Executive Summary

- The economy is in the early stages of what could be a multi-year run for housing

- We are attempting to mitigate risk by selecting names with varying target markets and business approaches

- Industries beyond home builders should benefit from a resurgence in housing

- Our optimism is rooted in promising demographic trends

A series of false starts sums up the U.S. housing market’s recent past. Yet, we believe that pattern has reversed. The beginning stages of a multi–year boom that could benefit investors has begun, and low interest rates, demographics, and years of economic growth should provide a solid foundation for the sector.

Not Just Starter Homes. While much of investor focus has been on first–time buyers, the high–end of the market is also showing strength. Move–up homes in the $500,000 to $749,000 range year–to–date have enjoyed the largest growth in sales with an increase of 47% year over year, according to industry estimates.

We believe the boom will endure. Our focus has been on identifying undervalued stocks with idiosyncratic factors that should benefit from an upswing in housing.

Same Business, Different Approach. For example, by holding multiple home builders that operate in 12 states, we are attempting to mitigate regional risks. Our housing names also specialize in different types of properties. Longtime investment M.D.C. Holdings Inc. (MDC), generates roughly 40% of its sales through first–time buyers whereas portfolio holding WCI Communities (WCIC) focuses on higher–end dwellings in Florida. By owning construction companies with varying target markets, we believe we are able to mitigate risk tied to a single demographic group.

While we conscientiously seek to reduce risk by diversifying stock–specific factors, we seek consistency among holdings in regards to attractive valuations.

At 1.16x book value, M.D.C. is trading at a nearly 32% discount to its peers and features a 3.4% dividend yield compared to 0.5% for the industry average among North American builders. Additionally, on a price–to–sales basis the stock is trading at just 80% of its counterparts. We’ve been long–time owners of the company, which operates under the Richmond brand, due in part to its conservative approach in the space. Many builders stock up on vacant land which provides a tailwind during up markets as it appreciate housing inventory. When the market softens, undeveloped land often gets marked down and can sink formerly attractive balance sheets. M.D.C. keeps its land portfolio light, instead focusing on generating returns from building.

KB Home (KBH) is another holding trading at compelling valuations. KB takes a different approach to property inventory but one that we believe is also prudent. Post the credit crisis, the company focused on selectively acquiring land at attractive rates in markets that feature high household incomes and scarcity of buildable parcels. The strategy has created operating leverage for the company and should result in significant margin expansion as the real estate market continues to grow. At just 87% of book value and 10.4x next year’s estimated earnings despite five consecutive years of increasing sales, we believe the market isn’t fully appreciating the upside opportunity for the stock.

WCI owns or controls 13,500 home sites in the fast-growth Florida market, with a focus on coastal areas. We believe the company’s greater than a 10-year supply of land in a robust region is a key differentiator. Often, builders that hold significant acreage have weaker balance sheets. WCI is an exception with $146 million in cash and less than 20% net debt. Given the cost of its real estate is already largely realized, we believe its operating leverage results in greater upside potential than downside risk. The company saw new orders jump 53.8% in the second quarter of 2015 and its backlog grow by nearly 45%. As the pace of building quickens, we believe WCI’s land will prove a valuable asset to boost top-line growth. The company’s focus on serving second-home buyers and active adults as well as its higher average selling price of $476,000 provides another unique aspect that diversifies demographic risk in the portfolio.

Beyond the Builders. While owning construction companies is the most direct way to participate in the resurgence of housing, we believe the powerful trend will impact additional industries from raw materials to home décor.

The Paper and Forest Products industry is beginning to benefit from housing activity. While pricing has been under pressure for wood products due to softness in China, some of the weakness has been offset by demand from domestic construction. Producers expect prices will stabilize and demand in North America will continue to increase in response to an uptick in renovations, remodeling, and new construction. When that happens, we believe, the group’s performance should resume its historical correlation with housing as illustrated below.

Our holdings in the space are generally trading at discounts to peers and their five–year historical averages which, we believe, gives them additional downside protection while lumber prices stabilize.

Specialty Retail is an area that should benefit from household formation and can thrive whether people are building new homes or moving into apartments. Pier 1 Imports (PIR) is a company we’ve found attractive based on valuations and internal improvements and should also reap additional benefits from increased consumer focus on homes.

The company is in the early stages of improving its business. Pier 1 operates in the competitive home décor space and its margins have eroded due to promotional discounting and spending to strengthen its e–commerce presence. As profit levels compressed, valuations followed and, based on forward earnings, the stock now trades at a nearly 14% discount to its 10–year median price–to–earnings (P/E) of 14.8x. We believe online marketing efforts will be beneficial and the bulk of associated costs have already been expended.

The Numbers Behind our Optimism. According to recent census data, 30% of the 80 million people in the millennial generation live with their parents. That’s up from 23% for the same age group in 2000. Trends in household formation suggest many of those Millennials are starting to venture out of the nest. As the chart illustrates, the number of new households formed turned up significantly toward the end of 2014 and has continued to expand. Through the first half of 2015, the number of households has increased by 2.2 million compared to the same time a year ago. The flood of those moving out on their own should provide a pipeline of home buyers for the next several years.

