When it rains, it pours

We have been bemoaning the “correction” in MLPs for a year now, and waiting for this phase to pass. Unfortunately, this quarter saw the correction in MLPs turn into a rout. The Alerian MLP Index (the “Index”) experienced its worst quarter since 2008, falling 22.1% for the quarter, bringing its year-to-date return to -30.7%. To put this in perspective, the S&P Energy Select Sector Index fell only 18.0% for the quarter and 21.0% for the year-to-date period. The crescendo of selling peaked in September when the Index fell 15.3%. We cannot point to any specific news to account for this, and posit that a combination of forced selling from leveraged closed-end funds and others, open-end fund and ETF redemptions and short selling from hedge funds created the conditions for the sell-off. Already in October the prices of MLPs are rebounding lending support to the notion that a good bit of the selling in September was related to end of the quarter effects for various investors in the midstream sector.

The index shown is for informational purposes only and is not reflective of any investment. An investor cannot invest directly in an index. Indices do not include fees or operating expenses and are not available for actual investment. They are unmanaged and shown for illustrative purposes only. The Alerian MLP Index (NYSE: AMZ) is a composite index of the 50 most prominent energy master limited partnerships.

Flight to safety

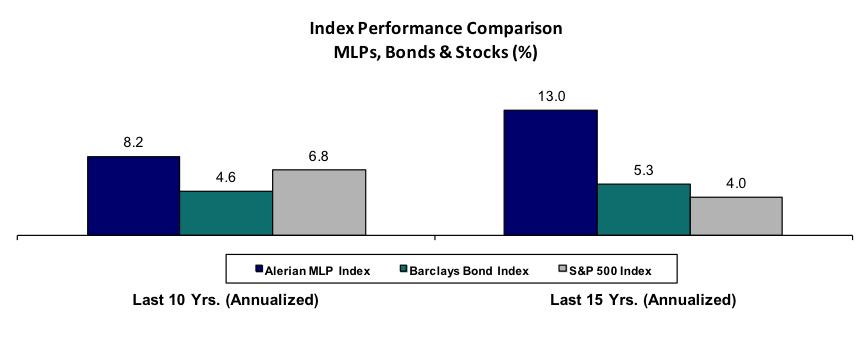

The poor performance of MLPs also reflected a sell-off in all risk assets. The S&P 500 Index declined 6.4% this past quarter while fixed income assets rose. This recent performance has dented the longer term outperformance of MLPs versus bonds and stocks, however, MLPs have significantly outperformed other asset classes, with the 15-year annual return for MLPs approximately 9.0% per year above the annual return for U.S. stocks.

*The inception of the Alerian MLP Index was June 1, 2006; however, Alerian publishes hypothetical index data beginning January 1, 1996.

The indices shown are for informational purposes only and are not reflective of any investment. As it is not possible to invest in the indices, the data shown does not reflect or compare features of an actual investment, such as its objectives, costs and expenses, liquidity, safety, guarantees or insurance, fluctuation of principal or return, or tax features. Indices do not include fees or operating expenses and are not available for actual investment. Indices presented are representative of various broad base asset classes. They are unmanaged and shown for illustrative purposes only. Data from Alerian and Bloomberg. Past performance is not indicative of future results. The Alerian MLP Index does not represent the Eagle MLP Strategy Fund.

Some of the selling over the past quarter was probably related to a decline in the price of oil, down another 20% in the quarter, as hopes for a quick rebound in prices this year readjusted to a “lower for longer” outlook for the commodity. Futures, which earlier this year allowed producers to sell oil for delivery in December of 2016 at near $70, now trade in the low $50s. Of course the cash flows of most MLPs are not directly affected by the price of oil, but by volumes, and while analysts have adjusted lower their expected production of oil from North America in the near-term, the decline in production is only expected to last one to two years before resuming growth, and the outlook for gas production is still robust. While we have adjusted our models to take account of this for individual MLPs and midstream companies, it does not explain the severity of the decline in prices.

