Weighing the Week Ahead: What Will Higher Interest Rates Mean for Financial Markets?

Friday’s employment report, rightly or wrongly, confirmed expectations for a December shift in Fed policy. There will be a parade of Fed speakers. We can expect daily discussion about the implications. The punditry will be asking:

What will higher rates mean for financial markets?

Prior Theme Recap

In my last WTWA (two weeks ago) I predicted that the market story would focus on the FOMC and a possible change in policy. This was a good guess about the recurrent theme, although there have also been plenty of big earnings stories. To get the full story, let us look at Doug Short’s weekly chart. Doug’s full post discusses the muted effect of Friday’s strong payroll report. (With the ever-increasing effects from foreign markets, you should also add Doug’s World Markets Weekend Update to your reading list).

Doug’s update also provides multi-year context. See his full post for more excellent charts and analysis.

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead. You can make your own predictions in the comments.

This Week’s Theme

The economic calendar is modest and earnings season is winding down. The entire market mood shifted with the employment report. A 2015 rate hike that seemed very unlikely two weeks ago has now become the conventional wisdom. Markets made a quick adjustment on Friday, but is there more to come? Providing some help (??) we will have a weeklong series of speeches from Fed Governors and Presidents.

There will be many opportunities to opine on Fed policy and the consequences. Everyone will be asking:

What will higher rates mean for the markets?

Let’s divide this into two themes – the overall impact and specific markets.

-

Overall we have the three camps we have identified in the past:

- The market strength rests upon worldwide liquidity. Changing this could halt the rally.

- No. Fed policy has done little to help the economy, so gradual cuts will make little difference.

- No. As long as rate increases match economic growth, the market will respond well.

-

Sector effects are quite different, and vary widely.

- Bank stocks jumped about 2.8%.

- REITs declined.

- Utilities dropped 3.5% — almost a year’s worth of dividends in one day.

There are sources taking each of these positions. I expect it to be fiercely debated in the week ahead.

As always, I have my own ideas, reported in today’s conclusion. But first, let us do our regular update of the last week’s news and data. Readers, especially those new to this series, will benefit from reading the background information.

Last Week’s Data

Each week I break down events into good and bad. Often there is “ugly” and on rare occasion something really good. My working definition of “good” has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially – no politics.

- It is better than expectations.

The Good

The news of the week was mostly good.

- Signs of compromise in Washington. A highway bill and extension of the Export-Import bank passed in the House with bipartisan support. The vote was forced via an arcane procedure – the discharge petition – used when committee leadership is blocking a vote. (The Hill) Compromise will be needed to avoid a government shutdown with a deadline of December 11th. (The Hill) Bob McTeer objects to handing the bill to the Fed.

- Construction spending beat expectations with a monthly increase of 0.6%.

- Home prices increased 6.4% year-over-year according to CoreLogic. This is more recent (September) data than other measures and consistent with the prior month’s report. (Calculated Risk)

- ISM non-manufacturing was very strong at 59.1. Steven Hansen at GEI has the full story, with plenty of charts and comparisons. This table is particularly helpful.

- Private employment growth beat expectations. The ADP report showed a monthly increase of 189K private jobs. This is a totally different method from the government surveys and provides useful confirmation.

- Auto sales were very strong. The sector is “on fire” says Scott Grannis, who notes that the annualized rate of increase is 11% since 2009, 10% in the last year. Bespoke also notes the strength in F-150 sales, an interesting overall indicator.

-

The monthly employment report was strong. The employment news has so many dimensions that it is easy to spin. This time even the persistent critics had trouble finding a flaw. (Good WSJ summary of the numbers and additional commentary from New Deal Democrat).

- Headline net job gains of 271K beat expectations by about 90K.

- Labor force participation held steady at 62.4% and employment via the “household” report increased.

- The unemployment rate dropped to 5% and below 10% on the U6 measure, which includes discouraged workers and the under-employed.

- Voluntary versus involuntary part-time employment improved.

