Weighing the Week Ahead: Has the Fed Assumed a Third Mandate?

Despite many signs of economic improvement, the Fed chose to maintain policy accommodation at emergency levels. In a week that is light on data and long on speeches, this news will be enough to keep Fed policy at the forefront. The punditry will be asking:

Has the Fed Assumed a Third Mandate?

An Opportunity for Readers: Ask Me Anything

The AMA sessions are the rage these days, and I agreed to participate in one next week. I certainly do not have all of the answers. I have had success in figuring out where to look and identifying real experts on many topics. I answer as many questions as possible in the comments and via email, but I expect this session to be more wide-ranging.

Thanks to Scutify for inviting me. If readers are interested in asking something, you can do so in advance. The entire session will be available later as well, but I hope to interact with many at the scheduled time of 2PM EDT on Wednesday, 9/23. There is no charge, so I have some hope that the discussion will provide a net profit for participants!

Young Writers

Consider entering the competition for the Bracken Brower prize. You need to be under age 35 to compete for this very meaningful award.

Prior Theme Recap

In my last WTWA I predicted that it would be all Fed, all the time. That was an easy one! It was a sharply divided week, with a good-looking market into the Fed meeting and for a few minutes afterward. As he does each week, Doug Short’s recap describes the action with appropriate wariness about causality. As always, the full article includes several other helpful charts. (With the ever-increasing effects from foreign markets, you should also add Doug’s World Markets Weekend Update to your reading list).

The chart shows it as a flat week, but you can readily see why it did not feel that good. The week was good enough for the Texas boys to maintain the post-Cramer slot on CNBC, but another day or two of this will bring back “Markets in Turmoil.”

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead. You can make your own predictions in the comments.

This Week’s Theme

We are in the period before the important new earnings season. The economic calendar is a bit light. There is a strong focus on international issues. I expect plenty of attention to the meeting of Israel’s Prime Minister Netanyahu with Russia’s Vladimir Putin. Chinese President Xi Jinping Has a state visit to the U.S., including a summit meeting with President Obama. Pope Francis will also continue his tour, including a Presidential meeting on Wednesday.

The international theme comes in the wake of last week’s FOMC decision, which acknowledged the influence of foreign markets on the U.S. economy. The Fed has two legal mandates: maximizing employment and maintaining price stability. Through the mere mention of issues in China and emerging markets, the punditry has a fresh angle on their favorite topic: Criticizing the Fed. The question on the week will be:

Has the Fed taken on a new mandate?

As always, the viewpoints are varied.

The Viewpoints

The post-mortem Fed opinions include the following:

- The Fed failed on transparency, by not tipping off the decision in advance. (You just can’t make this stuff up).

- The Fed missed the chance to raise rates, and is already way too slow.

- The Fed needs to hurry to raise rates to that they can cut when the next recession hits. It is right around the corner.

- The Fed is warning about global economic weakness.

- The Fed is sending a muddled message.

- None of this was very relevant. Investors should tune out the noise.

As always, I have my own ideas in today’s conclusion. But first, let us do our regular update of the last week’s news and data. Readers, especially those new to this series, will benefit from reading the background information.

Last Week’s Data

Each week I break down events into good and bad. Often there is “ugly” and on rare occasion something really good. My working definition of “good” has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially – no politics.

- It is better than expectations.

The Good

There was a little good economic news.

-

High-frequency indicators are generally positive. New Deal Democrat’s indispensable weekly summary includes many indicators that get insufficient attention His conclusion reflects our theme this week:

Once again, those portions of the US economy most exposed to global forces have turned negative, while those most insulated from global problems are generally positive. With housing and motor vehicles still quite positive, I remain positive on the US economy at least through the second quarter of next year, and increasingly so as to the third quarter as well.

- Homebuilder confidence hit the highest level in ten years. (Calculated Risk).

- Q3 earnings estimates may be too pessimistic. Earnings guru Brian Gilmartin notes the expected decline of 2.8% and suggests that actual results might beat this target, especially in certain sectors. We will be following this subject very closely in a few weeks.

