. Income was OK, but spending slightly missed the seasonally-adjusted expectations. Steven Hansen at GEI provides the complete picture, with a slightly more optimistic take on year-over-year data.

- Pending home sales showed a slight miss, while still gaining 5% on a year-over-year basis. (Calculated Risk).

- Michigan sentiment disappointed slightly and declined. Given the stock market decline, those in charge of the survey thought the results held up pretty well. This one was especially interesting because the data represent later polling than the Conference Board report. NY Fed President Bill Dudley noted this in answers to questions following a speech. Fed observers seem to be watching this closely. As always, Doug Short (and Jill Mislinski) have the full story including both analysis and plenty of charts. It is useful to look at both the Conference Board and Michigan surveys, which usually show a high correlation.

The Ugly

The ugly award this week goes to the performance of many financial markets. Many reasons are being offered, making this a subject for a full post someday. For now, let us note the following:

- The “rule 48” process of opening stocks did not generate valid prices. Customers doing market sell orders lost 20% or more on major stocks.

- ETF pricing was unfair, according to fair value based on underlying holdings. (ETF.com)

- Options markets were extremely wide, including prices that were “below parity” and therefore impossibly unfair.

- Popular hedging products like the VIX did not even have quotes until the market had regained more than 50% of the early losses. (Options expert Adam Warner)

- Some online trading sites were not responding.

- Systems overheated, creating a “glitch.” (Reuters)

The products and rules have become more complicated. This has permitted more products and increased revenue for the exchanges. It may not have improved opportunities or fairness for individual investors.

Quite frankly, the best thing that the individual investor could do during the turmoil was beware, and maybe stand back. Buy orders were OK, but that was not the mission of most traders on Monday morning.

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. Think of The Lone Ranger.

This week’s award goes, for separate articles on a theme, to Michael Batnick and Todd Sullivan (citing “Davidson). Both illustrate the danger in the way the Shiller CAPE ratio is presented to investors. Batnick notes:

When Shiller says 15-16 is where CAPE has typically been, what he really means is this is what the average has been. However, what he fails to mention is that over the past 25 years, the CAPE ratio has been above its historical average 95% of the time. Stocks have been below their historical average just 16 out of the last 309 months. Since that time, the total return on the S&P 500 is over 925%.

Sullivan shows that the profit estimates in the data are flawed because of accounting changes. He shows that large and completely implausible changes in “earnings” were actually the result of the FAS 157 rules.

Noteworthy

As a professor I made it a point to review and update illustrations and references in pop culture, but it was a swiftly-moving target. Beloit College provides a “mindset” list highlighting the experience of incoming freshmen. If you are forty or older, I guarantee that this will make you feel even older. The list has 50 entries. A few of my favorites?

-

Incoming students have always had Google.

-

They have never licked a postage stamp.

-

They have grown up treating Wi-Fi as an entitlement.

-

The announcement of someone being the “first woman” to hold a position has only impressed their parents.

Quant Corner

Whether a trader or an investor, you need to understand risk. I monitor many quantitative reports and highlight the best methods in this weekly update. For more information on each source, check here.

Recent Expert Commentary on Recession Odds and Market Trends

Bob Dieli does a monthly update (subscription required) after the employment report and also a monthly overview analysis. He follows many concurrent indicators to supplement our featured “C Score.”

Georg Vrba: An array of interesting systems. Check out his site for the full story. We especially like his unemployment rate recession indicator, confirming that there is no recession signal. He gets a similar result from the Business Cycle Indicator. Georg continues to develop new tools for market analysis and timing, including a combination of models to do gradual shifting to and from the S&P 500.

Doug Short: Provides an array of important economic updates including the best charts around. One of these is monitoring the ECRI’s business cycle analysis. Jill Mislinski has joined Doug’s team and provides this week’s update.

RecessionAlert: A variety of strong quantitative indicators for both economic and market analysis. While we feature the recession analysis, Dwaine also has a number of interesting systems. These include approaches helpful in both economic and market timing. He has been very accurate in helping people to stay on the right side of the market.

Dwaine has a new signal from his Stock Market Health Diffusion Index, something he calls a high alert. At the moment, it is just an alert, but it bears watching. (We note the similarity to Felix’s conclusion this week).

The Week Ahead

It is very big week for economic data.

The “A List” includes the following:

- Employment report (F). Most important remaining data before the September FOMC decision.

- ISM index (T). Private data with both concurrent and leading qualities.

- ADP employment (W). A good independent read on the changes in private sector jobs.

- Auto sales (T). Surge is a sign of consumer strength. Pickup trucks indicate construction strength.

- Construction spending (T). July data, but an important sector.

- ISM services (Th). Gets less attention than the manufacturing survey, but actually covers more of the economy.

