Weighing the Week Ahead: Will global weakness drag down the U.S. economy?

The recent Fed non-decision on interest rates increased worries about global economic weakness. Trading in commodity markets underscores a widespread perception of a potential recession. The week ahead is packed with fresh economic data, including the most important reports. The punditry will be asking:

Will the U.S. economy succumb to global weakness?

Young Writers

Consider entering the competition for the Bracken Brower prize. You need to be under age 35 to compete for this very meaningful award. Entries close on 9/30 at 5 PM British Summer Time, so do not delay further.

Prior Theme Recap

In my last WTWA I predicted that it would be a week for Fed critiques and reviews, including commentary and speeches from the actual participants. I expected the Fed to “clarify” the message that many took from the post-decision announcement. That was a fairly accurate guess for the major theme, but there was plenty of competition from the Pope, the President of China, and the Speaker of the House. The S&P 500 declined 1.36% on the week, with the NASDAQ and small stocks doing worse. To put this in perspective, here is a different chart from Doug Short’s excellent weekly recap – a look back over nearly two years. As always, the full article includes several other helpful charts. (With the ever-increasing effects from foreign markets, you should also add Doug’s World Markets Weekend Update to your reading list).

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead. You can make your own predictions in the comments.

This Week’s Theme

The Fed is concerned about the global economy. Or maybe not. Markets trade daily on a risk on, risk off basis, led by commodity and energy prices. Many believe that the U.S. economy is on life support. With plenty of economic data on tap we have new evidence for the ongoing debate. I expect the pundits to be asking:

Will the US economy succumb to global weakness?

As always, the viewpoints are varied.

The Viewpoints

The wide range of economic forecasts includes the following:

- The U.S. is already in a recession. QE4 is needed. The ECRI has a creative recession definition supporting this. (Via Doug Short).

- Market indicators suggest that a recession is imminent.

- The economy is showing modest growth, but we have an earnings recession. (FactSet’s Q3 estimates call for a decline of 4.5%, which would be the first two-quarter decline since 2009). Brian Gilmartin notes that full-year 2015 will probably be positive.

- Sluggish growth continues, overcoming the global drag, but only weakly. The Atlanta Fed’s GDP Nowproject presents this picture:

- Growth is improving, but gradually. (This is the mainstream economic viewpoint – major economists and the Fed. For specific China attention see also Dallas Fed via GEI).

- Q2 signaled the start of a real economic rebound.

Josh Brown has a good discussion of this. While the economic debate is important, the major focus remains with the risk-on, risk off psychology.

As always, I have my own ideas in today’s conclusion. But first, let us do our regular update of the last week’s news and data. Readers, especially those new to this series, will benefit from reading the background information.

Last Week’s Data

Each week I break down events into good and bad. Often there is “ugly” and on rare occasion something really good. My working definition of “good” has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially – no politics.

- It is better than expectations.

The Good

There was some good economic news.

- China – Nike. Nike joins the list of consumer-oriented companies that are doing well in China. (But see bad news below). Might there be a lesson here?

- Euro zone banks are well-capitalized. ECB head Draghi elaborates.

- Government shutdown odds decline. Putting aside the underlying policy issues, the market does not like shutdowns. The factors behind the Boehner resignation are complicated, but the immediate implication is that the shutdown issue will be delayed for a few months. Jeffry Bartash at MarketWatch has the story. We’ll get more discussion and analysis in the Sunday talk shows.

- Michigan sentiment. The final read for September was a slight beat of expectations, but still pretty soft. As always, I recommend the Doug Short analysis and a chart that brings several different variables into focus.

- New home sales beat expectations. Calculated Risk notes the 21.1% increase over last year as well as the strong YTD numbers. Inventories are lower.

New highs in bearishness – a contrary indicator. Mark Hulbert has the story.

The Bad

There was also a little negative news last week.

- China – Caterpillar. Companies strongly and directly tied to Chinese manufacturing continue to struggle. (But see good news above). Might there be a lesson here?

- CFOs see the market as overvalued. So say the results of the annual Duke survey, which looks at worldwide markets.

- Durable goods orders declined and slightly missed expectations. Steven Hansen at GEI has the full story, also noting that a three-month rolling average may be a better take on this volatile series.

- Existing home sales missed expectations. Calculated Risk comments.

The Ugly

Volkswagen deception. This story is generating plenty of collateral damage. Looking beyond the future of the company itself, there are questions about the overall Germany economy (autos make up 17%) and possible offenses by competitors. Auto sales have been an economic bright spot, so even a delay in purchase decisions represents an important drag. (Kevin Roose has a good summary of the issues).

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. Think of The Lone Ranger. No award this week. Nominations are always welcome.

