Seeing the Forest for the Trees: The Role of Investment Yield in a Portfolio

Chasing Investment Yield or Total Return – Which is More Prudent in a Low Yield World?

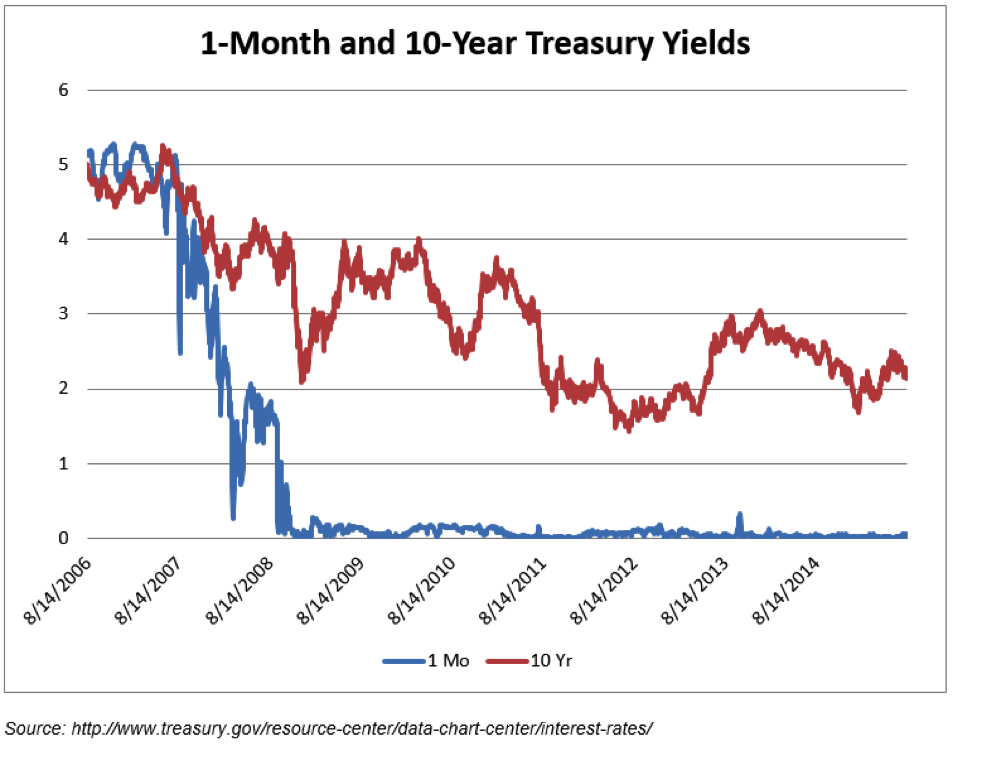

As investors prepare for the gradual “lift-off” in interest rates, it is worth reviewing the impact of exceptionally low rates on the fixed income markets. The last time the Federal Reserve raised the Federal Funds Rate was June 2006, almost a decade ago. One-month T-Bill yields have been close to zero since Lehman Brothers collapsed in September 2008 and ten-year Treasury bond yields have mostly been in the 2%-3% range for the last five years.

