Fall Quarterly Commentary

No man is an island, entire of itself;

Every man is a piece of the continent,

A part of the main.

If a clod be washed away by the sea,

Europe is the less.

As well as if a promontory were.

As well as if a manor of thy friend's

Or of thine own were;

Any man's death diminishes me,

Because I am involved in mankind,

And therefore never send to know for whom

The bell tolls; it tolls for thee.

John Donne, 1572 – 1631

English poet and cleric

Meditation XVII

Devotions upon Emergent Occasions

John Donne wrote these words during a bout of deathly sickness in the 17th century. In the original full version (which is prose, not poetry), he first asks if the bell is tolling for himself or for another, then in the above passage he suggests that it matters less for whom the bell specifically tolls, and then finally he concludes that death can actually have value but only if someone, by understanding it properly, makes good use of it to bring himself closer to God. While even then it may have been true that no man is an island, we find today’s world more interconnected than ever. This interconnectedness goes a long way in understanding the recent selloff in global equity and credit markets.

The third quarter produced the worst return for the S&P 500 Index in four years, wiping out the prior year’s gains. Peak to trough declines from 2014-15 index highs to recent lows were even greater. Shown below, many diverse groups of stocks dropped more than the S&P 500 Index:

• Dow Jones Industrials: -14.4%

• Dow Jones Transports: -19.0%

• Dow Jones Utilities: -16.9%

• S&P 500 Index: -12.4%

• NASDAQ: -13.6%

• Russell 2000 (small cap): -16.4%

• MSCI EAFE (international): -19.3%

• MSCI Emerging Markets: -29.9%

A plethora of stocks hit 52-week lows during August and September, with only three stocks on the NYSE at new 52-week highs versus 507 at new lows on the final trading day of the quarter. The following two market statistics are daunting, as they have typically signaled a “bear market”, i.e. an ultimate market decline of more than 20%:

• The S&P 500 Index dropped more than 10% below its 50-day moving average on August 25th

• 44% of the stocks on the NYSE reached new 52-week lows in the week ending August 28th

The initial triggers for the aforementioned market declines were weak Chinese growth and a surprise August “devaluation”1 of the yuan, which spooked global markets. While we don’t intend to reprise the entire bearish China argument from our previous letters, we reiterate that we believe the situation is “worse than you think2 ”.

The bear case on China is that it has had a huge building boom, and building booms are often followed by busts, as we recently learned in our country. In fact, let’s compare the two. At its peak before the U.S. housing crisis, six percent of GDP was involved in homebuilding (about double or triple the U.S. average). Afterwards, a large overhang of unemployed construction workers dragged on the U.S. economy, as many of these builders who previously held good construction jobs were unable to find work. China, in comparison, has fully 12% of its economy involved in residential construction (officially). And no, China is not starting from a lower base. The country already boasts the second highest residential space per capita in the world, behind only the U.S. Thus, the Chinese are clearly running out of opportunities to continue to build apartments and home... while still having the new construction be useful/desired. This is the predicament put in real terms, rather than financial terms. No matter what kind of monetary easing or other lever-pulling Chinese authorities engage in, we find it very hard to believe that they will take 110 million3 construction workers and get them engaged in another occupation without missing a beat.

There exists a long history of countries finishing giant construction projects just before or after their economic comeuppance. This can be observed anecdotally by tracking construction of the world’s tallest buildings: the Burj Khalifa opened in 2010 during Dubai’s debt bust, both the Empire State and Chrysler Buildings were conceived before the 1929 U.S. crash, and Malaysia’s Petronas Towers opened in 1998, just as the Asian Financial Crisis was gaining steam, to name only a few. While China isn’t currently building the world’s future tallest building (that dubious honor goes to Azerbaijan), a quick look at a list of the world’s tallest buildings (including those currently being planned or constructed) reveals that a full 28 of 50 are in China, 20 of which are still under construction... with the majority scheduled to be finished during 2017-2018. This timeline is compatible with a paper just released from the Bank for International Settlements, “the central bank to the world’s central bankers” and a very sober source. The paper notes that China, by one measure4 , has a two-thirds chance of experiencing “serious banking strains” within three years.

China’s historic building boom has required raw commodities from all over the world, and now that further increases in demand look unlikely, the currencies of some of those countries that supplied the raw materials (along with the materials themselves) are being crushed. To recount but a few of the casualties this quarter, the Brazilian real fell 22%, the South African rand 12%, and the Malaysian ringgit 14%. Clearly the economic disturbance is now more than just a “China problem”.

These moves also put China’s three percent “devaluation” in context as pretty small... so far that is. Further yuan “devaluations” may be coming, as preventing them has become very expensive. For years, China bought billions of U.S. dollars with yuan in order to keep its currency down (some called this “manipulation”). Now, however, the story has changed and China is spending billions of those U.S. dollars5 to prop the yuan up as its economy falters and rich Chinese try to get their money out of the country.

