KEY TAKEAWAYS

· Non-energy companies may potentially grow earnings by 10% during the third quarter, excluding the impact of currency fluctuations on profits earned overseas.

· The potential acceleration in earnings growth over the next few quarters is one of several reasons we expect stocks to finish the year strongly.

· However, reaching our 5 – 9% S&P 500 total return forecast for 2015* following the latest correction may be difficult.

The Source

Different sources such as FactSet, Bloomberg, and others have different calculations than Thomson Reuters for S&P 500 earnings, based on various methodologies and different interpretations of what constitutes operating earnings.

*Historically since WWII, the average annual gain on stocks has been 7 – 9%. Thus, our forecast is in-line with average stock market growth. We forecast a 5 – 9% gain, including dividends, for U.S. stocks in 2015 as measured by the S&P 500. This gain is derived from earnings per share (EPS) for S&P 500 companies assuming mid-single-digit earnings gains. Earnings gains are supported by our expectation of improved global economic growth and stable profit margins in 2015.

Third quarter earnings season will potentially look a lot like the second quarter. This quarter’s earnings preview could almost be a copy and paste of the second quarter preview: It looks like we will get meager earnings growth, if we get any at all. The media will again tout earnings recession, which we discussed on April 6, 2015. The big headwinds from energy sector weakness and a strong U.S. dollar remain. And the big overseas worries are again unlikely to have much impact on earnings overall, as business conditions in the U.S. — outside of the energy sector — are pretty good. However, several things make this quarter more interesting, as we discuss below.

MORE OF THE SAME (NOT THAT BAD)

The third quarter of 2015 may look a lot like the second quarter in terms of the limited earnings growth the S&P 500 will likely produce (at best). The dual drags of depressed energy sector profits and a strong U.S. dollar are likely to sap what would otherwise be healthy earnings gains. Consensus estimates from Thomson Reuters are calling for a 4% year-over-year decline in S&P 500 earnings (other data sources have slightly different but generally lower numbers).

Breaking earnings down reveals a more encouraging picture of corporate America’s earnings power. Based on a quiet earnings preannouncement season, we expect at least 4% upside to published forecasts, in-line with last quarter and the long-term average. If we then remove the energy sector [Figure 1], where temporary outsized declines in earnings are about a 7% drag on overall S&P 500 profits, earnings get a big bump up. Finally, if the temporary drag from U.S. dollar strength is excluded (though it will be with us for a while longer), we estimate earnings get bumped up by another 3 – 4%.

Adding this up, non-energy companies may potentially grow earnings by 10% during the third quarter, excluding the impact of currency fluctuations on profits earned overseas. That’s pretty good underlying earnings power and speaks to the health of the broader U.S. economy.

The revenue story looks similar to the earnings story in the third quarter. S&P 500 revenue will possibly be down about 3% again this quarter, but would be solidly positive without the drags from energy and the U.S. dollar. Historically, revenue growth tracks growth in gross domestic product (GDP), including inflation, which we expect to be over 3% this quarter — after coming in at about 5% in the second quarter. Revenue growth will fall well short of that target in the third quarter; but the size of the gap, we believe, indicates better underlying revenue production and an upward trajectory.

WHAT MAKES THE THIRD QUARTER DIFFERENT?

Although many similarities exist between the upcoming earnings season and the last one, there are some notable differences. The big one is that stocks have fallen heading into this earnings season (the S&P 500 fell 12% peak to trough from July 20, 2015, through August 25, 2015). Given this latest stock market correction was the first drop of more than 10% in four years, it has been a while since investors were as negative as they are now heading an earnings reporting season. Surveys also suggest widespread investor pessimism, meaning we may be set up for a potentially positive reaction to results.

