KEY TAKEAWAYS

- This week we highlight seven key charts to watch that may determine the stock market’s near-term direction.

- The charts cover a wide range of topics including manufacturing sentiment, earnings, oil, and high-yield bonds.

- We believe these charts can help investors navigate the market’s course for the balance of 2015 and into 2016.

This week we highlight seven key charts to watch that may determine the stock market’s near-term direction. We believe these charts, covering a wide range of topics, including manufacturing sentiment, earnings, oil, and high-yield bonds, collectively can help investors navigate the market’s course for the balance of 2015 and into 2016.

KEY CHARTS TO WATCH

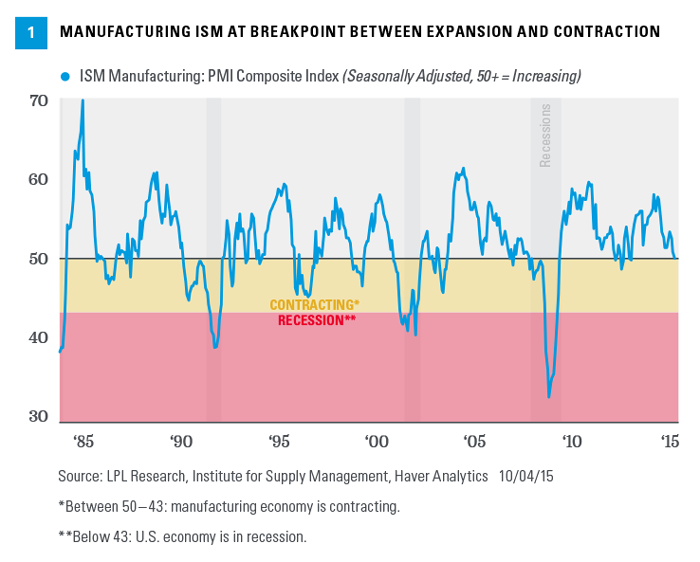

ISM Manufacturing Index. The Institute for Supply Management (ISM) Manufacturing Purchasing Managers’ Index (PMI) is one of our favorite leading indicators [Figure 1]. We have found it to be a good leading indicator of earnings growth. Due to the fact that as much as two-thirds of the S&P 500 is manufacturing based, a survey that measures optimism (or pessimism) of purchasing managers is much more reflective of the corporate earnings-driven stock market than the U.S. economy as measured by gross domestic product (GDP), of which manufacturing only makes up less than one-third of the total.

The most recent reading on the manufacturing ISM for September, released on October 1, 2015, came in at 50.2, the lowest reading since May 2013 and teetering on the edge of contraction. Importantly, a dip in the manufacturing ISM to below 50 has not been a signal that the broader economy is headed for recession (historically a low 40s reading means recession). The manufacturing ISM has averaged 52.2 over the first nine months of 2015, a level that the Institute for Supply Management notes has corresponded to growth in real GDP of 2.9%, just a shade below our long-held forecast of 3.0%+ for 2015.*

*As noted in the Outlook 2015, LPL Financial Research expects GDP to expand at a rate of 3% or higher, which matches the average growth rate of the past 50 years. This is based on contributions from consumer spending, business capital spending, and housing, which are poised to advance at historically average or better growth rates in 2015. Net exports and the government sector should trail behind.

Also worth noting is the manufacturing ISM has dipped to 50 (or below) in each of the last three expansions without a recession actually occurring. Oil and the strong dollar have been a drag on manufacturer sentiment, as they have been on earnings. For more on the ISM, please see the recent Weekly Economic Commentary, “ISM Indicates Fairly Robust Economic Activity Continues.”