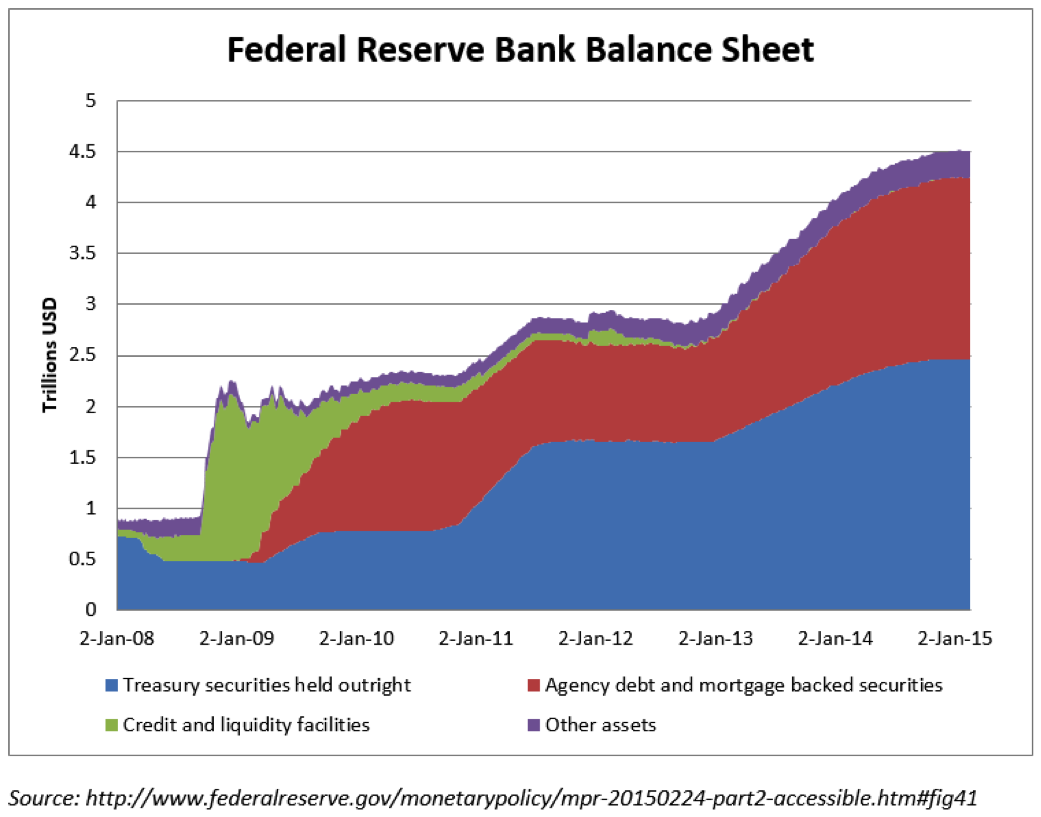

Faced with the biggest challenge to the financial system since the Great Depression and without the ability to take interest rates any lower, authorities implemented untraditional means of stimulating demand in the economy. Open market operations, or quantitative easing, were used to keep credit artificially cheap. The Federal Reserve Balance sheet ballooned from under $1 trillion in assets prior to the crisis, to an estimated $4.5 trillion today.