- Initial jobless claims (Th). The best concurrent news on employment trends, with emphasis on job losses.

The “B List” includes the following:

- Beige book (W). Anecdotal data used in the Fed decision process. This sometimes gets a lot of attention.

- Chicago PMI (M). Most important of the regional surveys.

- Trade balance (Th). July data of special relevance for Q3 GDP and evaluating effects of dollar strength.

- Factory orders (W). July data and a volatile series.

- Crude oil inventories (W). Current interest in energy keeps this on the list of items to watch.

While the Jackson Hole conference is over, there is plenty of FedSpeak on tap. Expect wide-ranging opinions.

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a “one size fits all” approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

Insight for Traders

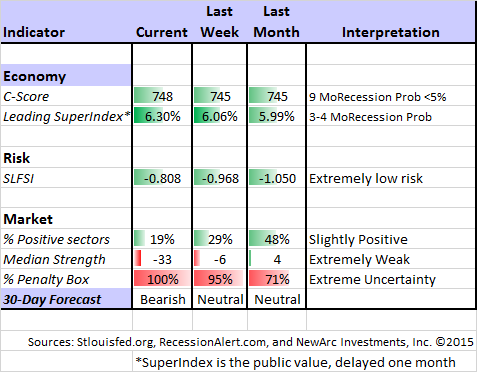

Felix has switched to “neutral,” but is almost completely out of the market. The confidence in this three-week forecast remains extremely low with nearly all sectors in the penalty box. Felix withdraws from the market when volatility gets very high. It is simply not a good environment for the model. I noted reports that many system-oriented trading firms have temporarily suspended trading. There is nothing wrong with waiting for better conditions. The inverse funds, bonds, and gold recently moved up the rankings, but are mostly in the penalty box.

See this week’s “Ugly” section for more on trading challenges.

Insight for Investors

I review the themes here each week and refresh when needed. For investors, as we would expect, the key ideas may stay on the list longer than the updates for traders. Major market declines occur after business cycle peaks, sparked by severely declining earnings. Our methods are focused on limiting this risk. Start with our Tips for Individual Investors and follow the links.

We also have a page summarizing many of the current investor fears. If you read something scary, this is a good place to do some fact checking.

Other Advice

Here is our collection of great investor advice for this week.

If I had to pick a single most important article, it would be this article from Morgan Housel, explaining the results and challenges for individual investors. First, the results.

Please read the entire post. A key theme is that investors blame performance on the wrong things – the market cheated them, etc., when it is mostly their own poor market timing.

Stock Ideas

Energy –Back in Focus On several occasions I have explained why “energy” should not all be traded like an oil futures contract. Joshua Kennon does a very good job on this topic, backed up with data and charts. A key point is that the oil majors must operate on a longer time frame than the quarterly report. You acquire reserves when it is possible to do so, not when compelled, for example. It is a long post, but well worth reading. Here is a key point, familiar to regular WTWA readers:

For the oil majors (as opposed to the pure plays, which are a different story), that’s not the whole picture. It is entirely possible for a trader or hedge fund manager to say oil stocks are overpriced at the moment, calling for them to decline and a long-term investor to say that oil stocks are undervalued at the moment, preaching you should use your funds to load up on them. That seems almost nonsensical; a paradox. Nevertheless, it’s true when you understand one fundamental fact: When you buy a share of the oil majors outright, paying for it in cash and locking it away, you are being paid to absorb volatility over multi-year periods.

For this reason we frequently have one of the big integrated oil companies as part of our Enhanced Yield portfolio, capturing both dividends and income from selling calls, with the expectance of gradual long-term growth.

Commodity guru Jim Rogers sees a potential rebound.

Dividend strategies. Please read this excellent comprehensive guide. Is it enough to cash your regular payments, ignoring the stock price? Or should you focus on total return? Rob Martorana’s absolutely first-rate article is written for the community of investment advisors, but it is not a secret. Individual investors will appreciate the advice.

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for over ten years. The average investor should make time (even if not able to read every day as I do) for a weekly trip on Wednesday. Tadas always has first-rate links for investors in this special edition. As always, there are several great links, but I especially liked this article from Monevator on the need for a plan. Does this sound familiar?

When markets fall, some panic and consider selling. That’s natural.

Others act brave, rub their hands, and boast about it being time to buy – to be greedy when others are fearful.

That sentiment is right, and they can sound like bold geniuses.

But how long were they sat in cash, waiting for the moment to get back in?

If you buy equities when they drop 10% but you missed the previous 50% rally, you’re not being greedy when others are fearful.

Not in the bigger picture.

You’re actually being timid when others are stoically betting on the long-term propensity of stock markets to rise over the long-term.

And you’re probably going to be left poorer compared to someone who is less cunning but more pragmatic.