- Average hourly earnings increased – now up 2.5% year-over-year. (Calculated Risk)

The Bad

There was some negative news as well.

- Keystone pipeline rejected. The President finally acted on the Keystone pipeline, citing environmental and some economic reasons. I am scoring this as “bad” by using our stated criterion of what is “market-friendly” – not making a judgment of the environmental arguments. Republicans were close to a veto-proof majority on this legislation early in 2015, and probably could have done some horse trading for a few more votes. The proposal might resurface in 2017, depending upon the election results.

- Initial jobless claims moved higher. The level of 276K is still low by historic standards. The recent week was not part of the survey period for the October job report.

- ISM manufacturing was barely positive, at 50.1. Flat manufacturing activity is disappointing, even though the result was in line with expectations. Most people do not realize that the manufacturing index can and does signal economic growth even when below 50. According to the ISM, the current report is consistent with economic growth of 2.2%.

- Disappointing earnings. The worst since 2009, says Bloomberg. Beating on earnings expectations, but not on revenue, says FactSet. They also note that the averages were dragged down by companies generating more than half of their sales outside of the U.S., a 12.5% decline for the group. Brian Gilmartin is more upbeat, noting the distortions of 2008-09 and the recent impact from energy stocks. He sees a current world of stable and consistent earnings growth.

The Ugly

Complex, high-commission investment products. There are two in the news this week. Either might be suitable in the right circumstances, but sadly, that is not how they are often marketed.

Josh Brown takes up the non-traded REIT, where the salesperson gets an upfront 7% commission, He cites Simon Lack’s book, Wall Street Potholes, and then adds his own take.

Sen. Elizabeth Warren issued a report on conflicts of interest in annuity sales. Slate has a summary of the concerns, describing both the high commissions and additional perks for those selling.

At the heart of the controversy is a public expectation of a fiduciary interest on the part of the sales rep.

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. Think of The Lone Ranger. No award this week, despite the abundance of really bad analysis. I am thinking of starting a nominee section. This would include items that have obvious errors but which have not attracted any replies or refutation. Almost any two-variable chart these days is a candidate.

Quant Corner

Whether a trader or an investor, you need to understand risk. I monitor many quantitative reports and highlight the best methods in this weekly update. For more information on each source, check here.

Recent Expert Commentary on Recession Odds and Market Trends

Bob Dieli does a monthly update (subscription required) after the employment report and also a monthly overview analysis. He follows many concurrent indicators to supplement our featured “C Score.”

Georg Vrba: An array of interesting systems. Check out his site for the full story. We especially like hisunemployment rate recession indicator, confirming that there is no recession signal. He gets a similar result from the Business Cycle Indicator, updated this week.

Doug Short: Provides an array of important economic updates including the best charts around. One of these is monitoring the ECRI’s business cycle analysis, as his associate Jill Mislinski does in this week’s update. The ECRI story is becoming repetitive and even more unhelpful. It seems too related to commodity prices, and only slightly changed from their failed recession forecast. It would be refreshing to see them do a complete reset and adopt a fresh approach.

RecessionAlert: A variety of strong quantitative indicators for both economic and market analysis. While we feature the recession analysis, Dwaine also has a number of interesting systems. These include approaches helpful in both economic and market timing. He has been very accurate in helping people to stay on the right side of the market.

This week Dwaine highlights a recession “warning” (next September) from his proprietary indicators. Since these have not yet been tested in real time, he recommends a watchful approach before making an official forecast. Read the entire story here.

New Deal Democrat updates a number of long-leading indicators, suggesting no recession before next year’s election. See the full post for analysis.

It is time for another update of Doug Short’s excellent Big Four series, where he tracks the most important indicators used by the NBER in recession dating. Check out the full post for detailed analysis of each component.

The Week Ahead

It is a moderate week for economic data. While I highlight the most important items, you can get an excellent comprehensive listing at Investing.com. You can filter for country, type of report, and other factors.

