Signs of Healing in the Markets Are Slowly Starting to Appear

Key Points

▪ Risk assets have started to show preliminary signs of stabilizing, but more healing needs to occur.

▪ Investors remain wary about global growth prospects; we expect gradual improvements.

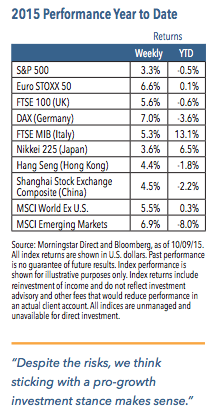

Signs of economic stabilization in China and improvements in commodity markets helped U.S. equities recover some ground last week. Diminishing concerns over the delay in Federal Reserve rate hikes also aided sentiment. For the week, the S&P 500 Index jumped 3.3%, with the energy, materials and industrials sectors leading the way.1 Health care, in contrast, struggled.1

Volatility Should Persist, Possibly Creating Opportunities

Over the past couple of weeks, markets have started to show some resiliency, with risk assets such as fixed income credit sectors, commodities and emerging markets showing gains.1 We remain of the opinion that equity markets must continue healing and expect volatility will persist, but we also think the recent sharp sell-off did not signal the start of a new bear market. Prices are likely to vacillate in the near term, so investors with longer time horizons may want to consider adding to equity positions during times of weakness. In particular, we are seeing opportunity in companies that have become relatively inexpensive but that have solid fundamentals.

Weekly Top Themes

1. Modest levels of jobs growth should promote consumer spending. The September jobs report showed employment has increased 2.0% year-over-year, while average hourly earnings have climbed 2.2%.2 With broad inflationary pressures still absent and unemployment down to 5.1%,2 we think these levels should be enough to drive personal income levels and spending higher.

2. The rise in the dollar and corresponding decrease in energy prices shouldn’t hurt the economy as much as many think. Since these trends became evident in the summer of 2014, three million jobs have been created in the service sector and 150,000 in the manufacturing sector.3 At the same time, the energy sector has lost 70,000 jobs.3 These numbers suggest that any economic problems have remained well contained.

3. We expect the U.S. economy to continue to accelerate modestly, but see possible drags. In particular, we think a correction in inventories and a drag from foreign trade will act as headwinds for third quarter growth.

4. Recent political issues in Washington could lead to economic issues. Last week’s news that Kevin McCarthy dropped out of the running to replace John Boehner as Speaker of the House raises the odds of brinkmanship, procrastination or gridlock over the debt ceiling issue.

5. It’s not a done deal yet, but the odds of passing the Trans-Pacific Partnership have grown. The agreement is one of the most significant trade deals in years. Some legislative language needs to be worked out, however, and it will probably take months before the deal is voted on in Congress.

The Outlook Is Still Murky, but Favors a Pro-Growth Stance

Equities are starting to show tentatively encouraging signs. In late September, equity markets experienced a renewed downturn, but did not pierce their August lows.1 Had they done so, that could have led to a further rout. Instead, however, prices moved modestly higher over the last week, even in the face of mixed economic data. We think this suggests selling pressures may be starting to fade. We are hardly out of the woods yet, and it is certainly possible we could see another retest of the recent lows. In the short term, we don’t anticipate any sustained advance in prices until we see equity prices break out of their recent trading ranges to the upside.

So what will it take for equities to be begin another rally? For one, we think investors will need to see continued evidence that global growth remains on track. More signs of stability from China would certainly help. We expect such evidence will materialize, but acknowledge that it will still take some time. Nevertheless, we think stronger growth will push both global equity prices and bond yields higher in the coming months. As such, we believe sticking with a pro-growth investment stance still makes sense. Traditional safe havens have become expensive in recent years while most risk assets, including equities, offer better value. We caution, however, that commodities (and commodity-based markets and regions) are likely to continue to struggle.

1 Source: Morningstar Direct and Bloomberg, as of 10/09/15

2 Source: Bureau of Labor Statistics

3 Source: Deutsche Bank Research

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

©2015 Nuveen Investments, Inc. All rights reserved.