China May Surprise You

The current global market volatility has made some investors skittish and, presumably, many are contemplating curtailing the equity exposure in their portfolios. But before throwing in the towel, they will do well to ask themselves: Who is buying all the stocks amid this selloff?

The most likely answer is experienced investors who can look beyond the media noise and stay focused on the long term. We at Thomas White believe there are several reasons why the current market environment presents an opportunity for investors that are patient and resolute.

To put our reasoning in perspective, first let us explain the events of recent weeks and why we think many of the concerns now, in particular those related to China, appear to be misguided.

WHY GLOBAL MARKETS, ESPECIALLY THE U.S. AND CHINA, HAVE BEEN IN TURMOIL RECENTLY

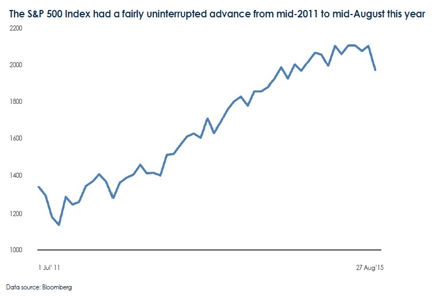

The popular view is that the developed equity markets started falling because China devalued its currency abruptly, adding to concerns that the Asian economy’s problems were bigger than they appeared to be. In reality, developed markets, particularly the U.S., were primed for a decline, not having experienced any significant correction for an unusually long time. For instance, the S&P 500 had been setting records for its uninterrupted advance and had not had a 10 percent plus correction since mid- 2011. So, China’s currency devaluation on the 11th of August, typically a month when markets decline due to low investor trading activity, likely acted as a spark for the downside.

It is also possible that with the recent round of positive economic news in the U.S., market participants were convinced the Federal Reserve would increase interest rates for the first time in September. Investors have long been apprehensive about this first hike, given the over-reaction and contagion former Federal Reserve Chairman Ben Bernanke’s “taper” announcement caused in May 2013. Notably, even before China’s currency devaluation, junk bonds appeared to have entered a bear market and the prices of smaller cap stocks had started experiencing downward pressure in anticipation of a rate hike.

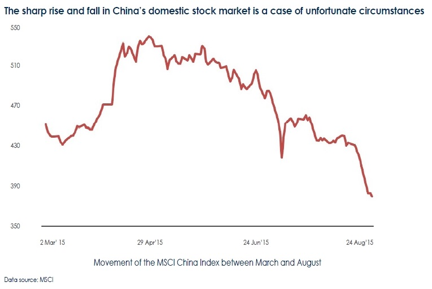

Seen in the proper context, even the sharp rise and fall in China’s domestic stock market since March this year is likely a case of unfortunate circumstances. All through late last year and early this year, speculators significantly pushed up the prices of Chinese stocks trading on the mainland (the so-called “A” shares), expecting more foreigners to buy these shares through the Hong Kong Shanghai Connect program, a new trading link Beijing launched in 2014 to open up the Shanghai stock market to overseas investors as a part of its ongoing effort to improve China’s capital market institutions. But by the time final permission was given to make the program operational, mainland stock prices had climbed to such levels that many foreign institutions chose not to participate. Since the majority of speculators had borrowed money at high interest rates to buy the shares, they were forced to sell their stocks in a hurry when they did not see the expected rise in demand from foreign buyers.

Speculators’ demand for “A” shares had also been driven by the fact that MSCI was expected to include the “A” shares in its Emerging Markets Index, a move that would have drawn an estimated $400 billion from foreign asset managers and other institutional investors into mainland China’s equity markets. Unfortunately, MSCI put on hold this planned inclusion due to technical and other reasons, which disappointed speculators and fueled the stock market decline.

WHY SOME OF THE CONCERNS RELATED TO CHINA, ESPECIALLY ITS RECENT CURRENCY DEVALUATION, ARE LIKELY EXAGGERATED

Close on the heels of the June and July selloff in Chinese equities came the devaluation of the yuan, which exacerbated the slide since it created the perception that China’s planned move from an investment and export-driven growth model to one that relies on domestic consumption was faltering and so, policy makers in the country were focused again on boosting exports through a yuan devaluation. We feel this perception is likely incorrect due to one or more of these reasons.

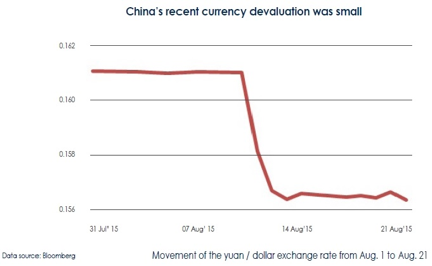

For one, the devaluation was so small (about 2 percent) that perhaps its primary purpose was to warn Europe and Japan to stop devaluing their currencies. Through the devaluation, Beijing might also have been signaling to the Federal Reserve that raising interest rates in September could damage the global recovery. What is most plausible though is that Beijing was trying to move China toward a more flexible exchange rate to increase the yuan’s chances of being included as a component in the International Monetary Fund’s (IMF) Special Drawing Rights, which is an international reserve asset.

