KEY TAKEAWAYS

The latest Beige Book suggests that the U.S. economy is still growing at or above its long-term trend, and that emerging upward wage pressures may get the Fed’s attention soon.

Optimism regarding the economic outlook far outweighed pessimism throughout the Beige Book once again.

Concerns over China’s impact on the U.S. economy have increased on Main Street.

BEIGE BOOK SUGGESTS CONTINUED MODEST ECONOMIC GROWTH

The latest Beige Book suggests that the U.S. economy is still growing at or above its long-term trend, indicating that some of the “transitory factors” that held the U.S. economy back in the first quarter of 2015 have faded. Comments also indicate that concern over China’s impact on the U.S. economy has increased and that some upward pressure on wages is beginning to emerge. Overall, the Beige Book described the economy as expanding at a “modest or moderate” pace in most districts. In general, optimism regarding the economic outlook far outweighed pessimism throughout the Beige Book, as it has for the past two years or so.

The Beige Book is a qualitative assessment of the U.S. economy and each of the 12 Federal Reserve (Fed) districts. We believe the Beige Book is best interpreted quantitatively by measuring how the descriptors change over time. The latest edition of the Fed’s Beige Book was released Wednesday, September 2, 2015, ahead of the September 16 – 17 Federal Open Market Committee (FOMC) meeting. The qualitative inputs for the September 2015 Beige Book were collected from mid-July 2015 through August 24, 2015. Thus, they captured the Main Street reaction to:

Generally better than expected U.S. economic data for June, July, and August 2015, as the economy bounced back in the second quarter and third quarters following several first quarter disruptions (port strike, bad weather, strong U.S. dollar)

A 30% drop in oil prices to under $40 per barrel following a period of price stability in May, June, and early July

The devaluation of the Chinese yuan, a 17% decline in Chinese equity prices, and heightened fears of a “hard landing” in the Chinese economy

SENTIMENT SNAPSHOT

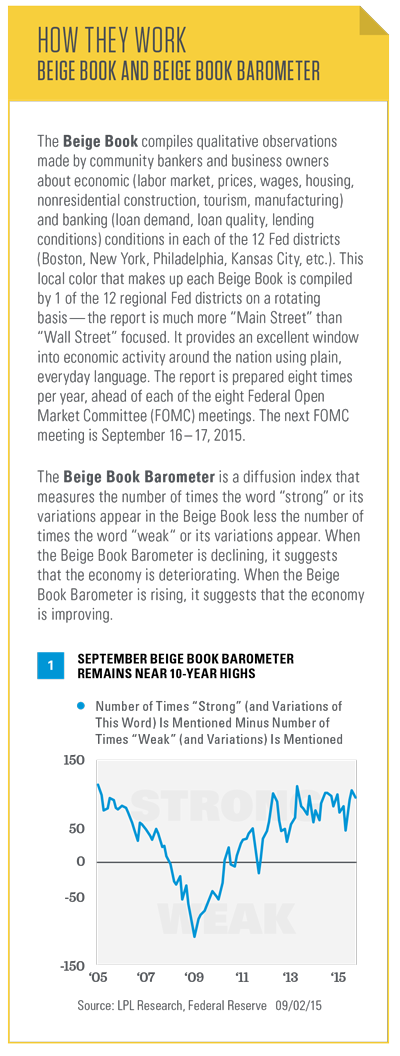

To provide a snapshot of the sentiment behind the entire Beige Book collage of data, we created our proprietary Beige Book Barometer (BBB) [Figure 1]. In September 2015, the barometer ticked down to +95 from +106 in July 2015. Recall that the +106 reading in July 2015 was the highest reading since April 2013, and the second-highest reading in over 10 years. The +95 reading in September 2015 was the ninth-highest reading in more than 10 years.

WATCHING WAGES & INFLATION

As it has over the past year, the September 2015 Beige Book noted that employers were having difficulty finding qualified workers for certain skilled positions and some reported upward wage pressures for particular industries and occupations. In the past, these characterizations of labor markets have been a precursor to more prevalent economy-wide wage increases. Indeed, for the first time in this business cycle, the latest seven Beige Books (going back to December 2014) contained several mentions of employers having difficulty attracting and retaining low-skilled workers, and retaining and compensating key workers.

