Let’s face it – nobody really likes paying taxes, especially investors. We all know investment returns can be taxable, but most investors generally hope to minimize taxes so they can try to maximize net returns. And why not? Reducing taxes on an investment portfolio can help to increase an investor’s after-tax wealth. But the overarching goal should be about maximizing after-tax wealth — not tax avoidance. Avoiding a tax is not a financial plan.

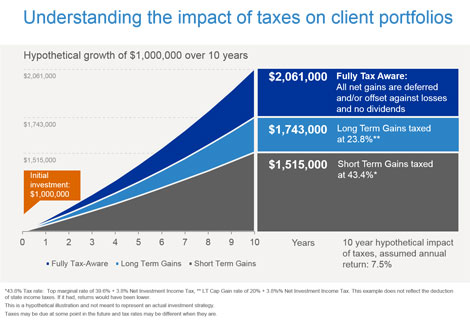

Here’s a hypothetical example that shows the potential impact of taxes on an investment portfolio. Our prudent investor, we’ll call him James, has a $1 million nest egg. Over the next 10 years he has three options for investing that money. One strategy is fully tax-managedand successfully defers all gain recognition to a later date. Thesecond treats all gains as long-term capital gains for the funds, but in doing so incurs taxes of 23.8% (rate for those in top tax bracket) each year. The third approach chases short-term gains, whichresults in the annual gain being taxed as short term and treated as ordinary income at 43.4%.

As you can see in the chart, the fully tax-managed strategy could potentially help to net big, albeit hypothetical, gains, more than doubling the initial fund. Going after only long-term gains in this hypothetical situation looks good if taken by itself, but less appealing when matched against the fully tax-managed strategy. And if James chooses to chase short-term gains — ouch! That approach could potentially yield only half the gains of a tax-managed strategy.

Yet, it’s understandable that people might choose the initial potential returns of short-term gains because the high activity of buying and selling can seem appealing. But that is only part of the story, especially when the potential tax consequences are not taken into account. So what could investors do when their goal is not to avoid paying tax, but to help gain higher after-tax wealth? The key may be to locate investments in a manner that’s right for their tax status.

For instance, an investor might have a stock portfolio that turns over rapidly, maybe 100% or more within a year. Such turnover can create a lot of short-term capital gains, which, as we’ve seen in the above example, also incurs the highest tax. So any account like that might help to serve an investor’s goals better by being under a more tax-friendly investing umbrella, such as a 401(k).

Commodities can be another tax-unfriendly investment vehicle, so they too may serve an investor’s tax-managed investing strategies best by being held in accounts that have a tax- deferred or tax-exempt status. I’ll write later about portfolio turnover that can be good for reducing taxes through a process called loss harvesting. Just know that there is “good” turnover and “bad” turnover in regards to taxes.

Other investments that can be tax-friendly, such as municipal bonds, may be beneficial for accounts that have a higher tax load. We’ll be talking more about municipal bonds in a future post. Tax-managed mutual funds are another way that may help to lower the tax burden on investments.

The main point of understanding tax liability is to simply be aware of the impact of taxes on a portfolio, and start asking questions about how to lower tax burdens. Too many investors — and their advisors — take a “set-it-and-forget-it” approach to investment portfolios. But the consequences of such an approach can also mean unintentionally “setting it and forgetting it” when it comes to taxes.

So be tax-smart: Seek investment strategies that are designed to help you see good returns while helping to reduce your investments’ tax burden. Until our next tax-aware post, you can see more on my advice to financial advisors and other investors on taxes in this video here.

Disclosures

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

Stock/Equity investors should carefully consider risks such as market risk when investing. There are no guarantees when it comes to individual stocks. Any stock may go bankrupt, in which case your investment may be worth nothing.

Bonds involve risks such as interest rate, credit, default and duration risks. Greater risk, such as increased volatility, limited liquidity, prepayment, non-payment and increased default risk, is inherent in portfolios that invest in high yield (“junk”) bonds or mortgage-backed securities. Investments in derivatives may cause the investors losses to be greater than if he/she invests only in conventional securities and can cause the returns to be more volatile.

Exposure to the commodities markets may subject the Fund to greater volatility than investments in traditional securities, particularly if the investments involve leverage. The value of commodity-linked derivative instruments may be affected by changes in overall market movements, commodity index volatility, changes in interest rates or sectors affecting a particular industry or commodity and international economic, political and regulatory developments. The use of leveraged commodity-linked derivatives creates an opportunity for increased return, but also creates the possibility for a greater loss.

The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional. The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

Investing involves risk and principal loss is possible.

Forecasting is inherently uncertain and may be incorrect. It is not representative of a projection of the stock market, or of any specific investment.

Russell Investments is a trade name and registered trademark of Frank Russell Company, a Washington USA corporation, which operates through subsidiaries worldwide and is part of London Stock Exchange Group.

Copyright © Russell Investments 2015. All rights reserved.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

UNI – 10594