The IMF is now conducting a review of the basket of currencies that form the SDRs and the inclusion of the yuan in this basket will not only enhance the yuan’s standing globally but should also encourage other nations to include the yuan in their currency reserves.

The yuan devaluation has triggered another concern – that if other Asian economies also start devaluing their currencies to protect their exporters, the region may see a round of competitive currency devaluations, the sort of event that triggered the Asian Financial Crisis in 1997. We feel such a scenario is unlikely because the conditions now are very different from what they were 18 years ago. Back then, many weak Asian economies with inadequate foreign exchange reserves had their currencies rigidly pegged to the U.S. Dollar. Today, financial systems in the region are relatively robust, with limits on capital flows, more flexible exchange rates, and bigger than before foreign exchange reserves. Further, short term foreign borrowings of these countries are much lower when compared to 1997. In short, Asian economies these days have more effective control over their liquidity conditions.

Many investors believe the devaluation can hurt China in two other ways – the country’s import costs may go up, denting the economy, and a weaker local currency may add to the debt burdens of Chinese companies that have all or a portion of their borrowings denominated in a foreign currency, such as the U.S. Dollar or the Hong Kong Dollar. In our opinion, Chinese companies in the manufacturing, energy, chemicals and electrical generation sectors may be slightly hurt due to a rise in import costs, but a major part of China’s imports are commodities and the demand for natural resources in the country is so weak now that the cost of these imports may not rise meaningfully.

As far as the external borrowings of Chinese companies are concerned, most firms have a relatively small portion of their debts denominated in U.S. or Hong Kong dollars. Real estate developers, at an average of 35 percent, have the most.

WHY CHINA IS AN OPPORTUNITY FOR INVESTORS NOW

In our opinion, the events of the last few months have presented investors an opportunity to enter or increase their exposure to the China equity markets. Having interpreted the Chinese government’s recent direct purchase of stocks as a big negative, most institutional investors have forced down the prices of the major Chinese blue chips that trade in Hong Kong and the U.S. In fact, since only a small number of mainland investors can purchase Chinese companies traded in Hong Kong, most of the Hong Kong shares currently trade at prices 30 percent lower than the same company shares on the mainland.

What’s more, valuation levels of the MSCI China Index, which represents 26 percent of the MSCI Emerging Markets Index, are near their decade lows. We believe that the distinct undervaluation of the MSCI China Index relative to other world equities has increased the likelihood of the emerging markets asset class beginning an extended period of relative outperformance. If so, this represents an opportunity for investors to consider realigning their asset allocation.

Besides benefiting from low valuations of the broader China markets, investors may also add value to their portfolios in the long term by focusing on specific categories of stocks. For instance, the recent devaluation should help Chinese exporters, effectively allowing them to gain business by offering lower prices versus their competition. This is especially true of companies that primarily export to the U.S. These companies have seen robust growth in their U.S. revenues lately as the relative strength of the American economy has boosted their sales volumes while the dollars they have received as revenues have expanded in value relative to the yuan. In short, their profit margins have grown wider as the yuan remains weak versus the dollar.

As China embraces a consumption-driven growth model, many American consumer goods companies that have significant operations in China could see expanding sales in the future. Although anecdotal evidence suggests that the Chinese consumer is becoming more discerning and price-conscious, retail spending does not appear to have been affected significantly by the stock market turbulence as only 6 percent of Chinese households own stocks. In fact, China’s retail sales have been expanding at an annualized rate of 10 percent in recent months.

On the whole, China’s current policies appear to have been designed to soften a mild growth recession, something the country’s policy makers have handled successfully every 5-6 years. Way back in 2008, at the peak of the global financial crisis, it was the Chinese government that kept things going for the global economy through an enormous stimulus. China’s voracious appetite for resources lifted commodity-producing economies from Brazil to South Africa and it was Chinese demand that saved the day for American auto companies.

We believe that this time too Beijing’s proven capacity for a turnaround, along with the attractive valuations of Chinese stocks, stands long-term investors in good stead.

This article is for informational purposes only. This article is not intended to provide tax, legal, insurance or other investment advice. Unless otherwise specified, you are solely responsible for determining whether any investment, security or other product or service is appropriate for you based on your personal investment objectives and financial situation. You should consult an attorney or tax professional regarding your specific legal or tax situation. The information contained in this article does not, in any way, constitute investment advice and should not be considered a recommendation to buy or sell any security discussed herein. It should not be assumed that any investment will be profitable or will equal the performance of any security mentioned herein. Thomas White International, Ltd, may, from time to time, have a position or interest in, or may buy, sell or otherwise transact in, or with respect to, a particular security, issuer or market on our own behalf or on behalf of a client account.

FORWARD LOOKING STATEMENTS

Certain statements made in this article may be forward looking. Actual future results or occurrences may differ significantly from those anticipated in any forward looking statements due to numerous factors. Thomas White International, Ltd. undertakes no responsibility to update publicly or revise any forward looking statements.