If this trend persists over the next few Beige Books, history suggests it may not be long until Fed policymakers begin to take note of a faster pace of wage inflation in their monetary policy deliberations. Thus far, most Fed officials have not viewed it to be a pressing concern. In her most recent public appearance, giving testimony to the Financial Services Committee of the U.S. House of Representatives on July 15, 2015, Fed Chair Janet Yellen noted, “Although there are tentative signs that wage growth has picked up, it continues to be relatively subdued, consistent with other indications of slack.”

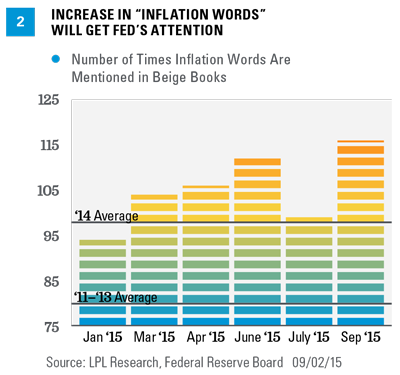

Figure 2 shows the recent trend in the number of “inflation words” in the Beige Book. We counted the number of times the words “wage,” “skilled,” “shortage,” “widespread,” and “rising” appeared in recent editions of the Beige Book. In September 2015, these words appeared 116 times, up from 99 in July 2015. The September reading was the highest count so far this year. This increase in the number of inflation words came despite a 30% drop in oil prices and a smaller decline in broad commodity prices. In all of 2014 — when deflation, not inflation, was a concern — those words appeared, on average, 98 times per Beige Book. During 2011 – 13, also a period when heightened risk of deflation was evident, inflation words appeared, on average, 80 times per Beige Book. We’ll continue to monitor this trend closely, as the FOMC has told markets that it will begin raising rates when it is “reasonably confident” that inflation will move back toward 2.0%.

FEWER COMMENTS ON OIL & ENERGY VS. PAST BEIGE BOOKS

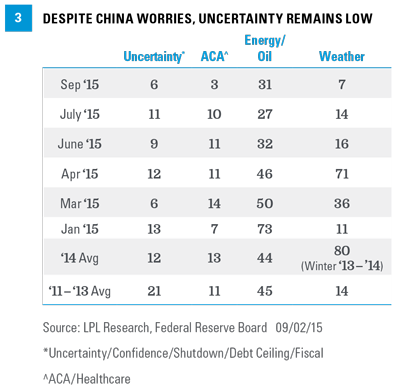

Oil received a total of 31 mentions in the September 2015 Beige Book, below the 46 mentions, on average, in each of the 5 Beige Books released through July of this year, and even below the 44 – 45 mentions per Beige Book in 2011 – 2014 [Figure 3]. This is somewhat surprising given the 30% drop in oil prices during the time the data for this Beige Book were being collected. Although it seems counterintuitive, this may suggest that the capital spending cuts, rig count reductions, and job cuts in the oil and gas sector in late 2014 and in the first few months of 2015 may be fading as drags on economic activity. The summary comment on the energy sector in the September 2015 Beige Book captures the situation in the oil and gas drilling sector well: “Districts reporting on the energy sector indicated that conditions were stable to declining; coal production was down in the Richmond and St. Louis Districts, while oil-related activity declined in the Cleveland, Atlanta, and Dallas Districts.”

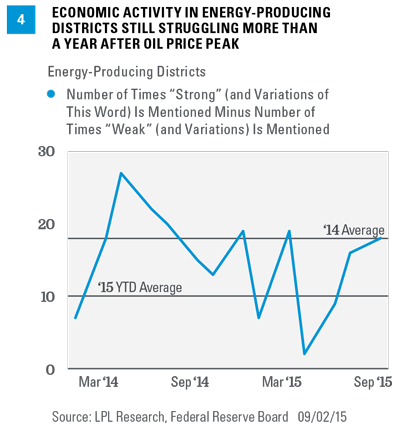

To better gauge the impact of lower oil prices on the economy, we recently constructed a separate Beige Book Barometer [Figure 4] for the three Fed districts that have the most energy-related economic activity (Minneapolis, Kansas City, and Dallas). During 2014, the Beige Book Barometer in the energy-related Fed districts averaged +18. In the first 6 Beige Books of 2015, the barometer in the energy-related districts was just +12, a clear deceleration in activity. However, the energy states’ barometer has been moving higher since hitting +2 in April 2015, and stood at +18 in September 2015, which may indicate that the economy outside of the energy sector in these Fed districts is performing well. Even in places like Texas, Louisiana, and Oklahoma, energy accounts for less 20% of gross domestic product (GDP). However, in the June, July, and September 2015 Beige Books, the number of weak words in the energy-related Fed districts (40) alone accounted for one-third of all weak words (118) in the entire Beige Book, indicating that the economic weakness related to the oil and gas sector is still significant.

