Key Points

▪ Janet Yellen’s comments last week increased the likelihood for a rate increase in 2015, which would be good news for equities.

▪ U.S. economic growth and corporate earnings trends should both improve.

▪ Volatility may persist for some time, but we still have a favorable view toward equities.

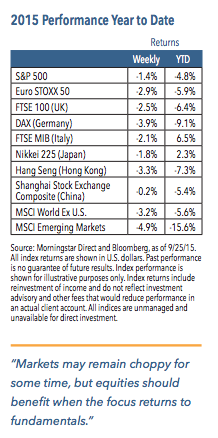

Sentiment was negative for most of last week, as investors focused on continued uncertainty over Federal Reserve policy, slowing growth in China and emerging markets and ongoing weakness in commodities. Stock prices bounced on Friday following comments from Fed Chair Janet Yellen that a rate increase was looking more likely in 2015. Nevertheless, equities finished in negative territory, with the S&P 500 Index falling 1.4%.1 The health care, materials and industrials sectors came under pressure, while utilities, consumer staples and financials finished higher.1

Weekly Top Themes

1. Second quarter growth was revised higher. Real gross domestic product growth was revised from 3.7% to 3.9%, helped by improved retail sales figures.2 Looking ahead, we expect sales figures will continue to drive growth higher, but we also anticipate a drag from a drawdown in high inventory levels.

2. Janet Yellen’s comments increased the odds that the Fed would raise rates later this year. Her speech last week was more clear than the statement that accompanied the September policy meeting. The Fed Chair cited a reasonably solid economy and an improving labor market as reasons to justify a rate increase. She also pointed out that inflation remains below target, but indicated that global pressures may be transitory.

3. For U.S. corporations, domestic profits should continue to outpace non-U.S. profits. At present, U.S. domestic corporate profits are approximately two-anda-half times higher than non-U.S. profits.3 If the U.S. economy can remain relatively decoupled from the rest of the world, we expect this trend will persist.

4. The near-term direction of equity markets looks uncertain. Following the sharp pullback in August, markets appear to be trying to form a base. We expect that the next significant trend in equities will depend on economic growth and earnings results in 2016. At present, indications for both are murky.

5. Active managers have become less correlated to the broader market, which could be a bullish signal. Recently, the beta for hedge funds has fallen and is now close to zero, while the beta for actively managed mutual funds is 0.85, both three-year lows.4 These beta levels have has fallen sharply over the last month,4 which may indicate opportunities for equities to move higher when fundamental conditions look more certain.

We Still Favor Equities over the Long Term

U.S. equities are likely to struggle until it becomes more clear that China’s economy will stabilize and the Fed will start lifting rates. The good news is that we expect both of these to happen, but another risk lies on the horizon. The possibility of another U.S. government shutdown looms, and John Boehner’s decision to resign likely increases the odds of a standoff over government spending. The current continuing resolution should keep the government funded through December 11, when the debt ceiling will need to be raised. This is an issue that could drive market volatility higher.

For now, the main focus for investors continues to be Fed policy. We think we’ll need to see clear indications from the Fed that it will begin moving rates higher for equities to sustain a rally. The delay in starting an increase cycle acts as a headwind for equities since it potentially fuels price imbalances, exacerbates the possibility of asset price bubbles, increases uncertainty and could force the Fed into tightening at a faster pace than it wants to. Ultimately, a risk-averse Federal Reserve attuned to promoting economic growth should be a positive for risk assets, including stocks. In the near-term, however, the delay and uncertainty is keeping equity prices in check and is putting downward pressure on bond yields.

Financial markets may remain choppy for some time, but we expect investors will eventually return to focusing on fundamentals, which should benefit equities. We believe the global economy should continue to grow unevenly and corporate earnings should improve. As a result, we continue to favor equities over bonds and cash. We also have a particularly positive view toward cyclical equity sectors and markets that are not tied to commodities.

1 Source: Morningstar Direct, as of 9/25/15

2 Source: Commerce Department

3 Source: Cornerstone Macro

4 Source: FundStrat Global Advisors. Beta is a measure of the variability of the change in the share price for a fund in relation to a change in the value of the market. Funds with betas higher than 1.0 have been, and are expected to be, more volatile than the market; funds with betas lower than 1.0 have been, and are expected to be, less volatile than the market.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

©2015 Nuveen Investments, Inc. All rights reserved.