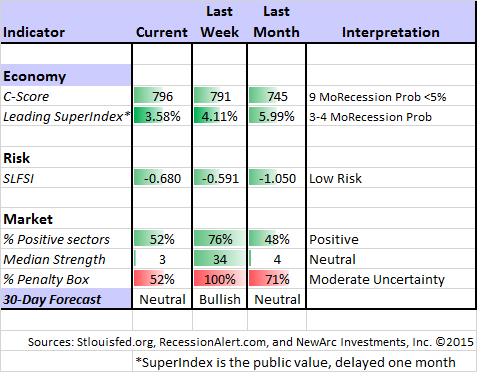

Quant Corner

Whether a trader or an investor, you need to understand risk. I monitor many quantitative reports and highlight the best methods in this weekly update. For more information on each source, check here.

Recent Expert Commentary on Recession Odds and Market Trends

Bob Dieli does a monthly update (subscription required) after the employment report and also a monthly overview analysis. He follows many concurrent indicators to supplement our featured “C Score.”

Doug Short: Provides an array of important economic updates including the best charts around. One of these is monitoring the ECRI’s business cycle analysis. Jill Mislinski has joined Doug’s team and provides this week’s update. The ECRI’s most recent article suggests that U.S. economic growth has been declining for eighteen months according to their indicators. They have continued in the chorus of Fed critics. While eventually stepping back from their mistaken and insistent recession call in 2011, ECRI has remained persistently bearish on economic growth.

RecessionAlert: A variety of strong quantitative indicators for both economic and market analysis. While we feature the recession analysis, Dwaine also has a number of interesting systems. These include approaches helpful in both economic and market timing. He has been very accurate in helping people to stay on the right side of the market.

Georg Vrba: An array of interesting systems. Check out his site for the full story. We especially like his unemployment rate recession indicator, confirming that there is no recession signal. He gets a similar result from the Business Cycle Indicator. Georg

Georg also analyzes the market after a “Death Cross” event – often a weaker market, but not a time to panic. His work was featured in this Seeking Alpha article.

The Week Ahead

It is a huge week for economic data. There are many items, even when I highlight only the most important. For a comprehensive listing I use Investing.com. You can filter for country, type of report, and other factors.

The “A List” includes the following:

- Employment report (F). Despite the wide error band on monthly changes, this is remains most important for markets and pundits.

- ISM index (Th). This measure of manufacturing might dip to 50, which will be misperceived by nearly everyone. That level for manufacturing corresponds to growth of over 2% in the service-centric U.S. economy.

- Consumer confidence (T). The Conference Board version is a helpful read on job creation and consumer spending.

- ADP employment (W). A strong alternative measure of job growth.

- Auto sales (Th). Will this important source of strength continue?

- Personal income and spending (M). A key economic indicator. Will recent strength continue?

- Initial jobless claims (Th). The best concurrent news on employment trends, with emphasis on job losses.

The “B List” includes the following:

- Pending home sales (M). Less direct economic significance than new sales, but a good read on the strength of the housing market.

- PCE prices (M). This is the Fed’s favorite inflation indicator, and it remains well below the target of 2%.

- Chicago PMI (W). The best of the regional indexes, and a hint for Thursday’s ISM report.

- Construction spending (Th). Volatile August data, but a key market sector.

- Crude oil inventories (W). Current interest in energy keeps this on the list of items to watch.

Once again there will be plenty of FedSpeak, but probably no more “clarification.” French President Hollande, German Chancellor Merkel, meet with Putin and Ukrainian President Poroshenko on Friday. I am not holding out a high level of hope, but any progress would be welcome. Few understand how much of a drag the Ukraine conflict has created for the world economy.

There is also the possibility of a government shutdown beginning Thursday. Were that to occur, we might not get the employment data.

I will also be watching for earnings pre-announcements.

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a “one size fits all” approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

Insight for Traders

Felix has remained neutral, although weakness last week puts us on the edge of a bearish call. Felix is still fully invested because there are several remaining pockets of strength. The confidence in this three-week forecast is now stronger than it has been in recent weeks. For more information, I have posted a further description — Meet Felix and Oscar. You can sign up for Felix’s weekly ratings updates via email to etf at newarc dot com. Felix appears almost every day at Scutify.

This interview with Dr. Brett Steenbarger is worth the time to listen.Creativity can be learned!

Insight for Investors

I review the themes here each week and refresh when needed. For investors, as we would expect, the key ideas may stay on the list longer than the updates for traders. Major market declines occur after business cycle peaks, sparked by severely declining earnings. Our methods are focused on limiting this risk. Start with our Tips for Individual Investors and follow the links.

We also have a page summarizing many of the current investor fears. If you read something scary, this is a good place to do some fact checking.

Other Advice

Here is our collection of great investor advice for this week.

If I had to pick a single most important article, it would be this advice from the SEC (via GEI, where there is abundant information on related topics) about investment scams on radio shows. There are plenty of good tips. Any investment source could include these scams, but radio claims are harder to check.

Stock Ideas

How many stocks should you hold? How should you determine the weighting? Chuck Carnevale considers these important and oft-neglected questions.

Barron’s has a nice feature with value investor John Buckingham. He discusses several of this week’s issues and provides quite a few ideas for value investors.