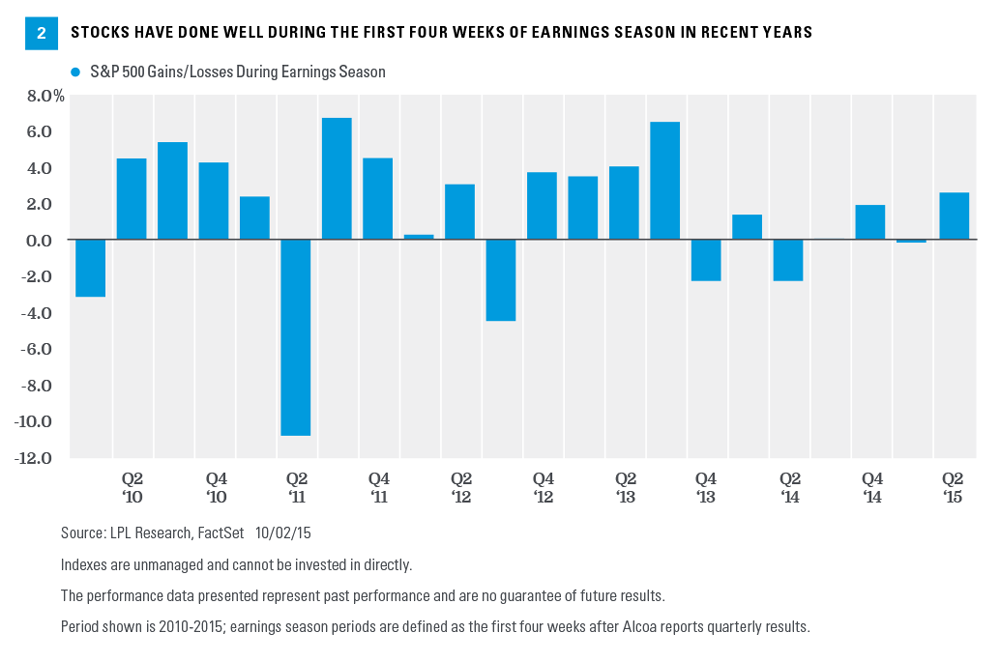

Regardless of stock performance ahead of earnings, the stock market has generally welcomed earnings reporting season. Since 2010, spanning 22 quarters, the S&P 500 is up an average of 1.5% during the four weeks after Alcoa’s results and has risen during 68% of those periods [Figure 2]. (Alcoa has historically marked the “unofficial” start of earnings season because it has been the first major company to report quarterly results.) We expect gains this reporting season even though this pattern has been mixed over the past year. Turning the market’s attention away from investors’ concerns about the Federal Reserve (Fed) and China is likely to be a good thing, especially if what we hear from companies about the Chinese demand environment is sanguine, as we heard from Nike on September 24, 2015, when reporting its results.

Another difference between this quarter’s earnings season and last is more evidence of slower growth in China. But given China represents an estimated less than 5% of S&P 500 profits, we do not expect much direct impact. China is responsible for a lot of the weakness in commodity sector earnings, though that is certainly not a new development.

OPPORTUNITIES

We believe these two sectors are well positioned for earnings season and may outperform over the next month or so:

· Healthcare. Healthcare was one of the worst performing sectors during the third quarter with a 10.7% loss. The primary reason for the weakness was concern about drug price controls after Democratic presidential candidate Hillary Clinton proposed a plan to rein in the high cost of drugs, especially those produced by biotech companies. We see little chance of any such plan being passed regardless of the outcome of the 2016 elections, and expect the now reasonably valued group to do well on what should be solid results.

· Consumer discretionary. The consumer discretionary sector was one of the top performing sectors during the third quarter and will likely produce solid third quarter results due to cheaper gas prices and low input cost inflation. In addition, with relatively less overseas exposure, this group is somewhat insulated from the slowdown in China.

We continue to favor the industrials and technology sectors, but slower growth overseas may negatively impact certain parts of these sectors. And given the 21% drop in oil prices during the third quarter, it is difficult to have much confidence that the energy sector will surprise positively.

2015 STOCK MARKET FORECAST

In November 2014, we forecast a total return for the S&P 500 in 2015 of 5 – 9%, a forecast we stood by in June 2015. Although we have not officially lowered our forecast (we typically only publish two forecasts each year), we acknowledge that following the latest stock market correction it is going to be difficult to reach the low end of that target. That forecast was predicated on high-single-digit earnings growth that will not likely materialize (again, energy and the dollar are the main culprits). S&P 500 earnings for 2015 will likely end up growing in the low-single digits, which has, in part, translated into lower stock prices.

However, we remain confident that stocks will rally over the rest of the year and stand a good chance of ending in positive territory, driven by easing China fears, increased comfort with the Fed’s go-slow approach to raising rates, a likely solid earnings ramp-up over the next several quarters, stability in the energy sector, and favorable seasonal patterns (the fourth quarter has seen a median S&P 500 gain of over 5% and has been positive 80% of the time since 1980). Reaching the low end of our target (3% price gain plus 2% from dividends) may not be probable at this point but is still possible.

CONCLUSION

Third quarter 2015 earnings season may look a lot like second quarter, with little, if any, earnings growth amid big headwinds from the energy sector and a strong U.S. dollar. But underneath those drags is some healthy earnings power that we believe will help propel stocks higher in the coming weeks. Looking forward, a potential acceleration in earnings growth over the next several quarters is one of several reasons we expect stocks to finish the year strongly.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

Because of its narrow focus, investing in a single sector, such as energy or manufacturing, will be subject to greater volatility than investing more broadly across many sectors and companies.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a nondiversified portfolio. Diversification does not ensure against market risk.

All investing involves risk including loss of principal.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.