Despite the decline in stock prices, the fact is that cash flows of our portfolio companies have been largely what we have been forecasting and distribution growth is on track to meet our forecasts. This past quarter our portfolio companies saw on average an increase in their distribution of 4.0% over the prior quarter, and are on track to meet the 10%+ distribution growth for 2015 that we forecasted at the beginning of this year. For the MLP market in general, the weighted average MLP distribution in the third quarter was a healthy 6.7% higher than a year ago.

Past performance is not indicative of future results.

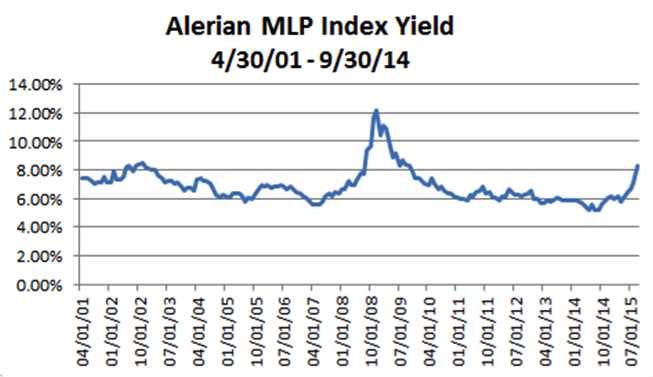

Despite this, during the quarter the yield of the Alerian MLP Index rose from 6.5% to 8.3%. In contrast, most other interest rates fell in the quarter, leading to significant increases in yield spreads of MLPs versus alternative yielding asset classes.

There are numerous challenges that many have highlighted for MLPs from the fall in oil prices and what that means for future production, less accommodating capital markets now for MLPs needing to raise money, and the outlook for future infrastructure needs. Indeed, these challenges appear so great that some financial commentators have declared “the death of the MLP”. But we believe many are overlooking a number of positive factors impacting this area. Spurred by lower prices, growth in the demand for hydrocarbons globally is strong. “Lower for longer” appears also to apply for interest rates in our economy as inflation stays stubbornly low and employment growth moderates. Finally, MLPs have faced more difficult capital markets in the past and the business model proved resilient.

We believe the MLP business model retains its unique advantages. It is still, in our opinion, the most efficient corporate structure to distribute cash flows from steadily earning assets, especially for taxable investors. The model of using the capital markets primarily to raise money for new investments rather than utilizing internally generated cash flow is believed to be the most effective method to guard against corporate hubris and malinvestment. The natural monopoly nature of many of the underlying assets affords MLPs pricing stability that is the envy of most other businesses. While currently low valuations in the equity markets creates challenges for those companies that need to raise money for new investment, history has consistently shown that these periods pass. The bond markets are still open to MLPs at, what we believe to be, attractive rates and other avenues are available (preferreds, PIPEs, parent company measures) to MLPs to raise capital at attractive costs. The advantages and competitiveness of North American shale assets will only grow over time and we expect production to resume its increase at some point. We believe the recent sell off in MLPs is due to forced selling and a typical equity market cascade and overshoot, which has created a potentially attractive opportunity for investors to allocate to the asset class. Adapting Mark Twain to the MLP market, the reports of its demise are greatly exaggerated.

MLP Valuations appear Compelling

With the sell-off in MLPs and midstream energy infrastructure companies, valuations have approached levels not seen for many years. The yield on the Alerian MLP Index is back to levels not seen since late 2009, almost 6 years ago, as the market emerged from the financial crisis. This level is higher than it has been, outside of the financial crisis period, for the last 15 years (except for a few observations in 2002).

Source: Alerian. The inception of the Alerian MLP Index was June 1, 2006; however, Alerian publishes hypothetical index data beginning January 1, 1996. Past performance is not indicative of future results.

Compared with other income producing publicly traded assets, the spread of MLP yields versus Baa corporate bonds and Ba high yield bonds appears to the be the largest in the last 20 years (which is the extent of our history); compared with REITs, MLP yields are near their highest spreads experienced in the last 20 years, and versus the 10-year Treasury, are at their highest spread except for the financial crisis period. On all metrics, we believe valuations for MLPs look attractive. In fact, Wells Fargo estimates that MLPs are trading 10-20% below historical median valuation levels as measured by commonly used valuation metrics, Enterprise Value (“EV”) to EBITDA and EV to Distributable Cash Flow.