The price they pay for their long-term gains is not feeling as smug as you when the market does swoon. They have to take their lumps.

Fed Outlook

As I suggested last week, we have the key news from Jackson Hole in time for WTWA, but not in time for Friday’s trading. Fed Vice-Chair Stanley Fischer granted a CNBC interview on Friday which seemed to cover many of the key points from his Saturday keynote speech. The speech was a little hawkish, but I do not expect a major market reaction to this on Monday. Sam Ro at Business Insider has good coverage along with key charts from the speech.

Here are some key takeaways:

- As of a few weeks ago, the Fed was probably ready to act in September;

- The Fed rates economic strength significantly higher than do the various financial markets;

- Market volatility is not the determining factor in a delay, but it is a consideration;

- The Fed sees the current low levels of inflation as a “one off” effect of lower energy prices and dollar strength;

- The Fed will not wait until after there is more inflation before starting the process of withdrawing accommodation; and finally

- The process of normalizing rates will be gradual – perhaps very gradual.

And of course, Fed expert Tim Duy’s take. And finally, a member-by-member scorecard (Steve Goldstein).

China Outlook

With so much attention on China, U.S. investors need to understand the implications for their portfolio. Everyone is trying to figure out which sources are reliable and how serious slowing growth is for the rest of the world. Sound? Or not sound? Dueling professors look at different data. It is all interesting. And keep in mind, from a Nobel Prize Winner, that the Chinese stock market does not give a good read on the economy.

At the peak of concern last week I provided a summary of What Investors Must Know about China. China expert Nicholas Lardy reached similar conclusions in a NYT op-ed piece published the same day.

The New York Times is highlighting “zombie factories” with a dramatic slide show. In sharp contrast, Templeton’s Mark Mobius, perhaps the most respected source on international investing sees jammed malls and expensive purchases. (Mobius’s frequent flyer miles make the George Clooney character seem like a piker!) Mobius provides some investing ideas along with this interesting thought:

A lot of attention has been given to slowing gross domestic product (GDP) growth in China. It bears repeating—China’s growth rate may be slowing, but one of the things that gets lost in translation is that while the percentage increases in the economy are indeed slowing down, but the actual dollar amounts are going up. When China’s economy was growing at 10% in 2010, about US$844 billion was added to the economy, but with growth at 7.7% in 2013, US$986 billion was added.2 I would also emphasize that 7% growth is nothing to sneeze at, either, given the size of China’s economy. It should not be a shock to see growth slow.

Watch out for…

Long-short equity funds, which have now lagged for more than a decade. (Eqira).

Final Thought

The past week was a great test for many investors. If you were prepared and had confidence in your plan, all was well. If you were calling audibles, you were likely to go wrong.

My own take on the lessons?

The China concern is over-rated, both because the economy is not as bad as advertised and because the US does not compete so much on exports. I expect companies that benefit from cheaper Chinese goods to show better profits.

The energy market is showing a little strength. The benefits of lower prices will start to show up for some companies, and the eventual market price will be OK for suppliers. There are opportunities here.

The Fed is more accurate on the economic prospects than the financial punditry. It is much better than the commodities market, which has (once again) dramatically over-estimated the probability of a recession. Falling oil prices have never predicted an economic downturn. (GaveKal).

The market timers who “predicted” the selling may not have done as well as advertised. Think about the following (all examples I read in major media):

- Some of them have been waiting for this for many months, paying put premiums throughout

- Claims of profits on Monday were not “locked in” gains, but on paper. Much of this was gone by Friday. (Example).

- Many of the big bears saw Monday and Tuesday as verification of their theories about the market being 50% over-valued. They were not selling their puts. They were waiting for more or rolling positions.

- Those who tried to cash in struggled because of illiquidity or unfair pricing in markets.

If you think it is wise to have protection in place, this week’s experience helps to see how difficult it can be to manage your hedges.

Those who read and considered this section last week may have escaped without major losses, and maybe with some gains in the market turmoil. I hope so.

Let me turn to this week’s investment thought.

Investment Conclusion

I still do not know whether we have a real near-term market bottom in place. (Neither does anyone else). I was right about retail panic last week.

I continue to see the trader/investor difference as crucial. I expect continued economic strength in the U.S. and improvement in Europe. While watching China and energy closely, the focus on commodity prices as an economic indicator is mistaken. I expect the Fed to start raising rates. It will have little impact on most sectors, but will help financials.

As a result, I find good opportunities, as follows:

- Financials, especially regional banks, from rising rates

- Technology, since skepticism about the dollar is overdone

- Energy, since the dollar will not grow at the same pace, the economy is better than expected, and geopolitical risks are showing up

- Health care – especially stocks with little or no China exposure