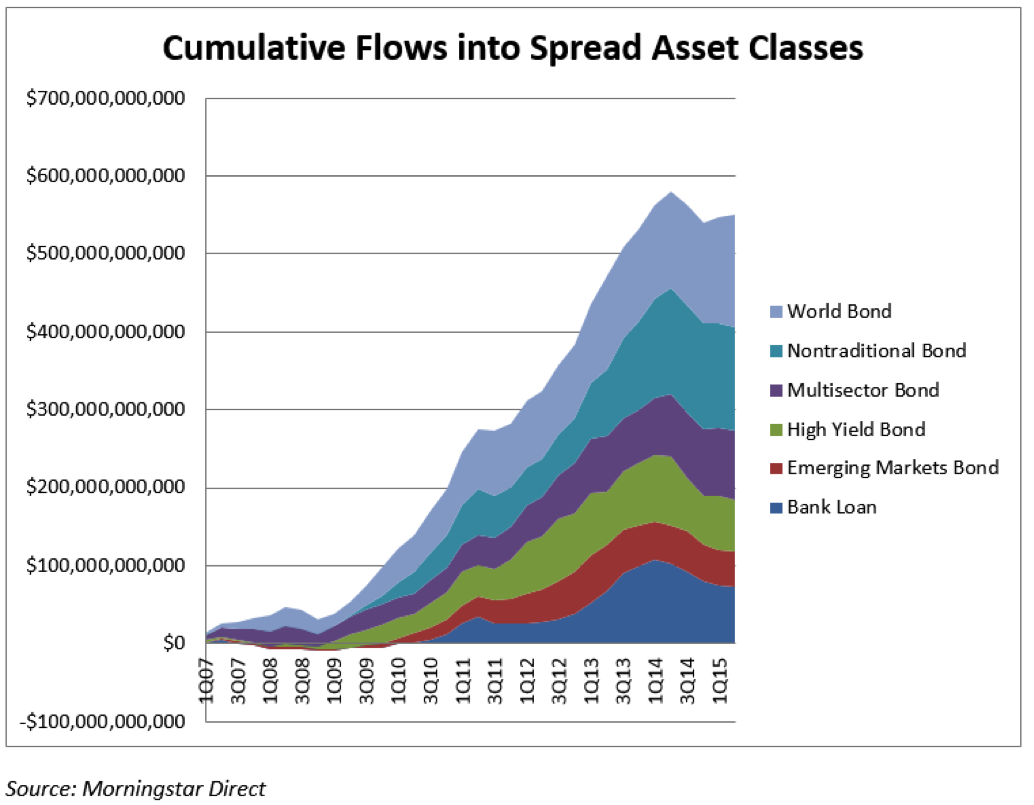

We’ll leave the discussion of the impact of these decisions on the equity market for another day. The focus of this discussion is the fixed income market and investment yields. Certainly the impact upon investors seeking income was very negative. With investment grade rates barely keeping pace with inflation, investors started ‘chasing yield’ wherever it might be found…high yield bonds, emerging market debt, world bond funds, bank loan funds, “non-traditional” and “multi-sector” bonds funds, et cetera. The graph below shows a cumulative estimated flow of $550bn into these “spread” asset classes since January 2007.

Of course with all the new money flowing into these asset classes, the spreads over Treasuries have come down, so on an absolute basis investors are still struggling to find investments with enough income for their needs.

