New bond issuance in the US investment grade (IG) market has exploded in 2015 as companies look to finance mergers and acquisitions (M&A), and Invesco Fixed Income sees no signs of this trend slowing down through the end of the year.

This has consistently weighed on US IG credit spreads this year, as investors sell their current holdings to make room for new bond issues. However, the US IG market is enforcing some discipline on issuers by demanding higher yields and wider spreads in order to get new bond deals done, which means valuations in the US IG market are becoming quite attractive relative to other fixed income asset classes, in our view. This may garner a pickup in demand for the asset class over the medium term.

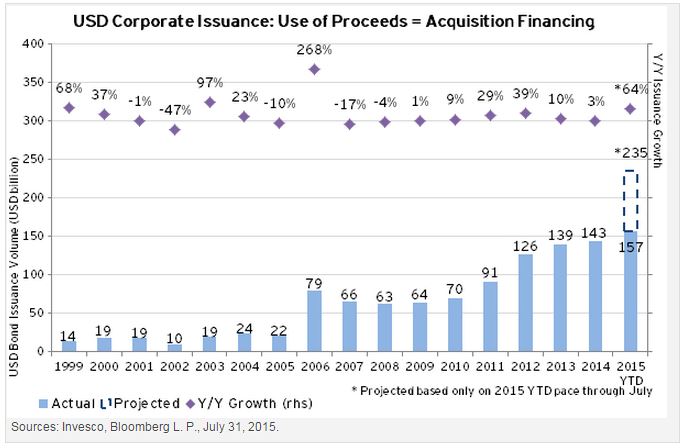

2015 looks to be a big year for M&A

As the chart below shows, we have already exceeded 2014’s acquisition-related issuance volumes through July 2015, and, at this pace, we are on track for 64% year-over-year growth.1 While the bulk of activity continues to originate from the health care sector, M&A related supply growth has been widespread across industries in 2015. Even in the banking sector, where M&A activity has been very subdued, we are seeing new bond issues due to new regulations aimed at raising more capital.

Why are companies issuing IG bonds to finance M&A?

Much of the impetus behind M&A transactions has been strategic rather than financial. Organic revenue growth has been difficult to achieve in the current environment, and many companies have already squeezed as much efficiency out of their own expense bases as possible. Given the low interest rate environment, it makes a lot of sense for companies to seek acquisitions with attractive synergy opportunities to drive future earnings growth.

While a pickup in M&A is a common phenomenon as the economy enters the later phases of the corporate credit cycle, we’ve never seen the US investment grade bond market serve as the most favored source of M&A financing. So why the popularity today?

- Increased regulatory scrutiny has severely restricted banks’ ability to provide financing for highly-levered deals (i.e., leveraged buy-outs or LBOs).

- In addition, the high yield corporate bond market has been less receptive to a pickup in new bond supply in 2015, due to pressure from the severe decline in oil and commodity prices.

- On the other hand, extremely accommodative monetary policy by the Fed has helped to stimulate extraordinary demand for US IG bonds in recent years.

Unfortunately, monetary policy is contracting just as new bond supply has shifted into high gear.

All eyes on the Fed

Regarding monetary policy, the anticipation of an increase in the fed funds rate by the Federal Open Market Committee (FOMC) later this year has likely exacerbated the drive for companies to complete deals and obtain financing at low interest rates before rates start to rise again. We are expecting a potentially record-breaking amount of new bond supply between Labor Day and the FOMC meeting on Sept. 17, with the possibility of multiple $10 billion-plus issuance days. Our estimate is based on the pending M&A calendar over the next 12 months (which includes around $190 billion of US dollar IG supply in the pipeline) and feedback from bond dealers.2

Invesco Fixed Income plans on taking a very discriminating approach toward these new issues, avoiding deals where we see credit challenges or significant new issue supply through the end of the year. If the Fed keeps rates unchanged, we would expect the heavy supply to continue at its recent pace through the end of the year. If the Fed raises interest rates in September, much will depend on the market’s interpretation of Fed forward guidance and pace of future interest rate increases.

- If the Fed vows to proceed at a very slow pace (i.e., no more hikes for six months and no more than two 25 basis point hikes in 2016), we would expect the markets to receive this positively and the new issue calendar to experience only a brief pause before resuming at a pace somewhat slower than we’ve seen so far year to date. This is likely the best case scenario for US IG credit spreads, in our view.

- However, if the Fed is hawkish and seems committed to hiking rates at a faster pace, the market is likely to react negatively and begin pricing in a recession in the US, and new issue supply could slow considerably. Unfortunately, this is not the type of outcome that would be positive for US IG spreads, despite the slowdown in supply, but we view this type of hawkish guidance from the Fed as unlikely.

Invesco Fixed Income’s view

The silver lining in all of this is that the US IG market is enforcing some discipline on issuers by demanding higher yields and wider spreads in order to get new bond deals done. Valuations in the US IG market are becoming quite attractive relative to other fixed income asset classes, and we suspect an opportunity will likely present itself in the medium term to take a more positive view on IG credit spreads and increase our allocations accordingly.

As long as the majority of M&A deals remain strategic in nature and companies follow through on commitments to de-leverage after the deals close and maintain investment grade ratings, we are likely to be in store for a longer-than-average credit cycle. We are watching for a normalization in the supply/demand imbalance that has persisted so far in 2015 through some combination of a slowdown in supply and/or an increase in demand for US IG.

1 Sources: Invesco, Bloomberg L.P., July 31, 2015.

2 Sources: Bloomberg L. P., Invesco, Aug. 17, 2015.

Read more fixed income investment views.

Important information

A basis point is one hundredth of a percentage point.

Fixed-income investments are subject to credit risk of the issuer and the effects of changing interest rates. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa. An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2015 Invesco Ltd. All rights reserved.

Investment grade bonds power explosion in M&A by Invesco Blog