Capital Market Conditions

Fund flows into the MLP sector slowed dramatically during the quarter, exacerbating the sell-off in MLPs. Fund flows into the MLP sector (tracked by following open and closed-end mutual funds, ETFs, and ETNs) were negative in the quarter to the tune of $57 million. This is the first quarter these investment vehicles have been negative. This compares to almost $3 billion of overall new flows into the sector during the first half of the year and almost $4 billion of inflows in the third quarter of last year. In particular, open-end funds saw $450 million of redemptions this quarter. The overall net outflow has no doubt contributed to headwinds for unit prices.

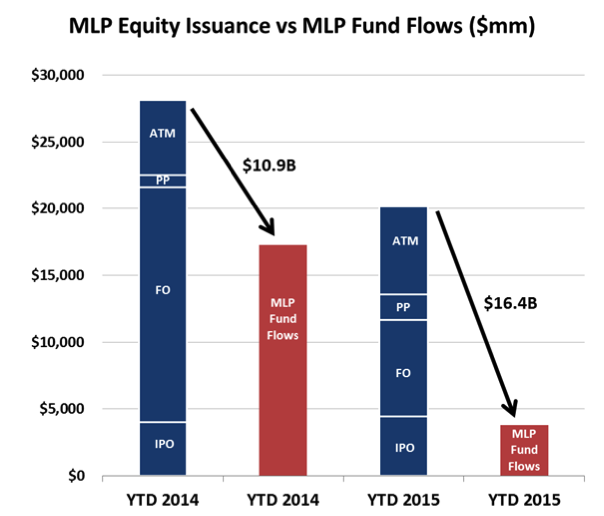

Capital raising activity also slowed down meaningfully during the quarter in response to weak demand. We did not see any IPOs come to market during the third quarter and MLP equity issuance slowed to $1.3 billion vs. $4.1 billion of new MLP equity capital raised in the second quarter this year and $6.7 billion of equity capital raised during the third quarter last year. Overall, the slowdown in money raised has not been as great as the reduction in new visible fund flows into the sector, leading to an increase in the gap between needs versus sources. US Capital analysts estimate that the gap between supply of equity and visible demand has risen from $10.9 billion in first 9 months of 2014 to $16.4 billion in the same period this year (see below).

Glossary of equity issuance terms for above chart: ATM-At the Market; PP-Private Placement; FO-Follow On; IPO-Initial Public Offering.

While we may view the recent trading of MLPs as irrational, we do recognize that technical selling can affect fundamentals since it raises the cash cost of equity for companies that need to raise capital to fund acquisitions or new development. There is evidence that companies that have near-term capital funding needs have been punished more by the markets than companies that do not need to tap the equity markets as much. For those companies that need to tap the capital markets, there are a number of strategies that they can adopt to ease their way in this market. For those that have parent sponsors or associated private equity backers, we see a number of MLPs using these relationships to assist their capital raising efforts. These sponsors often take a portion of any equity offerings by their associated MLPs, or if they are selling an asset, they can forego incentive distribution rights for a period of time or reduce the price at which the assets are sold to their associated MLPs. We expect other companies to resort to more PIPE (private investment in public equity) offerings, preferred securities, or other equity hybrid offerings in this environment. Finally, history has shown that difficult capital raising conditions do not exist for long in the MLP marketplace, and we would expect that pricing will improve at some point and open the door for believed attractive costs of financing.

