Remember Greece? Neither Does the Market.

As we wrote our last quarterly piece, the world was monitoring developments regarding a Greek referendum, viability of the Euro and as an aside, emanations from China that things might be getting worse. As Greece’s financial and political woes have returned to being a local problem, China’s local problems became the central thrust of market moves in the third quarter.

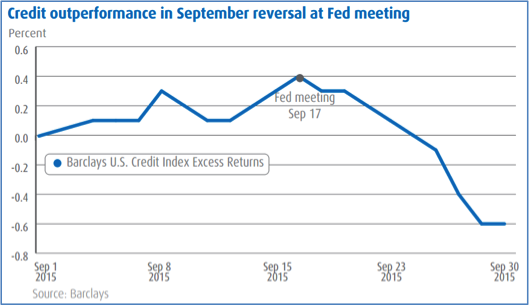

The worst quarter for U.S. equities since 2011, an intra-quarter doubling of equity market volatility and a significant commodities sell-off all have their roots in China’s stock market tanking and economic data slowing. Despite the ugly July and August for risk assets, by September markets had begun to heal. But as markets, particularly credit markets, had appeared to digest the China news, the Fed introduced a new wrinkle.

Now we’re global?

The September Fed meeting was viewed as the first meeting with a realistic possibility of a rate hike occurring. Going into the meeting, Fed Funds futures implied an approximately 30% probability of an increase and not long before, futures had projected close to, and at points above, a 50% chance.

Rather than the hike some expected, the Fed left rates unchanged and accompanied them with dovish language intended as further accommodation to markets. However, instead of interpreting the statements as one of continued support for risk assets as it was likely intended, the market focused on the surprising concern regarding “recent global economic and financial developments” as an indication that global conditions (particularly China) were worse than the market anticipated, prompting the question, “What do they know that we don’t?”

Market reaction to the language about foreign concerns was amplified by perception that this language was a departure from precedent for the Fed. Some Fed watchers asked (perhaps facetiously) if the Fed now had a triple mandate, adding global growth to the existing mandate of price stability and full employment.

The question of a global responsibility for this Fed harkens back to January 2014, after the Fed had begun the tapering program and shortly after Janet Yellen assumed the role of Chair. Raghuram Rajan, the head of India’s central bank, sharply criticized the Fed tapering decision as selfish. “Emerging markets tried to support global growth by huge fiscal and monetary stimulus,” he said referring to actions taken during the 2008 credit crisis, “and they can’t at this point wash their hands off and say, ‘we’ll do what we need to and you do the adjustment.’ ”

In her Semiannual Monetary Policy Report to the Congress on February 11, 2014, Janet Yellen dismissed this argument as one might expect from a nation’s central banker. She discussed the relevance of conditions as they related to the nation whose monetary policy she is responsible for. “We have been watching closely the recent volatility in global financial markets. Our sense is that at this stage these developments do not pose a substantial risk to the U.S. economic outlook.”

Do the more recent comments then reflect a change in philosophy, paying more heed to foreign needs, or simply an awareness that current economic developments abroad do indeed pose a risk to the U.S. economic outlook?

The market tightened for the Fed

Though the U.S. is perhaps the most self-contained economy in the world, global developments have long played a role in U.S. economic conditions. Currency strength, by its very nature, is a global phenomenon and intimately tied to the interest rate differentials and flows of funds between nations. The dollar strengthened significantly since June 2014 due to relatively higher growth, interest rates, and instability abroad and questioning of the viability of the Euro. The Fed has estimated that a 10% increase in the dollar during a quarter would detract 0.5% from gross domestic product in the first year and another 0.2% in the following year. From the outset of the currency increase, economists have expected a decrease in exports and increase in imports, net negatives for U.S. economic growth.