- Initial jobless claims moved even lower, to 264K. Bespoke compares the results to post-recession lows, showing their typical great charts for NSA data as well as the seasonally adjusted series. Here is the chart for the four-week moving average, a popular way of following this noisy series.

- Home equity has improved to over 56%, close to pre-2006 levels. U.S. residents have more wealth and less leverage. Scott Grannis has a list of key topics and charts, including this one:

The Bad

There was also some negative news last week.

- Rail traffic declined significantly, reversing last week’s spike higher. Steven Hansen at GEIexplores the data and possible reasons.

- Technical weakness. Bespoke notes that all ten S&P sectors are in downtrends. See the full post for a discussion of the market implications and additional charts. Charles Kirk (small subscription required and well worth it) reviews the failed bullish setups from recent trading and the significance for the coming week. Charles is always flexible in his preparation – willing to shift with the evidence.

- Industrial production fell a bit more than expected.

- Retail sales rose slightly less than expected.

- Housing starts were weaker than expected, although building permits were a bit stronger. Calculated Risk has the full story and some helpful charts.

- The Philly Fed showed contraction. Steven Hansen at GEI analyzes this noisy series while underscoring the most important components.

The Ugly

Manipulation of Treasury Rates? While still just an investigation, there is a big-bank pattern involving other markets. (Bloomberg View).

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. Think of The Lone Ranger. No award this week. Nominations are always welcome.

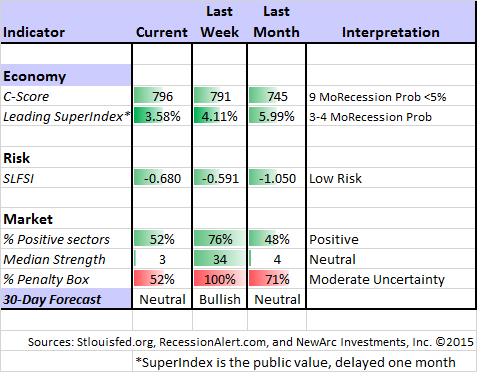

Quant Corner

Whether a trader or an investor, you need to understand risk. I monitor many quantitative reports and highlight the best methods in this weekly update.

Recent Expert Commentary on Recession Odds and Market Trends

Bob Dieli does a monthly update (subscription required) after the employment report and also a monthly overview analysis. He follows many concurrent indicators to supplement our featured “C Score.”

Doug Short: Provides an array of important economic updates including the best charts around. One of these is monitoring the ECRI’s business cycle analysis. Jill Mislinski has joined Doug’s team and provides this week’s update. The ECRI’s most recent article suggests that U.S. economic growth has been declining for eighteen months according to their indicators. They have continued in the chorus of Fed critics. While eventually stepping back from their mistaken and insistent recession call in 2011, ECRI has remained persistently bearish on economic growth.

RecessionAlert: A variety of strong quantitative indicators for both economic and market analysis. While we feature the recession analysis, Dwaine also has a number of interesting systems. These include approaches helpful in both economic and market timing. He has been very accurate in helping people to stay on the right side of the market.

Georg Vrba: An array of interesting systems. Check out his site for the full story. We especially like his unemployment rate recession indicator, confirming that there is no recession signal. He gets a similar result from the Business Cycle Indicator.

Financial Stress. I have been featuring the SLFSI for years, after making it one of our summer research projects. More complete findings are available upon request, but here were two key conclusions:

- This is not a market-timing tool, but a measure of risk.

- The important risk threshold is somewhere around 1.1.

We are not even close to a high risk level.

The Week Ahead

It is a modest week for economic data. I highlight what I see as important. For a comprehensive listing I use Investing.com. You can filter for country, type of report, and other factors.

The “A List” includes the following:

- New home sales (Th). Important for a continuing economic recovery.

- Initial jobless claims (Th). The best concurrent news on employment trends, with emphasis on job losses.

- Michigan sentiment (F). Any rebound from weakness in preliminary read? Useful indicator of job creation and spending.

The “B List” includes the following:

- Existing home sales (M). Less direct economic significance than new sales, but a good read on the strength of the market.

