The Rally Continues, but Equities Appear Stuck in a Trading Range

Key Points

▪ Equities have enjoyed a rally in recent weeks, but we doubt the technical conditions are in place for a sustained advance.

▪ For now, markets appear stuck in a trading range until we see more clarity from economic growth and corporate earnings.

▪ We expect positive signals will emerge over time, leading us to favor a pro-risk stance.

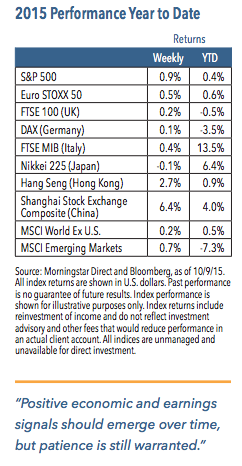

Equity markets continued to advance last week, with the S&P 500 Index climbing 0.9%.1 Third quarter earnings results were mixed, and investors focused on stabilization in China and the upside of the Federal Reserve holding rates steady. The utilities sector was the best-performing, while industrials lagged.1

A Continued Climb in Equities Will Require Earnings Clarity

Equity markets have enjoyed a strong comeback over the past couple of weeks, with the areas of the U.S. market that were hardest hit during the August/September sell-offs climbing the most.1 Given the prospects of a more benign Fed, the U.S. dollar has weakened a bit, which has helped emerging markets.1 Whether this rally can be sustained will largely depend on the prospects for corporate earnings and profits. Unfortunately, we think it will take some time to see such clarity.

Weekly Top Themes

1. We forecast third quarter U.S. economic growth will be between 2% and 2.5%.

Continued strong consumer spending should push the economy forward, while inventory and trade will likely be drags.

2. Over the next year, we expect a modest rise in inflation due to a stronger economy and tighter labor market. Headline CPI inflation fell 0.2% in September (in line with expectations), but core CPI rose 0.2%.2 Year-over-year, core CPI rose 1.9%, its highest level since July 2014.2

3. Investor sentiment may have improved recently, but frustration remains high. Specifically, investors appear uneasy after the recent sharp sell-off that drove the S&P 500 down 12% over nine trading days in August, with some areas of the market (such as biotech) falling even more.1 The sharp back-and-forth since that time has also contributed to unease.

4. Despite recent strength, we believe U.S. stocks remain in a trading range. Prices have tested upward resistance levels, but we don’t think there is enough technical strength to support a breakout. We believe the S&P 500 is in a trading range of between 1,867 (the August low) and an upper level of 2,050 to 2,100.3

5. During the rally, we have seen a notable change in market leadership. Through the end of September, momentum stocks led the way, but that trend has reversed in recent weeks.1 Furthermore, we are starting to see a shift from growth to value, with some areas of energy and materials assuming leadership. Retail sectors, health care, equipment and services are all lagging on a relative basis.1

Economic Stability Should Eventually Support Risk Assets

Since the Great Recession, the U.S. economy hasn’t been firing on all cylinders and has periodically slowed. Yet, the labor market has been relatively strong and while retail sales have been uneven, consumer spending levels have advanced at a respectable pace. Manufacturing activity has been lagging, which is worrisome, but a drop in manufacturing shouldn’t lead to broader problems. Furthermore, we anticipate manufacturing will pick up over time as spending levels continue to rise and the negative effects from the stronger dollar/lower oil trends fade.

Despite some issues, the U.S. economy still appears in better shape than most other regions. We are seeing similar directional signals from Europe, where nonmanufacturing activity is stronger than the manufacturing sector. Overall, developed markets have been experiencing choppy growth and many emerging economies are faltering after booming over the past decade. In particular, resource-related economies and regions are struggling noticeably.

Given this challenging economic environment, we think corporate earnings have held up reasonably well in recent years, which allowed equity markets to advance strongly up to 2015. The Fed remaining highly accommodative has helped as well. Risk assets (such as equities and high yield corporate bonds) have struggled in recent months, but we believe they should eventually return to favor as global economic conditions slowly improve. The keys to this outlook are continuing growth in the United States and Europe, stability in China and some calming in the commodity markets. We expect all three will occur over the coming year. Given these expectations, and our view that safe-haven assets such as government bonds look unattractive, we favor a pro-risk investment stance.

1 Source: Morningstar Direct, Bloomberg and FactSet as of 10/9/15

2 Source: Bureau of Labor Statistics

3 The S&P 500 Index closed at 2,033 on 10/9/15 (FactSet).

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

©2015 Nuveen Investments, Inc. All rights reserved.