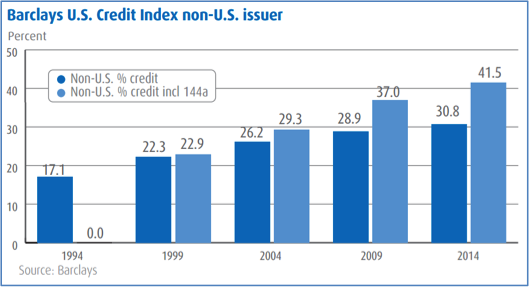

Equity markets were certainly impacted this quarter by global concerns as was commodity pricing. Oil, one of the key factors in U.S. inflation metrics, is largely driven by global demand, which is driven by global growth (and to a degree currency moves as it is priced in dollars). U.S. credit markets are exclusively American in name only. The U.S. has seen significant increases in non-U.S. entities issuing in U.S. dollars to take advantage of the world’s deepest, most liquid debt markets. Representative of the globalization of financial markets a whole and fixed income markets in particular, now approximately 40% of U.S. Credit is issued international entities and this does not even reflect the global nature (or geographic mix or international reach) of the U.S. entities tapping U.S. credit markets.

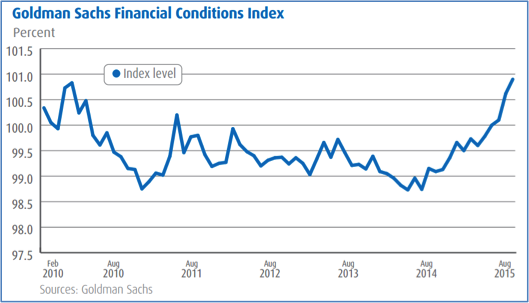

What credit markets, dollar strength, equity markets and oil have in common is that they are the key components in financial conditions for the real economy in the U.S. The Goldman Sachs’ U.S. Financial Conditions Index, which relies on those variables, rose to its highest level in five years indicating the tightest financial conditions since June 2010. Tighter financial conditions, partially due to global developments and partially due to significant debt issuance already year to date, weigh into the Fed’s decisions on monetary policy.

Transmission mechanism

While the public discourse continues to focus on Fed decisions relating to when to raise the Fed Funds rate target, there has been significant tightening of financial conditions even without the Fed taking action. As a general rule, the transmission mechanism from tightening at the front end to the real economy is about one half to one third of the move in the Fed Funds rate. Conversely, the approximately 65-basis-point move higher since June 2014 in the option adjusted spread of the Barclay’s U.S. Credit index is equivalent to about a 130 to 195 basis point increase in the Fed Funds Rate. With this backdrop, the Fed’s September decision to defer hiking rates becomes increasingly more logical.

Given this economic reality and the Fed’s introduction of global conditions, it appeared the Fed had missed its window to raise rates near term. The disconnect, however, is that the Fed Chair Yellen and her compatriots continue to repeatedly suggest they will raise rates this year, repeating this message several times since its mid-September meeting and explicitly referring to its “next” meeting in December as a possible liftoff in the Fed October statement. With Chinese growth concerns unlikely to abate by December, the Fed appeared to have created a narrow channel to navigate. We are led to suspect the Fed is watching the Fed Funds futures more closely than many market participants, hoping the market will give an ‘all clear’ signal by pricing in a rate hike before they take action. The language suggesting a rate hike this year then is almost a request of markets to give that signal. The request may be working. The October Fed statement seemed to deliberately walk back the global “concerns” to merely worth “monitoring”, which has pushed Fed Funds futures to just shy of the 50% level for a move in December.

Flipping the script

Rate hikes were originally supposed to follow the unwinding of the Fed’s balance sheet from quantitative easing. This plan morphed over time to suggest an end to reinvestment of maturing assets rather than outright sales, which further changed to suggest that the reinvestment would end at the same time as the first rate hike. Though our view was the Fed would take a more accommodative stance and only partially end reinvestment or do so over time, earlier this year the consensus remained that the Fed would end reinvestment with the first rate hike. This decision would allow an estimated $216 billion of maturing assets to roll off the Fed balance sheet in 2016.

Though it has eluded discussion in most popular press, the September Fed minutes included a discussion of different scenarios the Fed could employ to cease reinvestment of assets maturing on its $4.5 trillion balance sheet. Among the alternatives discussed was ending reinvestment when certain Fed Funds targets were reached, including 1%, 2% or even the unknown terminal point of rate hikes. Given the length of time it has taken to get even the first rate hike and our expectations that the Fed will move slowly and methodically with subsequent hikes, we expect reinvestment and thus deliberate support for the long end of the curve to remain in place for some time.

