Liquidity Premiums In High Yield Investing

There is no denying that liquidity has become a well-publicized concern in today’s high yield market, with much focus specifically on high yield ETFs. With the post financial crisis regulation that has curtailed market making activity by the large investment banks and dealer inventory, liquidity has decreased and volatility increased. However, we believe that arguments that liquidity concerns within the ETF space will lead to the high yield market’s demise are overblown.

As we have noted in past writings (see “High Yield ETFs: Market Size, Money Flows and Liquidity”), ETFs represent a small portion of the total high yield market. ETFs alone account for about 12% of “retail” high yield fund-based assets, which includes the much larger mutual fund counterpart, and ETFs alone account for about 3% of the broader high yield market.1 And even with all the volatility we have seen this year, the largest weekly reported mutual and exchange traded fund flow was an outflow of about $3 billion (with most weekly fund flows under $1 billion)—this pales in comparison to the total $1.8 trillion market.2 So it seems misguided to us to say that activity in such a small piece of the total market will lead to collapse.

Pre and post financial crisis, we have always seen periods of volatility when market sentiment shifts. During times of fundamental or economic fear or a “risk off” trading environment, it is natural for prices to move down, and in some cases swiftly. Then again, we can also see swift moves up/recovery as market sentiment improves—markets tend to be manic. Periods of strained liquidity are something we have always had to deal with as high yield investors, and even if we are seeing that acerbated by recent regulations, we believe it is still manageable, and actually an opportunity for active investors to acquire assets on the cheap.

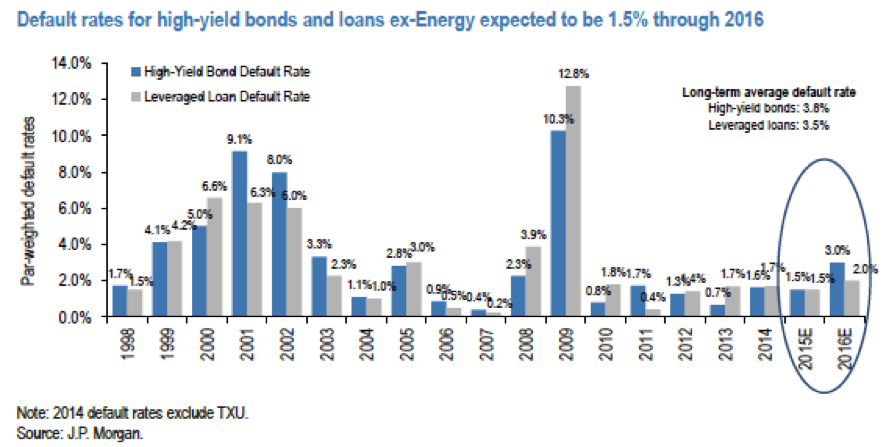

Our primary concern in high yield investing is defaults. We currently aren’t and don’t expect to see a big spike in defaults, outside of specific issues in certain energy and commodity sectors. We aren’t seeing issues with overleverage or bad market behavior in terms of use of proceeds, and while we are in a slow growth environment, outside of oil and commodities, we don’t see a huge shift in the underlying fundamentals of much of the high yield issuers. The high yield market tends to be more domestic focused, less reliant on international sales and less exposed to the dollar strengthening than the big multinationals pervasive in the equity indexes. And with the recent wave of refinancings, we generally see good liquidity at the corporate level and manageable capital structures. For all of these reasons, we do not see a huge default cycle outside of energy and commodities on the horizon.3

Yet we are still getting what we believe to be very attractive yields in many of these non-commodity names. Given these liquidity concerns, high yield bond investors today are capturing liquidity premiums, which is a risk for investors but it is not a fundamental risk and we believe we are getting well overpaid for this risk right now, making it a great time to selectively purchase credit. High yield bond spreads over comparable maturity Treasuries recently hit three year highs, providing high, tangible yield to investors as well as capital gain opportunities as much of the market is trading at a discount to par. You want to capture fear and liquidity, and not fundamental and default driven spread widening, and we believe that is what we are seeing in today’s high yield market, providing the best entry point that we have seen in years.

1 Acciavatti, Peter Tony Linares, Nelson Jantzen, CFA, Rahul Sharma, and Chuanxin Li. “2014 High-Yield Annual Review,” J.P. Morgan North American High Yield Research, July 31, 2015, p. 136.

2 Source for total high yield market size: Acciavatti, Peter Tony Linares, Nelson Jantzen, CFA, Rahul Sharma, and Chuanxin Li. “Credit Strategy Weekly Update,” J.P. Morgan North American High Yield Research, October 2, 2015, p. 38. Weekly fund flow totals sourced from S&P Capital IQ.

3 Acciavatti, Peter Tony Linares, Nelson R. Jantzen, CFA, Rahul Sharma, and Chuanxin Li. “Credit Strategy Weekly Update,” J.P. Morgan North American High Yield Research, April 10, 2015, p. 4-5.

Although information and analysis contained herein has been obtained from sources Peritus I Asset Management, LLC believes to be reliable, its accuracy and completeness cannot be guaranteed. Information on this website is for informational purposes only. As with all investments, investing in high yield corporate bonds and loans and other fixed income, equity, and fund securities involves various risk and uncertainties, as well as the potential for loss. Past performance is not an indication or guarantee of future results.