- Durable goods (Th). Weak report expected, but a volatile series.

- Crude oil inventories (W). Current interest in energy keeps this on the list of items to watch.

- GDP Q2 final (F). “Old news” still sets the baseline for measuring economic progress.

In addition to the big week for leaders on the world stage, central bankers will have more to say. Someone will be talking every day, but watch especially for ECB head Draghi on Wednesday, Fed Chair Yellen on Thursday, and St. Louis Fed President Bullard on Friday.

I will also be watching for earnings pre-announcements.

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a “one size fits all” approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

Insight for Traders

Felix has switched to neutral after the wild swings and failed rally of last week. Felix is still fully invested because there are several remaining pockets of strength. The confidence in this three-week forecast is now stronger than it has been in recent weeks. For more information, I have posted a further description — Meet Felix and Oscar. You can sign up for Felix’s weekly ratings updates via email to etf at newarc dot com. Felix appears almost every day at Scutify.

Steve Burns has a good list of why most traders are not profitable. My favorites are proper tracking of commission costs and excessive size. You cannot turn a poor system into a good one through money management, but you can go broke despite a good method. Traders take excessive size because the focus on what they want to make rather than what they can afford to risk.

Tradeciety focuses on stop losses, with a nice list of seven common mistakes.

Insight for Investors

I review the themes here each week and refresh when needed. For investors, as we would expect, the key ideas may stay on the list longer than the updates for traders. Major market declines occur after business cycle peaks, sparked by severely declining earnings. Our methods are focused on limiting this risk. Start with our Tips for Individual Investors and follow the links.

We also have a page summarizing many of the current investor fears. If you read something scary, this is a good place to do some fact checking.

Other Advice

Here is our collection of great investor advice for this week.

If I had to pick a single most important article, it would be Morgan Housel’s 50 Reasons We’re Living Through the Greatest Period in World History. Morgan has a great lead, emphasizing the health progress over the last 30 years. Since I have lost several family members to breast cancer, this hit home for me:

Consider this: In 1900, 1% of American women giving birth died in labor. Today, the five-year mortality rate for localized breast cancer is 1.2%. Being pregnant 100 years ago was almost as dangerous as having breast cancer is today.

The problem, the doctor said, is that these advances happen slowly over time, so you probably don’t hear about them. If cancer survival rates improve, say, 1% per year, any given year’s progress looks low, but over three decades, extraordinary progress is made.

Compare health-care improvements with the stuff that gets talked about in the news — NBC anchor Andrea Mitchell interrupted a Congresswoman last week to announce Justin Bieber’s arrest — and you can understand why Americans aren’t optimistic about the country’s direction. We ignore the really important news because it happens slowly, but we obsess over trivial news because it happens all day long.

This list is so good that it is difficult to pick some favorites, but try these:

5. The average American now retires at age 62. One hundred years ago, the average American died at age 51. Enjoy your golden years — your ancestors didn’t get any of them.

9. No one has died from a new nuclear weapon attack since 1945. If you went back to 1950 and asked the world’s smartest political scientists, they would have told you the odds of seeing that happen would be close to 0%. You don’t have to be very imaginative to think that the most important news story of the past 70 years is what didn’t happen. Congratulations, world.

10. People worry that the U.S. economy will end up stagnant like Japan’s. Next time you hear that, remember that unemployment in Japan hasn’t been above 5.6% in the past 25 years, its government corruption ranking has consistently improved, incomes per capita adjusted for purchasing power have grown at a decent rate, and life expectancy has risen by nearly five years. I can think of worse scenarios.

35. In 1900, 44% of all American jobs were in farming. Today, around 2% are. We’ve become so efficient at the basic need of feeding ourselves that nearly half the population can now work on other stuff.

47. According to AT&T archives and the Dallas Fed, a three-minute phone call from New York to San Francisco cost $341 in 1915, and $12.66 in 1960, adjusted for inflation. Today, Republic Wireless offers unlimited talk, text, and data for $5 a month.