The Business Cycle

Monevator has an interesting collection of charts about the business cycle. If you can figure out where we stand, you can choose the best sectors and stocks. Here is one example:

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for over ten years. The average investor should make time (even if not able to read every day as I do) for a weekly trip on Wednesday. Tadas always has first-rate links for investors in this special edition. As always, there are several great links, but I especially liked this discussion of common retirement blind spots (Morningstar). And should you go for early Social Security benefits? (Bloomberg).

Bear Market or Correction

I rarely find these debates to be helpful. I think we have better methods for spotting and avoiding major declines, so someone’s definition of a “bear market” is usually not helpful. Whenever there is a decline from the highs, some will cite it as a minor correction while others see it as the start of the next “big one.”

Saying “no” to the bear market is The Fat Pitch. You can feast on plenty of charts, including the one below:

Cam Hui surveys both technical and fundamental indicators in his balanced take. He writes as follows:

I have received a fair amount of feedback, mostly from technicians and chartists, on my view that the idea that downside risk on stock prices is limited and this is not the beginning of a major bear market. I want to clarify my views on that topic.

For illustration I am including this post from Steve Burns, whom I like to cite on trading matters. Read the article for yourself, but to me, it seems to start with the conclusion and go from there. In particular, I reject the idea that those who disagree with his conclusions are necessarily “perma-bulls.” The issues are much more complicated than he seems to acknowledge.

Beware about Bonds

Colin Barr (WSJ) has an excellent description of trends in the bond market and current risks. This article is the start of the series, which I urge readers to follow carefully. Here is a key concern:

Domestically, the rise of large bond funds has created new risks. As the funds have grown, so has cross-ownership of the same bonds, increasing the likelihood of contagion if one manager starts selling, the International Monetary Fund says. Regulators worry that many investors may not know what is in their funds. A market downswing could lead to rising redemptions of fund shares, prompting funds to sell assets to raise cash and amplifying selling pressure across the market.

Final Thought

I am confident of our recession indicators, which provide a lot of lead time as well as support from concurrent evidence. Most of what gets written on popular blogs has little basis in sound research. A common mistake is confusion over the role of the NBER, which does the official recession dating after all data become available. Unlike our regular sources, they do not and should not try to make contemporaneous recession calls, and they certainly do not make forecasts. You can save a lot of time by simply moving on whenever you see something that makes this basic blunder.

There is a persistent trading dynamic which is important for both traders and investors. It includes the following:

- There is a piece of news, perhaps minor, perhaps totally bogus, and perhaps just speculative.

- The fastest traders and algorithms act instantly in the indicated direction, often using ETFs.

- Slower traders join in, going with the flow.

- Pundits impute major significance to the event, filling air time and media space.

- Readers and viewers join the party, probably on the wrong side and definitely too late to profit.

Rinse, lather, repeat.

Here are several example themes from last week:

- China. There is a small miss in a barely-understood survey of 500 people. It is trumpeted as big news on China and therefore big news about the world economy. The result is a decline in economically sensitive stocks that have no direct China exposure. (Alliance Bernstein).

- Biotech. A Presidential candidate tweets about drug prices. Biotech stocks decline 5% in a matter of minutes. (Eddy Elfenbein) The election is sixteen months away. No one knows whether Clinton will be elected or even will win the nomination. If elected, the path to drug price control is a difficult one. Exacerbating the effect is that biotech ETFs take down every stock, regardless of characteristics.

- Auto news. We learn something about Volkswagen, which could actually be a positive for competitors. In the current market it is interpreted as negative for every auto company.

- Oil prices. This is the most important. The market is trading with a strong correlation to oil prices. Art Cashin mentions it daily and veteran observer Art Hogan says it has been a “lockstep” relationship for weeks. If you were using this indicator on an examination you would get an “F.” Prices include both supply and demand. Global demand has actually increased this year, even more than last year. It is not a sign of weakness. The trading works only because “everyone else” has the same illusion.

Trading and Investment Conclusions

If you are a trader, like Felix, these are treacherous waters. You can see the early reaction, but the algorithms and many other traders will be faster than you are. Unless you think that the initial move is too small, you are too late to trade. I see too many traders who have excessive confidence and probably excessive size. If you are a short-term trader you should beware of getting too big with your positions.

If you are an investor, the prospects are much better. As long as you focus on the long run, irrational dips in prices provide opportunity.

Reacting to the China theme, you have discount prices on anything related to the consumer economy.

On the biotech theme we have some aggressive positions mentioned in past articles and drawing on the excellent updates from John McCamant’s Medical Technology Stock Letter. Some are aggressive (ZIOP and NVAX) and others suited for a wide range of investors (GILD).

For autos, the entire sector is good, but I like the Ford F150 introduction. Since I expect modest growth, we sell calls against the position, getting expected appreciation, dividends, and call premiums.

For energy, I like mid-cycle stocks outside of the sector. This economic sector had a sharp decline and a gradual rebound. The time before the next business cycle peak is more than one year away and might be several. This is good for financial and technology stocks, and eventually for energy and materials. Regional banks remain a relatively safe choice, as do stocks like Apple (AAPL).