Furthermore, we believe conditions in the bond markets remain favorable and we continue to see MLPs raise capital at attractive rates. Throughout the recent equity market volatility for MLPs, publicly traded bonds of MLPs have not sold off similarly. For example, Plains All American Pipeline LP, whose equity sold off dramatically in the quarter, had its bonds due in 2024 trading at 4.4% yields in early October, about where they yielded at the beginning of the quarter. Recently Enbridge Energy Partners issued $500 million in 10 year notes at 5.875%. S&P announced they were putting Tesoro Logistics LP on credit watch upgrade. Following its merger announcement with Williams, both S&P and Moody’s announced they would put Energy Transfer Equity on a credit watch for an upgrade. The recent decision by the Fed to not raise interest rates will also help keep rates favorable to MLPs wishing to raise money in the bond markets.

Individual company developments

While most companies reported Q2 earnings that were generally in line with market expectations, the management team of Plains All American Pipeline LP (PAA) caught investors off guard when they reported earnings in early August. 2015 EBITDA guidance and distribution growth guidance were only slightly revised lower; however, comments regarding 2016 distribution growth along with broader industry comments drove weakness in both PAA and its general partner, PAGP, as well as across other MLP names. Management alluded that distribution growth in 2016 could be put on hold versus market expectations of roughly 6% growth. This contributed to an 11% decline for PAA, a 23% decline for PAGP, and about a 5% decline for the whole MLP market. After having conversations with the Plains management team post earnings, we come away believing that while the Plains companies have some headwinds in 2016, EBITDA growth is still expected to come from projects coming online to help offset weakness in the base business. Greg Armstrong, the CEO of Plains All American Pipeline LP, clarified his comment for no distribution growth in 2016 as being his lower end of guidance. Michael Mears, the CEO of Magellan Midstream Partners, specifically addressed some comments that were made on the Plains conference call regarding overbuild in capacity by reminding investors that Magellan’s four large crude oil pipelines are all supported with long-term take-or-pay contracts that do not come up for re-contracting for a quite some time. Nonetheless, we are not cavalier about the issues raised by the Plains management team. We have adjusted our models to take into account counterparty risk on contracts across the asset portfolios of all our investments.

At the end of the quarter, Williams Companies agreed to accept a slightly revised offer from Energy Transfer and terminated its merger offer for affiliate Williams Partners. The Energy Transfer management team highlighted costs savings and achievable synergies from the merger. While the market sold off these names dramatically, we think the deal is accretive for Energy Transfer and believe there is upside if the synergies are fully realized. While some have raised concerns about increased capital expenditure for the combined companies in this market, we believe technical factors such as investors with large overlap in both positions trying to reduce concentration risk was the main reason for the sell-off.

One other issue is that it will increase the complexity of the Energy Transfer network of companies. Energy Transfer Equity will issue a newly created security called Energy Transfer Corp, which will be a C-corp like Kinder Morgan, not an MLP. As this entity will basically be a shell entity that will hold shares of Energy Transfer Equity, the parent MLP, it remains to be seen how it will be valued in the marketplace. We still like Energy Transfer Equity and the value proposition at these levels and believe that unit prices will stabilize as the market works through some of these factors.

Consolidation was also evident elsewhere in the quarter. Another notable transaction was the proposed purchase of MarkWest Energy Partners by MPLX, LP. Additionally, Genesis Energy LP acquired offshore Gulf of Mexico assets from Enterprise Product Partners for $1.5 billion further bolstering their position in offshore market. Kinder Morgan (KMI) continued to lay the groundwork for a $2 billion new pipeline to bring gas from Pennsylvania to the Northeast and New England Markets. A study commissioned by KMI showed that approximately $3.7 billion in wholesale electricity cost savings would have been achieved during the 2013-2014 “Polar Vortex” had the pipeline been in service at that time.

Crude Oil Exports Stall

A bi-partisan push in Congress for lifting the decades long ban on crude oil exports from the U.S. progressed during the quarter; however, we continue to give long odds to its repeal. In September the House Energy and Commerce Committee passed a bill allowing for the 1970’s era ban to be lifted. However, the Senate and the White House have not yet endorsed the change in policy. Capital Alpha, a consultant in DC, still puts the odds of lifting the export ban at 25-30% in 2015 and 50-60% within the next year. While we believe the need for energy infrastructure will continue to grow at a steady pace, a favorable outcome for lifting the export ban would create a multi-billion dollar opportunity for MLPs in addition to our current outlook for infrastructure build out.