48. In 1990, the American auto industry produced 7.15 vehicles per auto employee. In 2010 it produced 11.2 vehicles per employee. Manufacturing efficiency has improved dramatically.

Reading the list reminds you of the great progress on so many fronts, despite the persistent focus on negative news and trivia. Much of this progress is not captured in official GDP figures. Everyone talks about health costs without noting how much progress there has been. Jobs “lost” in farming and auto manufacturing reflect productivity improvement, shifting opportunity elsewhere.

And it is also something to keep in mind the next time someone bases a theory on stock data from the 19th century!

Stock Ideas

Time to roll the dice on Macau gambling? Barron’s has a bullish article on Steve Wynn and Wynn Resorts (WYNN). They discuss a possible 50% gain in the stock and Wynn’s reasons for expecting supportive policy from the Chinese government.

Chuck Carnevale’s articles always provide a great mix of instruction and specific ideas. He continues his powerful series on retirement investing with an excellent discussion on how to pick the right type of stock for your specific needs. As usual there many good ideas (several of which we own), and you will learn how to assemble different stock types in an effective portfolio. You will also learn how to use Chuck’s FAST graphs, an indispensable tool.

Philip van Doorn (MarketWatch) identifies ten attractive stocks using sales, profits and earnings as criteria. I am always interested in these lists when some of our holdings are included, and we have two of these. I am looking at the others!

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for over ten years. The average investor should make time (even if not able to read every day as I do) for a weekly trip on Wednesday. Tadas always has first-rate links for investors in this special edition. As always, there are several great links, but I especially liked this sound advice about talking retirement with young people. Ben Carlson explains that retirement saving does not seem relevant to them, yet it is the very best time to start.

I took up this subject last year, promising to follow up with more. The original article is still relevant, but I have not added as much material as I hoped to. It is on my agenda.

Beware

Wild trading in ETFs present a risk for investors (WSJ). Be especially careful with market orders, but other intra-day pricing may still be an issue.

Trading in the morning may be the worst time for investors (WSJ).

It is tougher than you think to get commodity exposure through equity investments (Alpha Architect).

Final Thought

I’ll weigh in on each of the question from the introduction, and emphasize a few investment themes.

-

Concerning transparency, few understand what these means.

- It does not mean announcing results before the meeting. Former Dallas Fed President Bob McTeer explains that members do not know the outcome in advance. They do not even discuss the issue in advance. The meeting matters.

- It does not mean an “open meeting.” Good decisions require consideration of many possibilities – even the unlikely ones. Ideas can be floated, considered, and refuted. This is the reason that full transcripts are delayed for five years.

- The Fed is much more transparent than it was twenty years ago, but it seems only to provide more opportunity for speculation.

- Concerning timing of the first hike, I see little relevance to knowing the exact date. I suggested last week that it was much ado about nothing, and so it was. The overall path of increases is most important, and that will be gradual.

- Concerning the need to raise to permit a recession-fighting reduction later, this is a silly argument. Rate tightening cycles often create recessions. There is plenty of time left in this business cycle. This argument is most frequently raised by those who have been totally wrong about the economy and the stock market. They seem to seek something that will choke off growth.

- Concerning the Fed’s message about global economic weakness, there is no fresh information about the facts. The Fed produced no data that was not already widely known. The only new information is that, consistent with the urging of many sources, the Fed is cautiously calibrating the impact of global growth on the U.S. economy before taking any action.

- Concerning the Fed’s muddled message, some seem to embrace nuanced statements to suit their own purposes. Noting that the U.S. economy is solid and international markets are weaker is not “muddled.”

Let us turn back to Morgan Housel’s fine list for an interesting conclusion on the success of the Fed.

40. Annual inflation in the United States hasn’t been above 10% since 1981 and has been below 5% in 77% of years over the past seven decades. When you consider all the hatred directed toward the Federal Reserve, this is astounding.

The main investment angle from the Fed news is to take advantage of the over-reaction. I expect a week full of clarifying Fed speeches (already started) and some better earnings data to come. I continue to like regional banks, technology, consumer discretionary, and some cyclical stocks.