Chasing Investment Yield

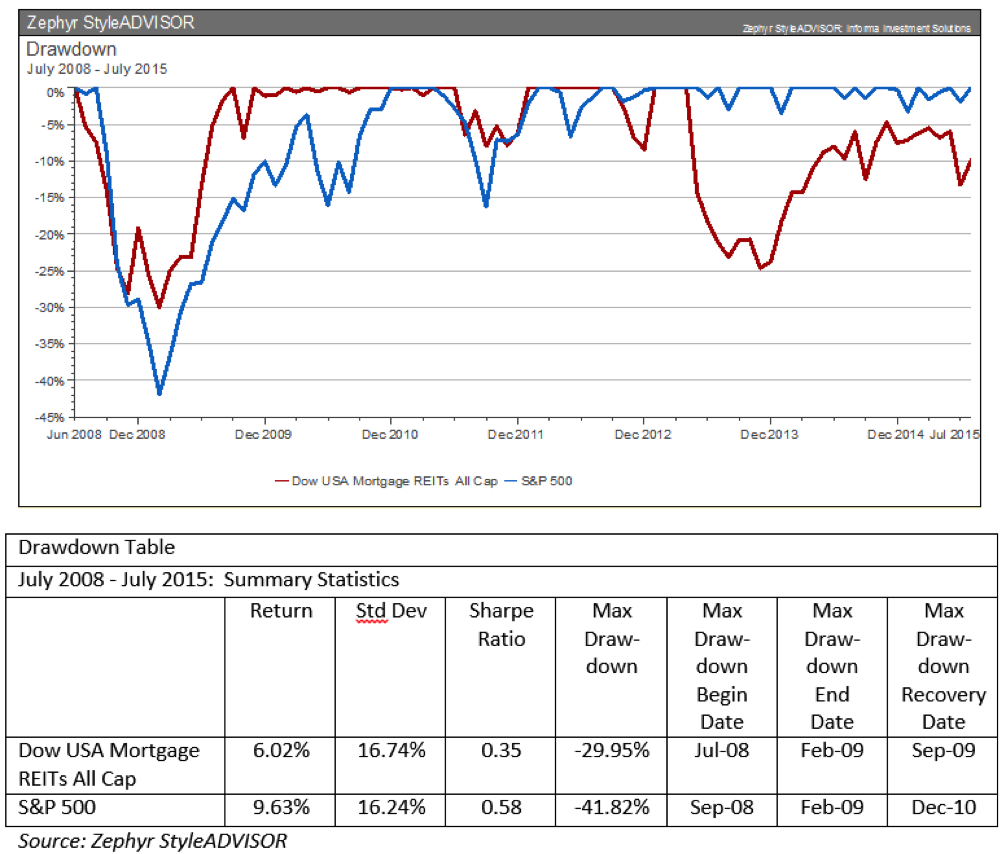

This habit of ‘chasing yield’ could lead an investor straight off a cliff. Mortgage REITs have offered very seductive yields over the last several years, hovering in the double-digit range. However, such investments depend upon leverage and a steep yield curve in order to provide such generous yields. When those conditions turn unfavorable, mortgage REITs have been very volatile and have seen steep, rapid drawdowns in value. During the “taper tantrum” of 2013, the Dow USA Mortgage REITs All Cap index lost almost 25%, with a loss of over 14% coming in the month of May 2013 alone.

We would argue that the quest for yield is a bit short-sighted and that really investors should be focused upon the total return of an investment. Too many investors focus just on the yield component of total return and miss the importance of capital gains. At the end of the day, a dollar gained is a dollar gained and one shouldn’t care how that dollar is generated. Moreover, by leaving gains invested one could reap the benefits of compounding returns.

