Conditions Remain Uneven, but Equities Again Charge Higher

Key Points

▪ The equity rally continued, with markets erasing the damage that was done in the August meltdown.

▪ Global economic conditions are mixed, but we think U.S. growth will continue to trend higher in the coming quarters.

▪ Equities may be at the high end of their current trading range, suggesting markets may need to take a breather at some point.

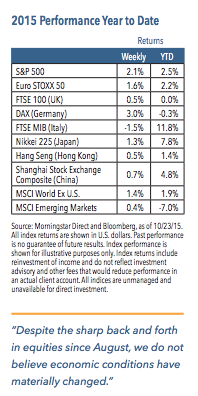

Equity markets climbed for the third consecutive week, with the S&P 500 Index gaining 2.1%.1 Much of the strength came from additional signs of easing from the European and Chinese central banks. Corporate earnings were mixed, with some health care and retail industries coming under pressure, while the technology sector provided impressive results. Overall, however, the majority of companies reported better-than-expected earnings results, which added to improved market sentiment.

Weekly Top Themes

1. The U.S. consumer remains relatively strong, and should be an important driver of economic growth. We expect retail sales will have increased by 4% or more in the third quarter, with strength coming from auto and restaurant sales, building and materials, and e-commerce. The combination of labor market gains and stronger real personal and family incomes should continue to support the U.S. consumer in the coming quarters.

2. The economy may have slowed in the third quarter but should rebound. In addition to consumer spending, we think residential investment and capital expenditures will have contributed to growth. On the other hand, trade may subtract 0.5% from growth and inventories may cause a 1.0% drag. Overall, we expect third quarter growth probably slowed to the 1.5% to 2.0% level. Looking ahead, we think fourth quarter growth may rebound and approach 3.0%.

3. The European Central Bank may engage in additional easing measures. The ECB adopted an extremely dovish tone at its policy meeting last week, which provided a strong tailwind for risk assets. The central bank indicated that it saw downside risks to economic growth and inflation, and suggested it may expand its quantitative easing program in December.

4. China engaged in yet another interest rate cut in an attempt to stimulate growth. The People’s Bank of China announced a 25 basis point cut in the one-year lending and deposit rates, the sixth such cut since last November.

5. Corporate earnings are beating expectations but may post another quarterly decline. One-third of S&P 500 companies have reported third quarter results, with 77% beating estimates by an average of 5%.2 However, earnings are on track to post their first back-to-back declining quarters since 2009.2 Reported earnings may be down around 2% to 3%, but would be up 4% to 5% excluding energy.2

What’s Behind the Recent Rally? Can it Continue?

The S&P 500 Index has now recovered all of the ground it lost since the midAugust crash.1 The market recovery is somewhat surprising since the overall economic backdrop has not really changed over the past few months. Concerns remain over Chinese growth and falling commodity prices (which helped precipitate the rout). More broadly, trends in global economic conditions remain relatively static. The developed world looks to be improving, especially in the United States and Europe where consumer spending levels are rising. Emerging markets growth looks more mixed. China’s economy is clearly slowing, and we think it is decelerating to approximately 5%. This would be a negative for commodity exporting emerging economies but a positive for those that import commodities.

So what has been driving the equity rally of recent weeks? We would point to some signs of stabilization and additional policy action in China, possible easing in other regions, the delay in rate increases from the Federal Reserve, a lack of negative noise from Washington, healthy bank credit levels, a resumption of merger-andacquisition activity and positive surprises from corporate earnings.

Looking ahead, we expect volatility will persist. Investors remain confused and uneasy and feel highly skeptical about the prospects for healing in the global economy. As the sharp summer downturn and subsequent recovery show, financial markets are capable of moving sharply due to changes in sentiment while ignoring actual fundamentals. We have argued previously that the S&P 500 was in a trading range of between a low of 1,867 and a high of around 2,050 to 2,100. The fact that we are at the upper end of that range does not change our view (the index closed at 2,075 on Friday).1 In other words, while we have an optimistic long-term view toward equities, we do not think the recent straight upward trend can continue without markets taking a breather at some point.

For more information or to subscribe, please visit nuveen.com/weekly-commentary.

1 Source: Morningstar Direct, as of 10/23/15

2 Source: FactSet

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

©2015 Nuveen Investments, Inc. All rights reserved.