While our gut instincts and quantitative disciplines aren’t always in agreement, that conflict doesn’t exist today. The evidence comes down decisively in the “bear market” camp—although, as noted, the S&P 500 decline of 12.4% (to-date) barely meets our definition of a severe correction.

While possibly too simplistic, our bear market argument boils down to this:

BEFORE: The action leading up to the S&P 500 bull market high of May 21st traced out a “textbook” top in many ways. Granted, divergently strong action in certain areas (NASDAQ, Small Caps, Financials) following that top added a bit of confusion to an otherwise straightforward picture. (Then again, every market top presents a few such anomalies. It’s part of the bear’s job.) While market action was the primary trigger to the timing of our bearish call, factors like valuations, investor sentiment, and possibly even monetary conditions (“tapering” as tightening) conformed more or less to the patterns leading up to past market peaks.

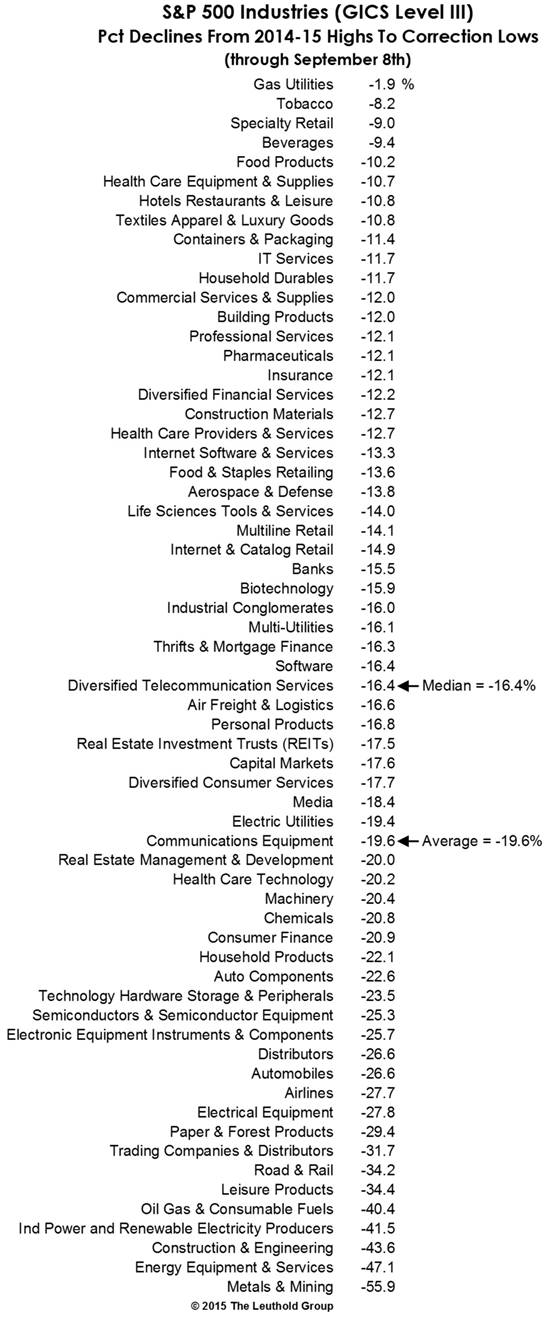

AFTER: The action subsequent to the S&P 500 high of May 21st has bear paws all over it. In late August, multiple measures of downside momentum sunk to levels rarely seen outside of bear markets. Damage has been broad; the average industry within one of the strongest indexes globally—the S&P 500—has already suffered an average peak-to-trough loss of 19.4%. And foreign stocks, despite their substantially lower valuations, have lived up to the bear market “betas” they’ve exhibited in the past. Yet, sentiment remains broadly in the “buy the dip” mindset, despite the serious nature of these breakdowns.

© 2015 The Leuthold Group