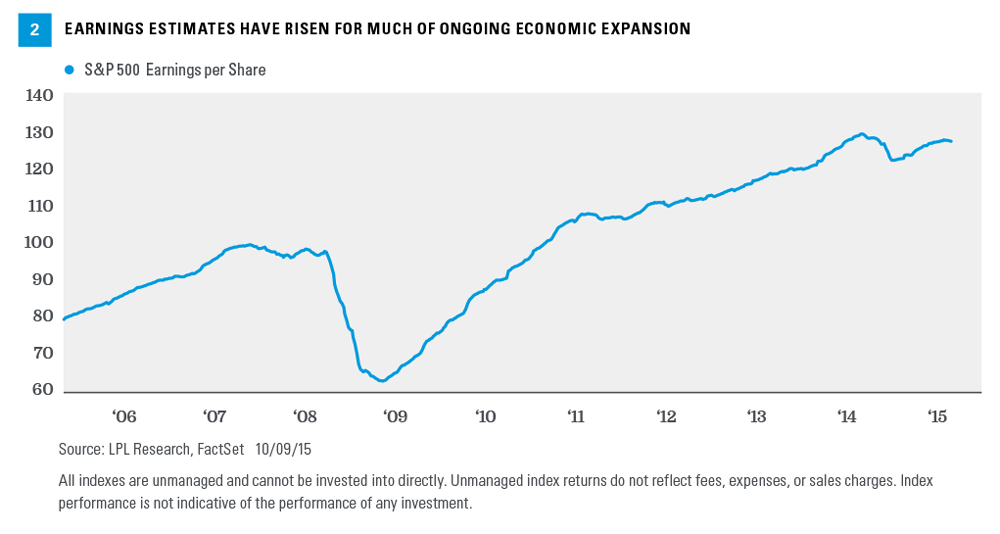

Earnings revisions. Earnings season unofficially kicked off last week (October 5 – 9) with Alcoa’s results, and this week 36 S&P 500 companies report (see our third quarter 2015 earnings preview). We are firm believers that earnings drive stock prices, so changes in earnings expectations are a favorite data point. The analyst community generally does a good job estimating the previous quarter’s results, which are “old news” by the time they are reported and typically have less impact on stock prices. But what company results and management comments mean for future earnings can drive big moves in stocks, and is where we focus most of our attention.

Consensus estimates over the next 12 months for the S&P 500 are about $127 per share [Figure 2]. Historically, analysts’ estimates have started the year too high and actual results have ended up about 3% lower than initial forecasts on average. Accordingly, if next year’s estimates hold steady or even fall slightly during this earnings season, we would view that as encouraging. We expect earnings growth to potentially accelerate next year as the drags from the energy sector and U.S. dollar begin to abate.

VIX measure of implied stock market volatility. The CBOE VIX Volatility Index is a market-based measure of the implied volatility of the S&P 500. Often referred to as a fear gauge, a higher reading indicates a fearful market where market participants are demanding insurance. A lower reading suggests market participants are less nervous and are generally not demanding protection from potential market losses. After spiking to as high as 40 on August 24, 2015, due to heightened uncertainty around the Federal Reserve (Fed), China, and the energy sector, the VIX has dropped nine consecutive days to about 17 [Figure 3], below its long-term average near 20 but well above the 2015 lows near 12.

The VIX is important as a measure of sentiment. At this stage of the business cycle when earnings growth is relatively modest, stocks need increases in what the market is willing to pay for those earnings (expansion in the price-to-earnings [PE] multiple) to move meaningfully higher. The latest stock market correction was driven more by souring sentiment and falling PE multiples, rather than deterioration in fundamentals of the U.S. economy or corporate America. Better sentiment, or less fear, will be required to get stocks back to positive territory for the year.

The Fed’s timetable. The beginning of a rising interest rate cycle is an important consideration for stock market investors because of the impact on market interest rates. The market’s expectations for the timetable of Fed rate hikes have shifted out quite a bit in a short amount of time, following dovish commentary from the Fed and the weak jobs report released on October 2, 2015 [Figure 4].

While the timing of the first rate hike is important, the pace of subsequent hikes is likely more so. The Fed has told us it expects hikes to be gradual once they begin and that it is unlikely to take rates as high as in previous cycles. This suggests the economic cycle may still have a ways to go, given initial Fed rates hikes during previous cycles have occurred approximately four years before the next recession, on average. That may mean good things for stocks over the next couple of years.

High-yield bond spreads. High-yield bond spreads (yield on the Barclays Corporate High Yield Bond Index relative to U.S. Treasuries) measure risk aversion in the markets (similar to the VIX). These spreads are especially important now because of close ties to the energy sector, which represents about 15% of the Barclays High Yield Bond Index. High-yield bond spreads have widened in recent months on heightened fears of defaults in the oil patch [Figure 5]. Narrowing credit spreads would potentially be indicative of improving financial health of the energy sector, which may be accompanied by healthier overall U.S. corporate profits and stronger bank balance sheets.

Credit markets have tended to factor in perceived deterioration in the economy or sectors ahead of the equity markets, making them a good leading indicator in certain circumstances. A recent example is the sell-off in high-yield bonds this summer, which preceded the stock market sell-off in July 2015.

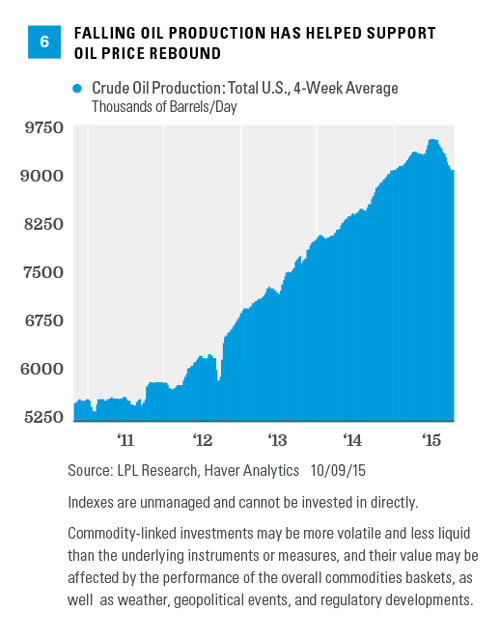

U.S. oil production. Oil has a supply problem, not a demand problem, and the way to fix a supply problem is with lower prices, which are then met with less supply. The sharp drop in oil prices since late 2014 has been met with a drop in U.S. oil production [Figure 6]. But with oil still below $50 (based on West Texas Intermediate), a level that is unprofitable for many domestic producers, more supply reductions are necessary. This year, the four-week average U.S. production has dropped from 9.6 million barrels per day to just above 9.0 million barrels per day, and is likely to fall further as capital spending reductions continue to flow through.