IRS Update

The IRS gave an update on its proposed changes to the rules governing what constitutes qualifying income for MLPs. The IRS continues to receive comments and testimony about its proposed rule changes, and it has indicated that it will modify some of the newly proposed rules before the process is over. We believe these rules will not be material for the types of MLPs we purchase for the Fund, and we view the issues at this point as not a major factor in MLP valuations. As for questions about the general tax treatment of MLPs, and whether some new industries like renewable power would be legislatively added to the MLP qualifying income regulations, we believe that is on hold for this Congress and would only be addressed in a general corporate tax reform effort, which is viewed as remote at this point.

Long Term Prospects for MLPs May be Very Attractive

Despite recent performance, we are optimistic about the outlook for MLPs and midstream energy infrastructure companies in the long run. Bottom line, we see the demand for midstream services to continue to expand. While we expect the volumes of oil will decline in the coming quarters, we expect the volumes of gas to be produced will still increase. And while oil is in oversupply at the current time, strong demand growth is being spurred by lower prices. Goldman Sachs recently noted that global oil product demand was up 1.7 million barrels per day (bpd) in the first half of 2015 versus flat growth in the same period last year, and they forecast another 1.3 million bpd growth in 2016. This growth is primarily being driven by increases in the demand for gasoline in the U.S, China, and India, to such a point that Goldman Sachs opines that gasoline could be in a “structural shortage” in that global demand for gasoline may exceed global refining capacity. Demand growth of this degree will certainly eat into the excess supply of oil in the coming quarters and years.

David Chiaro

David Chiaro is Co-Head of MLP Strategy for Eagle Global Advisors, LLC

Co-Advisor of the Eagle MLP Strategy Fund

Disclosures:

Investors should carefully consider the investment objectives, risks, charges and expenses of the Eagle MLP Strategy Fund. This and other important information about the Fund is contained in the prospectus, which can be obtained by calling 1-888-868-9501 or visiting www.eaglemlpfund.com. The prospectus should be read carefully before investing. The Eagle MLP Strategy Fund is distributed by Northern Lights Distributors, LLC member FINRA/SIPC. This is an actively managed dynamic portfolio. There is no guarantee that any investment (or this investment) will achieve its objectives, goals, generate positive returns, or avoid losses. The information provided should not be considered tax advice. Please consult your tax advisor for further information. Eagle Global Advisors, Princeton Fund Advisors, LLC and Northern Lights Distributors, LLC are not affiliated.

A master limited partnership (MLP) is a limited partnership that is publicly traded on a securities exchange. It combines the tax benefits of a limited partnership with the liquidity of publicly traded securities. To qualify for MLP status, a partnership must generate at least 90 percent of its income from what the Internal Revenue Service (IRS) deems "qualifying" sources, generally relating to the production, processing or transportation of natural resources, such as oil and natural gas.

The Alerian MLP Index is a composite of the 50 most prominent energy master limited partnerships calculated by Standard & Poor's using a float-adjusted market capitalization methodology.

A real estate investment trust (REIT) is a security that sells like a stock on the major exchanges and invests in real estate directly, either through properties or mortgages. REITs receive special tax considerations and typically offer investors a regular distribution, as well as a highly liquid method of investing in real estate.

Risk Factors:

Credit Risk: There is a risk that note issuers will not make payments on securities held by the Fund, resulting in losses to the Fund. In addition, the credit quality of securities held by the Fund may be lowered if an issuer’s financial condition changes.

Distribution Policy Risk: The Fund’s distribution policy is not designed to guarantee distributions that equal a fixed percentage of the Fund’s current net asset value per share. Shareholders receiving periodic payments from the Fund may be under the impression that they are receiving net profits. However, all or a portion of a distribution may consist of a return of capital (i.e. from your original investment). Shareholders should not assume that the source of a distribution from the Fund is net profit. Shareholders should note that return of capital will reduce the tax basis of their shares and potentially increase the taxable gain, if any, upon disposition of their shares.