Another Way to Pursue Returns and Endure a Low Yield World

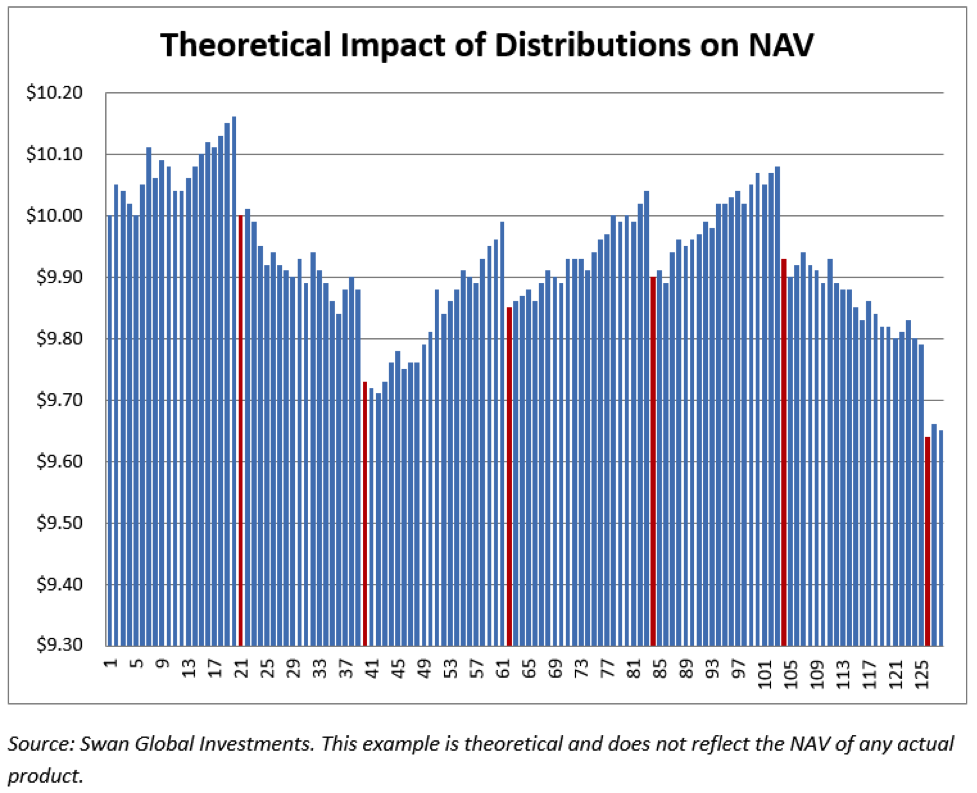

Below we see the theoretical daily NAVs for an imaginary fund. Although the NAVs here are fictional, the impact that a distribution has on NAV is not. The NAV will always decrease by the amount of the distribution. The NAV bars highlighted red show the post-distribution of taking a distribution. While the yield-focused investor might be happy to be receiving their income they are no better off in terms of total wealth.

This kind of return profile – a slow increase in the value of an investment, coupled with regular distributions from the value of the account – can easily be replicated by creating a systematic withdrawal plan. With a systematic withdrawal plan the investor liquidates a small portion of their portfolio every month or quarter in order to meet their spending needs.

In a way, a systematic withdrawal plan is similar to the dollar-cost averaging and regular 401(k) purchases many savers are familiar with during their working years when they were building up their nest eggs. The systematic withdrawal can be explained as the reverse of that. During the accumulation stage, investors saved what they could every paycheck period. In retirement, a systematic withdrawal plan simply reverses that flow.

When it comes to taxation, a systematic withdrawal plan may actually be preferable to a pure income-based plan. After all, income is taxed at regular income rates, whereas systematic withdrawals out of a long-term holding would likely be taxed at a long-term capital gains rate. Although many different variables come in to play when calculating after-tax returns, a systematic withdrawal plan does have its advantages.

In the wake of this extraordinary, post-crisis environment, it does seem unlikely that fixed income can fulfill its traditional role of capital preservation and income within a portfolio. It is important to remain focused on the big picture: wealth and the preservation of it, not investment yield, will determine whether or not an investor will be able to meet their retirement goals.

Marc Odo, CFA®, CAIA®, CIPM®, CFP®, Director of Investment Solutions, is responsible for helping clients and prospects gain a detailed understanding of Swan’s Defined Risk Strategy, including how it fits into an overall investment strategy. Formerly Marc was the Director of Research for 11 years at Zephyr Associates.

Important Notes and Disclosures:

Swan Global Investments, LLC is a SEC registered Investment Advisor that specializes in managing money using the proprietary Defined Risk Strategy (“DRS”). SEC registration does not denote any special training or qualification conferred by the SEC. Swan offers and manages the DRS for investors including individuals, institutions and other investment advisor firms. Any historical numbers, awards and recognitions presented are based on the performance of a (GIPS®) composite, Swan’s DRS Select Composite, which includes non-qualified discretionary accounts invested in since inception, July 1997, and are net of fees and expenses. Swan claims compliance with the Global Investment Performance Standards (GIPS®). All data used herein; including the statistical information, verification and performance reports are available upon request. The S&P 500 Index is a market cap weighted index of 500 widely held stocks often used as a proxy for the overall U.S. equity market. Indexes are unmanaged and have no fees or expenses. An investment cannot be made directly in an index. Swan’s investments may consist of securities which vary significantly from those in the benchmark indexes listed above and performance calculation methods may not be entirely comparable. Accordingly, comparing results shown to those of such indexes may be of limited use. The adviser’s dependence on its DRS process and judgments about the attractiveness, value and potential appreciation of particular ETFs and options in which the adviser invests or writes may prove to be incorrect and may not produce the desired results. There is no guarantee any investment or the DRS will meet its objectives. All investments involve the risk of potential investment losses as well as the potential for investment gains. Prior performance is not a guarantee of future results and there can be no assurance, and investors should not assume, that future performance will be comparable to past performance. All investment strategies have the potential for profit or loss. Further information is available upon request by contacting the company directly at 970-382-8901 or www.swanglobalinvestments.com. 047-SGI-100615