Test case

Nonetheless, an interesting test case has emerged for what a wind down of the balance sheet could look like. In August, as China slowed down significantly, it began selling reserves to make funds available for interventions in its own market, including support of the currency. Total sales of reserves exceeded $100 billion for the month, including the reduction of their U.S. Treasury holdings. China’s Treasury holdings have declined about $200 billion this year and current estimates are that China will sell about $40 billion of Treasuries a month for the remainder of 2015. $40 billion a month equates to nearly half a trillion dollars if continued for a year, far in excess of expected run-off from the Fed’s balance sheet per year. Despite these sales, Treasury yields have fallen this year, though the sales have coincided with fundamentals supporting low rates (slowing global economy and low inflation) and easy global monetary conditions. Further, with growing expectations that Europe will extend its quantitative easing program, Standard & Poor’s (S&P) published a report in September suggesting the program could grow to as large as €2.4 trillion in total, more than double the €1.1 trillion plan currently in place, continued support for low global government rates continues.

Conclusion

Global conditions are absolutely impacting the U.S. markets in known and established manners, but the Fed’s introduction of the language confused markets away from a perception of Fed support to one of Fed fear. Nonetheless, the Fed remains accommodative, which bodes well for risk assets in the U.S. The quarter was an extremely difficult one for financial markets with risk-off considerations overriding the fundamentals of individual issuers. As we look forward, however, the widening of credit spreads overall and the steepening of credit curves and quality curves have created a more attractive yield environment for investors.

Investment grade corporate bonds offering 5% are now readily available for the first time in several years. With the move wider in spreads being largely undifferentiated by issuer, the period was a very difficult one for security selection, but affords the opportunity to purchase potentially mispriced assets in anticipation of a return to rationality.

The potential for increased easing globally and weak growth and inflation abroad are supportive of low government bond yields. The divergence between the active easing abroad and the contemplation of tightening at home entrenches the divergence of U.S. and developed market monetary policy. That divergence paired with the relative economic strength of the U.S. and significantly higher U.S. yields versus other developed economies makes U.S. dollar assets, in particular U.S. fixed income assets, attractive in a global marketplace.

All investments involve risk, including the possible loss of principal.

Keep in mind that as interest rates rise, prices for bonds with fixed interest rates may fall. This may have an adverse effect on a portfolio.

Foreign investing involves special risks due to factors such as increased volatility, currency fluctuation and political uncertainties. High yield bond funds may have higher yields and are subject to greater credit, market and interest rate risk than higher-rated fixed-income securities. Keep in mind that as interest rates rise, prices for bonds with fixed interest rates may fall. This may have an adverse effect on a Fund’s portfolio.

Investments cannot be made in an index.

This presentation may contain targeted returns and forward-looking statements. “Forward-looking statements,” can be identified by the use of forward-looking terminology such as “may”, “should”, “expect”, “anticipate”, “outlook”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof, or variations thereon, or other comparable terminology. Investors are cautioned not to place undue reliance on such returns and statements, as actual returns and results could differ materially due to various risks and uncertainties. This material does not constitute investment advice. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. Investors should seek advice regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investment involves risk. Market conditions and trends will fluctuate. The value of an investment as well as income associated with investments may rise or fall. Accordingly, investors may receive back less than originally invested.

Taplin, Canida & Habacht, LLC is a registered investment adviser and a wholly owned subsidiary of BMO Asset Management Corp., which is a subsidiary of BMO Financial Corp. BMO Global Asset Management is the brand name for various affiliated entities of BMO Financial Group that provide investment management and trust and custody services. Certain of the products and services offered under the brand name BMO Global Asset Management are designed specifically for various categories of investors in a number of different countries and regions and may not be available to all investors. Products and services are only offered to such investors in those countries and regions in accordance with applicable laws and regulations. BMO Financial Group is a service mark of Bank of Montreal (BMO).

BMO Asset Management Corp. is the investment adviser to the BMO Funds. BMO Investment Distributors, LLC is the distributor. Member FINRA/SIPC.

BMO Asset Management Corp., BMO Investment Distributors, LLC, BMO Private Bank, BMO Harris Bank N.A. and BMO Harris Financial Advisors, Inc. are affiliated companies. BMO Private Bank is a brand name used in the United States by BMO Harris Bank N.A.

Investment products are: NOT FDIC INSURED — NOT BANK GUARANTEED — MAY LOSE VALUE.

© 2015 BMO Financial Corp. (3881966, 10/15)