The emerging market countries mentioned are all going to have recessions, particularly Brazil, which, in possessing oil reserves that are particularly expensive to develop, is also being hit by low oil prices. John Donne’s meditation intones “no man is an island”. Well, in today’s economy, “no country is an island”, especially not many of those physically surrounded by water such as Indonesia and Australia (both major commodity exporters suffering nine percent currency declines during the third quarter). Currently, opinion is divided as to whether the U.S. is indeed an “island” able to remain totally unaffected by the slowdown abroad. We are skeptical.

Weakness in emerging market currencies has significant implications for many of the corporations and economies of those countries. Witness the tenfold increase in U.S. dollar denominated corporate bonds outstanding, reflected in the chart at left. It becomes more difficult for foreign companies to pay off U.S. dollar debt when their own currencies decline.

The “islanders” crowd (those who believe the U.S. will be unaffected) is quick to point out that a similar currency crisis didn’t derail the U.S. economy too much during the 1998 Asian Currency Crisis. While the U.S. stock market did contract some 15%, it was quickly made up (...or perhaps it was only “covered up” in the indexes by the high-flying dot-com stocks of the era, which in retrospect were clearly disconnected from economic reality). Perhaps the U.S. will avoid major economic pain, and there are indeed reasons to be positive (more on that in a minute), but we would point out that today’s global economy is even more integrated and emerging markets make up a much greater proportion of it than was the case in 19986 (as reflected by the chart at the bottom of the prior page).

At the very least the stronger U.S. dollar will make it harder to sell American goods abroad and it will lower the dollar value of all overseas corporate earnings... putting overall U.S. corporate earnings at risk. Already, declines in U.S. corporate profits in both the second and third quarters represent the first successive drops since 2009.

U.S. corporate profit margins have contracted from highly elevated levels. This is a concern for two reasons: 1) margins would have to fall far in order to reach historic norms and 2) recessions (periods shown in grey on the chart at right) frequently followed similar declines in margins. Six years into a recovery, it is not hard to imagine a foreign-born recession washing ashore.

The bond market too is issuing warning signals. High yield credit spreads (the extra yield that owners of junk bonds require relative to Treasury yields) are at three-year highs. While many excuse this deterioration as isolated to energy and commodity issuers, we pay attention because credit spreads tend to lead equity markets. Junk bond spreads, which widen on concerns future interest and principal payments will be made, are a good barometer of economic conditions. A very strong U.S. economy is looking less and less likely, with continued slow growth or even a mild recession appearing the more probable alternate scenarios.

Thus we have laid out the bear case for the economy... but what does this mean for stocks? The risks from China for the global economy were always there... but only now are really starting to be taken seriously and recognized by the markets. This “recognition” created the recent price declines and actually lowered risk and now presents buying opportunities, as some previously prohibitively expensive stocks begin to look attractive for the long run... even if there are further drops in the immediate future. We will likely purchase another stock soon, and we have further dry powder in the form of cash beyond that if the market drops further.

Despite the possibility of a U.S. recession, there are economic reasons to believe that, even if a recession materializes, it wouldn’t be “that bad”. The first is that the U.S. financial system is in pretty good shape, with stronger regulation and natural post-crisis deleveraging having resulted in a much safer system. In addition, there is reason to believe that the U.S. consumer, which so many times has been the savior of world growth, might again come to the rescue. Low gasoline prices, low commodity prices, reasonably strong employment, and a strong dollar all make it easier and cheaper for the typical American to spend... and we believe spend they will. These are both strong arguments against going into full panic mode.

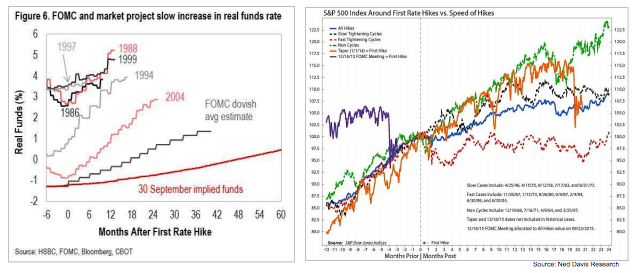

Indeed, the economic weakness itself argues for low inflation, and low inflation argues for low interest rates7 . The Fed has come out and said they expect to raise rates in 2015... but having heard this same message for years, we are skeptical, and so is the market. Above left, you can see the market’s expectations (the “implied funds” red line) are that hikes will be lower and slower than the Fed itself predicts (“FOMC line”). It’s also worth noting that even the Fed’s prediction is for a much more gradual pace than seen during past hikes... all rate hikes are not created equal. As the chart above right shows, slow rate hike cycles usually accompany rising stock markets.

An indication that the markets may soon turn upward is sentiment. A recent survey of financial advisors by Investors Intelligence registered only 25% of respondents “bullish”, a low not seen since the 22% reading following the collapse of Lehman Brothers in 2008. Meanwhile, stocks continue to be priced attractively relative to bonds, with the 2.2% dividend yield of the S&P 500 Index exceeding the 2% interest available in 10-year Treasuries.