As was the case in the Beige Books released thus far in 2015, the September 2015 Beige Book was also full of comments from all 12 Fed districts about how lower fuel and energy prices were benefiting multiple industries. In short, comments on the impact of falling oil prices are consistent with our view that while falling oil prices will be a net plus for the U.S. economy as a whole, economies in certain states could see a significant impact from the slowdown in drilling activity that is likely to occur over the next 6 – 9 months or so. (Please see our Weekly Economic Commentary, “Drilling into the Labor Market,” for more details. In addition, see the Weekly Market Commentary, “Oil’s Long Bottoming Process,” for our latest view on oil prices.)

FADING CONCERNS/RISING CONCERNS

Uncertainty around fiscal policy has continued to fade as a concern; however, in some cases it has been replaced by uncertainty surrounding China, the drop in oil and other commodity prices, and what it might signal for global growth. The Affordable Care Act, and healthcare in general, remained a consistent source of concern among Beige Book respondents; however, the impact has faded a bit recently, with just 3 mentions in the latest Beige Book. Thus far in 2015, this topic has received an average of 9 mentions per Beige Book, below the number of mentions per Beige Book in 2014 [Figure 3].

Weather continues to receive fewer mentions (7 in September 2015, 14 in July, and 16 in June 2015) compared with the 71 mentions in the April Beige Book, indicating the extreme winter weather of early 2015 is also fading as a drag on growth. Despite the effects of this year’s harsh weather, there was a far greater impact in early 2014 when more of the country was affected (early 2014 averaged 80 mentions of weather per Beige Book).

Looking ahead, the fiscal concerns may pick up over the next several Beige Books if Congress doesn’t quickly address funding the U.S. government past September 30, 2015, which could lead to a full or partial shutdown of the U.S. federal government, and raising the debt ceiling, which the U.S. Treasury is likely to approach in late fall/early winter.

China had 11 mentions in the latest Beige Book, the most of any Beige Book this year. China averaged only 2 mentions per Beige Book from 2011 through 2014. As we noted in the Weekly Economic Commentary, “China Challenge,” while the Chinese economy has been slowing for more than five years, the news media and U.S. financial markets have only recently seemed to have taken note. Most of the mentions of China in the latest Beige Book were in a negative context, but many were also confined to the industrial or manufacturing sector. We expect China to be a key topic in the Beige Book for the foreseeable future.

OPTIMISM STILL RULES

Of the major transitory factors that impacted the economy and the Beige Book in early 2015 (dollar, oil, port strike, bad weather), only the strong dollar has lingered (34 mentions in September and 23 mentions in July 2015, versus 30 in June and 31 in April); however, neither the dollar nor the other headlines dampened the optimism on the economy that has picked up strength in the past year or so.

In the September 2015 Beige Book, the word “optimism” (or its related words) appeared 22 times, whereas the word “pessimism” appeared just once. Over the first 6 Beige Books of 2015, optimism has appeared, on average, 22 times per Beige Book, while the word pessimism has appeared a total of just 4 times across all 6 Beige Books in 2015, with 2 of the 4 mentions coming in the Dallas district, commenting on the outlook for the oil and gas sector.

As reassuring as it is to see that Main Street can remain optimistic despite the flow of bad news, the large number of optimistic comments in the Beige Book is not the start of a new trend: In the 8 Beige Books released in 2014, the word “optimism” appeared, on average, 30 times in each edition. In 2013, “optimism” appeared, on average, 25 times per Beige Book. In the 8 Beige Books released in 2009, during some of the worst of the financial crisis and Great Recession, the word “optimism” appeared, on average, just 9 times.

Concerns that the economic and market environment we are in today is similar to the period just prior to the onset of the Great Recession and around the stock market peak in late 2007 also appear to be well overdone. In the 8 Beige Books released in 2007, the word “optimism” appeared, on average, just 10 times per edition — a far cry from the 30 times per edition in the 8 Beige Books released in 2014 [Figure 5].

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide or be construed as providing specific investment advice or recommendations for your clients. Any economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal and potential illiquidity of the investment in a falling market.

Commodity-linked investments may be more volatile and less liquid than the underlying instruments or measures, and their value may be affected by the performance of the overall commodities baskets as well as weather, geopolitical events, and regulatory developments.