We noted the importance of oil with respect to high-yield bonds, but oil is also connected to other segments of the market. The energy sector represents just 8% of the market cap of the S&P 500, but about 25% of its capital spending. The commodity is also tied to China, the world’s second biggest oil consumer (after the United States) and one of the market’s primary concerns right now. We continue to see oil’s fair value closer to $60 than $50, but this assumes further production cuts and the current, if not higher level of demand. Both assumptions are very reasonable, but neither is certain.

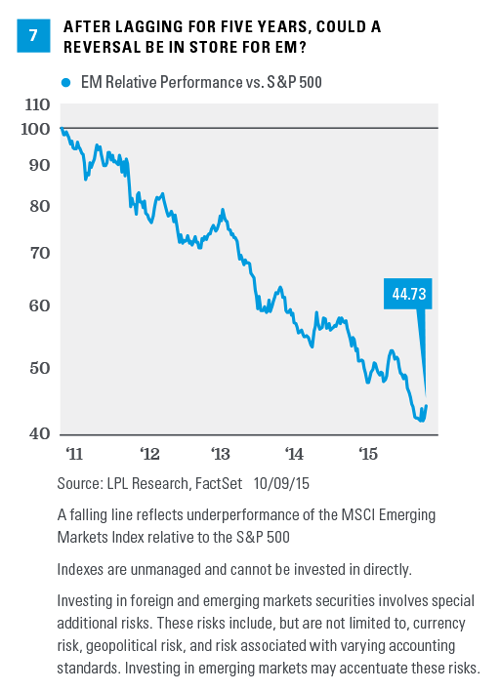

EM relative strength. Our last key chart to watch, relative strength of emerging markets (EM), is important because, after five years of underperformance, EM equities performance is beginning to turn [Figure 7] even as the slowdown in the Chinese economy has been such a big concern for the markets. EM performance is also important because of its links to commodities and investors’ risk tolerance. We are watching this one particularly closely because we maintain an EM allocation in the majority of our model portfolios.

CONCLUSION

We believe these charts will go a long way toward determining the near-term direction of the stock market. We will continue to follow these and other key data points as we chart the market’s course for the remainder of 2015 and formulate our market forecasts for 2016. n

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

Because of its narrow focus, investing in a single sector, such as energy or manufacturing, will be subject to greater volatility than investing more broadly across many sectors and companies.

Bond and bond mutual fund values and yields will decline as interest rates rise and bonds are subject to availability and change in price.

Government bonds and Treasury bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

DEFINITIONS

The VIX is a measure of the volatility implied in the prices of options contracts for the S&P 500. It is a market-based estimate of future volatility. When sentiment reaches one extreme or the other, the market typically reverses course. While this is not necessarily predictive it does measure the current degree of fear present in the stock market.

Purchasing Managers’ Indexes (PMI) are economic indicators derived from monthly surveys of private sector companies, and are intended to show the economic health of the manufacturing sector. A PMI of more than 50 indicates expansion in the manufacturing sector, a reading below 50 indicates contraction, and a reading of 50 indicates no change. The two principal producers of PMIs are Markit Group, which conducts PMIs for over 30 countries worldwide, and the Institute for Supply Management (ISM), which conducts PMIs for the U.S.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

The credit spread is the yield the corporate bonds less the yield on comparable maturity Treasury debt. This is a market-based estimate of the amount of fear in the bond market B-rated bonds are the lowest quality bonds that are considered investment-grade, rather than high-yield. They best reflect the stresses across the quality spectrum.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Institute for Supply Management (ISM) Index is based on surveys of more than 300 manufacturing firms by the Institute of Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders, and supplier deliveries. A composite diffusion index is created that monitors conditions in national manufacturing based on the data from these surveys.

The Barclays High Yield Bond Index covers the universe of publicly issued debt obligations rated below investment grade. Bonds must be rated below investment grade or high yield (Ba1/BB+ or lower), by at least two of the following ratings agencies: Moody’s, S&P, and Fitch. Bonds must also have at least one year to maturity, have at least $150 million in par value outstanding, and must be U.S. dollar denominated and nonconvertible. Bonds issued by countries designated as emerging markets are excluded.

The Barclays U.S. Corporate High Yield Index measures the market of USD-denominated, noninvestment-grade, fixed-rate, taxable corporate bonds. Securities are classified as high yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below, excluding emerging markets debt.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit

RES 5245 1015 | Tracking #1-429342 (Exp. 10/16)

(c) LPL Financial