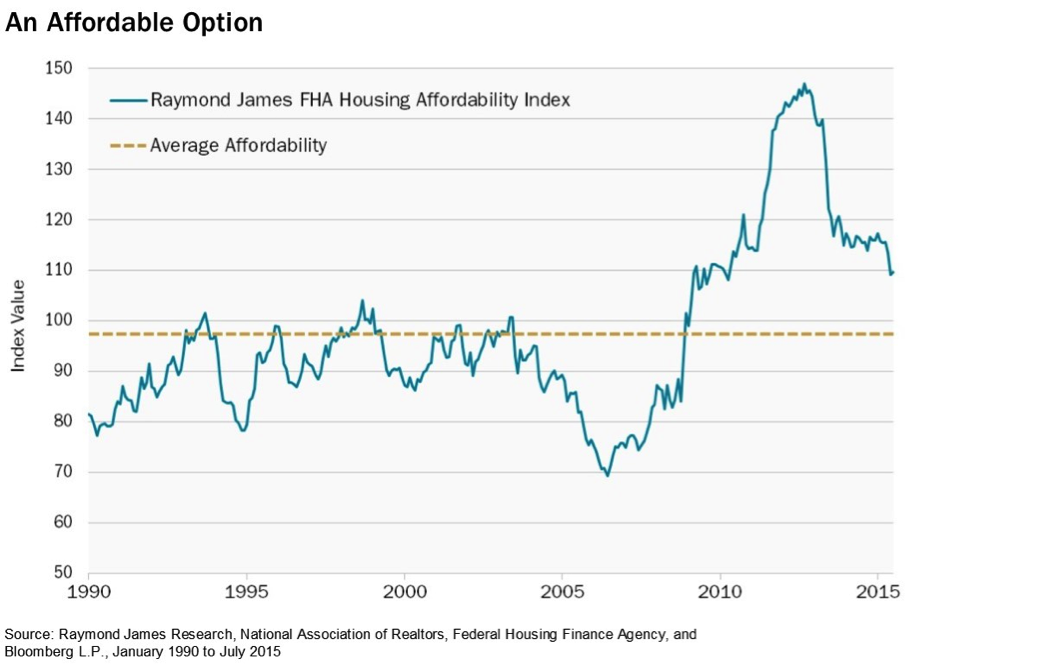

The explosion in household formation has put pressure on the rental market, which, in turn, is making home ownership financially attractive. Vacancy rates for rental properties hit a 10–year low at the end of the second quarter at 6.8% compared to the average of 9.1%. As excess apartment capacity has tightened, rents have edged up and are at all–time highs in nominal dollars. Meanwhile, housing prices are still more than 20% below their peak from 2006–07.

Historically low interest rates are more than 200 basis points lower than they were in late 2006, providing an additional discount for buyers. The upshot is that the difference in monthly payments between renting and owning has shrunk, making home ownership more attractive.

Budding wage pressure should also contribute to the affordability of housing. With unemployment hovering around 5.3%, the Federal Reserve has noted there is evidence that pay is beginning to creep up as some industries are competing to fill open positions. We expect that trend will continue.

Summary

While we believe there are several reasons for optimism regarding housing, recognizing an emerging theme is only the first step in capitalizing on an opportunity. We are convinced a focus on valuations, management and business strategy is key to identifying companies with the greatest chance for success. Additional analysis is then required to select a group of companies with unique attributes that together provide the greatest opportunity for success regardless of the nuances of how the broader theme plays out.

Disclosure:

Past performance does not guarantee future results

Investing involves risk, including the potential loss of principal. There is no guarantee that a particular investment strategy will be successful.

Value investments are subject to the risk that their intrinsic values may not be recognized by the broader market.

As of 6/30/2015, Heartland Advisors on behalf of its clients held approximately 5.58%, 1.72%, 0.82%, and 3.53% of the total shares outstanding of M.D.C. Holdings Inc., WCI Communities Inc., KB Home, and Pier 1 Imports, Inc., respectively. Statements regarding securities are not recommendations to buy or sell. Portfolio holdings are subject to change. Current and future holdings are subject to risk.

The statements and opinions expressed in this article are those of the presenter(s). Any discussion of investments and investment strategies represents the presenter’s views as of the date created and are subject to change without notice. The opinions expressed are for general information only and are not intended to provide specific advice or recommendations for any individual. The specific securities discussed above, which are intended to illustrate the advisor’s investment style, do not represent all of the securities purchased, sold, or recommended by the advisor for client accounts, and the reader should not assume that an investment in these securities was or would be profitable in the future. Certain security valuations and forward estimates are based on Heartland Advisors’ calculations. Any forecasts may not prove to be true. Economic predictions are based on estimates and are subject to change.

Industry and sector classifications for each security held in the composite are generally determined by referencing the Global Industry Classification Standard codes (GICS) developed by Standard & Poor’s and Morgan Stanley Capital International.

Data Sourced from FactSet: Copyright 2015 FactSet Research Systems Inc., FactSet Fundamentals. All rights reserved.

Definitions: Basis Point (bps): is a unit that is equal to 1/100th of 1% and is used to denote the change in a financial instrument. Book Value: is the sum of all of a company’s assets, minus its liabilities. Price/Book Ratio: of a company is calculated by dividing the market price of its stock by the company's per-share book value. Price/Earnings Ratio: of a stock is calculated by dividing the current price of the stock by its trailing or its forward 12 months’ earnings per share. Price/Sales Ratio: is the stock price divided by the sales per share for the trailing 12-month period. Raymond James FHA Housing Affordability Index: is a proprietary index based on median existing home prices, median household income, and prevailing Federal Housing Administration mortgage rates. S&P Composite 1500: combines three leading indices, the S&P 500, S&P MidCap 400, and S&P SmallCap 600 to cover approximately 90% of the U.S. market capitalization. All indices are unmanaged. It is not possible to invest directly in an index.

CFA is a trademark owned by the CFA Institute.

©2015 Heartland Advisors

heartlandadvisors.com

2015376/1015