There is another conceptual reason to be bullish, both on stocks and life: the march of human progress. Recession or no, the march goes on and we believe it is probably accelerating. The U.S. and world writ large continue to make impressive advances in manufacturing (3D printing), electronics (wearables), transportation (electric cars), artificial intelligence (Siri), medicine (everything), and resource extraction (horizontal drilling). Technology and progress is all about doing new things, and doing more with less. The graphic to the left is one of our favorite ways to express how technology allows us to do more with less: all your old items (to the right) are now in your iPhone (to the left).

We want to illustrate a few things about technological progress and in order to do so will ask you to consider a single example in the form of a smartphone application: Google Translate. Download it for free and try it for yourself if you haven’t. Among other things, you can use your phone’s camera to point at any text (a book, a sign, a menu) and it will translate that text on your screen... instantly and in real time! And it’s free. Equipped with this new capability, there is no need to purchase translation phrasebooks or hire translators to eliminate foreign language confusion. You (if you are a smartphone owner) now have something that you didn’t before, and you didn’t have to pay for it; in a very real sense, you are now richer.

We often talk about economic activity in terms of GDP – Gross Domestic Product. This figure attempts to measure economic activity, but it does so by measuring the price of things that are bought and sold. No matter what value Google Translate has for you, whether small or large, it will not directly increase GDP one bit, because it is given away for free. Google Translate is only one small example, but many of today’s advances are delivered very cheaply or for free, and hence are only partially or not at all included in official statistics.

Actually, this idea that through technology we are doing more with less, and that it is not properly measured, can help explain some of the economic data we’ve been seeing:

• Low Economic Growth. What does Google Translate add to GDP? Nothing! Actually it has a negative impact because now there will be fewer sales of translation phrase books (etc.), sales that previously were counted in GDP.

• Low Productivity Growth. This is perhaps the most surprising of all... shouldn’t technology make us more productive? Again it is measurement. Official “productivity” is GDP / hours worked. If your productivity isn’t measured in a commercial transaction, it won’t be in GDP and won’t be in official “productivity”.

• Low Inflation. The last few years have seen low, below target inflation despite extraordinary money printing. The money printing has been at least partially offset by what progress naturally does: make things cheaper. When things cost less inflation goes down. What is recent inflation in translation services? If you are now using Google Translate instead of hiring a translator, the inflation in translation services is negative 100%. Official statistics attempt to make adjustments for this effect but they are probably inadequate.

Other aspects, while not due to mismeasurement, can also be at least partially (and only partially because these are complex phenomena) explained by the nature of increasing technological advancement.

• Rising Inequality. Progress is doing more with less, and “less” can mean “fewer people” too. As fewer people can do the same work, the unnecessary workers are laid off. This leaves a smaller group of people to capture the industry’s benefits. Benefits that were distributed become concentrated. All else equal, faster progress can often mean more inequality.

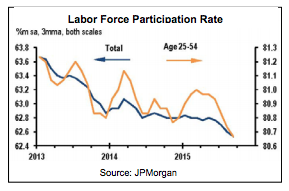

• Lower Labor Force Participation. By the same mechanism as explained above, technological advancement can throw people out of work. Finding a new job is not always easy, and many become discouraged or accept only part time work.

Despite the real and painful problems of technological advancement (which are not to be summarily dismissed), progress is ultimately beneficial not only in terms of unmeasured free products available to consumers, but also to GDP and hence stocks in general. Put in terms of our example, most unemployed former foreign language translators and phrase book printers eventually do find new jobs (which will be measured in GDP), and all of society benefits.

In short, we’re bullish on humanity and human progress. We’re bullish on America where much of this innovation takes place. Long term, we’re even bullish on China, which we believe will go on to advance and do great things after the painful, but ultimately temporary, potential economic stumble we’ve described.

Thus, despite the recent negative gyrations of the market, which we too have felt as we invest our own money alongside yours, we remain confident that the ultimate direction of progress is up, and by being invested in stocks we all will participate.

Very Truly Yours,

John G. Prichard , CFA

Miles E. Yourman, CFA

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

1 We use quotes here because the devaluation was only about 3%, which is so small that it hardly deserves to be considered a proper devaluation at all.

2 This phrase has been used by Jim Chanos, whose views on China have heavily informed our own. Mr. Chanos is a noted short seller, whose greatest fame came from being one of the first people to predict the downfall of Enron. So when he says something is that everyone thinks is a great success is in fact broken, one should take note.

3 920 million working age population * 12% = 110 million.

4 The measure is the ratio of private sector credit to gross domestic product, which is 25% in China, the highest among emerging markets by a wide margin.

5 China spent $43 billion in September for a total of $180 billion in the third quarter. They do have $3.5 trillion left in reserves so they can keep this up for a long while, but it is an expensive prospect.

6 Note that at first glance the chart seems to indicate that emerging market economies are now bigger than developed markets, but actually the two lines are using different scales (emerging markets on the right and developed on the left). Even though in this case not intentional, it is surprisingly easy to mislead using graphs, even with accurate data. Always look at the scale.

7 The comment around here, only a half-joke, is that “rates are never going up, ever.”

© Knightsbridge Asset Management, LLC