ETN Risk: ETNs are subject to administrative and other expenses, which will be indirectly paid by the Fund. Each ETN is subject to specific risks, depending on the nature of the ETN. ETNs are subject to default risks. Foreign Investment Risk: Investing in notes of foreign issuers involves risks not typically associated with U.S. investments, including adverse political, social and economic developments, less liquidity, greater volatility, less developed or less efficient trading markets, political instability and differing auditing and legal standards.

Interest Rate Risk: Typically, a rise in interest rates can cause a decline in the value of notes and MLPs owned by the Fund.

Liquidity Risk: Liquidity risk exists when particular investments of the Fund would be difficult to purchase or sell, possibly preventing the Fund from selling such illiquid securities at an advantageous time or price, or possibly requiring the Fund to dispose of other investments at unfavorable times or prices in order to satisfy its obligations.

Management Risk: Eagle’s judgments about the attractiveness, value and potential appreciation of particular asset classes and securities in which the Fund invests may prove to be incorrect and may not produce the desired results. Additionally, Princeton’s judgments about the potential performance of the Fund’s investment portfolio, within the Fund’s investment policies and risk parameters, may prove incorrect and may not produce the desired results.

Market Risk: Overall securities market risks may affect the value of individual instruments in which the Fund invests. Factors such as domestic and foreign economic growth and market conditions, interest rate levels, and political events affect the securities markets.

MLP Risk: Investments in MLPs involve risks different from those of investing in common stock including risks related to limited control and limited rights to vote on matters affecting the MLP, risks related to potential conflicts of interest between the MLP and the MLP’s general partner, cash flow risks, dilution risks and risks related to the general partner’s limited call right. MLPs are generally considered interest-rate sensitive investments. During periods of interest rate volatility, these investments may not provide attractive returns. Depending on the state of interest rates in general, the use of MLPs could enhance or harm the overall performance of the Fund.

MLP Tax Risk: MLPs, typically, do not pay U.S. federal income tax at the partnership level. Instead, each partner is allocated a share of the partnership’s income, gains, losses, deductions and expenses. A change in current tax law or in the underlying business mix of a given MLP could result in an MLP being treated as a corporation for U.S. federal income tax purposes, which would result in such MLP being required to pay U.S. federal income tax on its taxable income. The classification of an MLP as a corporation for U.S. federal income tax purposes would have the effect of reducing the amount of cash available for distribution by the MLP. Thus, if any of the MLPs owned by the Fund were treated as corporations for U.S. federal income tax purposes, it could result in a reduction of the value of your investment in the Fund and lower income, as compared to an MLP that is not taxed as a corporation.

Energy Related Risk: The Fund focuses its investments in the energy infrastructure sector, through MLP securities. Because of its focus in this sector, the performance of the Fund is tied closely to and affected by developments in the energy sector, such as the possibility that government regulation will negatively impact companies in this sector. Energy infrastructure entities are subject to the risks specific to the industry they serve including, but not limited to, the following: Fluctuations in commodity prices; Reduced volumes of natural gas or other energy commodities available for transporting, processing, storing or distributing; New construction risk and acquisition risk which can limit potential growth; A sustained reduced demand for crude oil, natural gas and refined petroleum products resulting from a recession or an increase in market price or higher taxes; Depletion of the natural gas reserves or other commodities if not replaced; Changes in the regulatory environment; Extreme weather; Rising interest rates which could result in a higher cost of capital and drive investors into other investment opportunities; and Threats of attack by terrorists.

Non-Diversification Risk: As a non-diversified fund, the Fund may invest more than 5% of its total assets in the securities of one or more issuers. Small and Medium Capitalization Company Risk: The value of a small or medium capitalization company securities may be subject to more abrupt or erratic market movements than those of larger, more established companies or the market averages in general. Structured Note Risk: MLP–related structured notes involve tracking risk, issuer default risk and may involve leverage risk. Mutual Funds involve risk including possible loss of principal.

6547-NLD-10/22/2015