The “A List” includes the following:

- Retail sales (F). Gasoline savings getting spent?

- Michigan sentiment (F). Good read on employment and spending.

- Initial claims (Th). Fastest and most accurate update on job losses.

- JOLTS report (Th). Getting more attention as an indicator of labor market tightness.

The “B List” includes the following:

- Wholesale inventories (T). September data, but relevant to final Q3 GDP.

- Business inventories (F). More GDP impact from September data.

- PPI (F). Will not have much significance until there are a few hot months.

- Crude oil inventories (Th). Focus on oil prices keeps this report in the spotlight.

This may be a record week for FedSpeak with at least one person taking a rostrum every day. Expect each appearance to be parsed for a validation of the new expectation of a December rate hike.

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a “one size fits all” approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

Insight for Traders

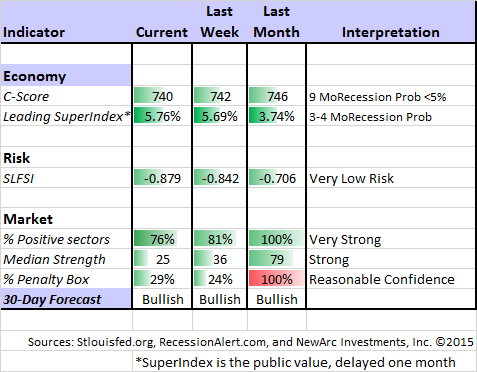

Felix has remained bullish, and we increased our commitment accordingly. The penalty box indicator remains relatively low, increasing our confidence in the multi-week bullish call. For more information, I have posted a further description — Meet Felix and Oscar. You can sign up for Felix’s weekly ratings updates via email to etf at newarc dot com. Felix appears almost every day at Scutify.

Dr. Brett Steenbarger continues to “bring it” for traders – post after post. This week he has two great articles. One shares his experience in hiring traders for prop firms and hedge funds. He notes two important predictors of success: originality and flexibility.

In the second he emphasizes the importance of intuition – when it works, and when it doesn’t. This counters some recent stories about experts, but I think it is correct and deserving of more study.

Insight for Investors

I review the themes here each week and refresh when needed. For investors, as we would expect, the key ideas may stay on the list longer than the updates for traders. Major market declines occur after business cycle peaks, sparked by severely declining earnings. Our methods are focused on limiting this risk. Start with our Tips for Individual Investors and follow the links.

We also have a page summarizing many of the current investor fears. If you read something scary, this is a good place to do some fact checking.

Other Advice

Here is our collection of great investor advice for this week.

If I had to pick a single most important article, it would be the KraneShares post, A Tale of Two Chinas. The story of China weakness, with overemphasis on manufacturing, has diminished over the last few weeks. Partly this is because more seem to understand the implications of the changing emphasis in the Chinese economy. This has been crucial in the shift in investor attitudes about the global economy and recession odds.

Many China indices have not kept pace with China’s shifting economy and still have heavy concentrations in China’s manufacturing industries. Additionally, many news reports continue to view China’s declining manufacturing numbers as a holistic representation of its entire economy. We believe this thinking was partially responsible for the rise in correlation between traditional sectors and “new China” sectors of China’s economy over the summer. Many investors turned indiscriminately averse to China, which detracted from the stock performance of companies that were otherwise growing healthily.

See the full article for charts and more details.

Stock Ideas

Chuck Carnevale’s most recent post for retirement investors is valuable for everyone. He highlights attractive undervalued stocks in the defense sector, attractive and less attractive names in health care, and explains the need for patience when taking a value approach. There are plenty of ideas, charts, and great explanations.

Jack Hough at Barrons.com has some ideas for cheap alternatives to the market-leading FANG stocks. We own two of the three.

Watch out for….

Hedge funds – – most not doing well. (Eqira).

Bitcoin – Jamie Dimon says that governments will crack down. (Fortune)

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for ten year. The average investor should make time (even if not able to read every day as I do) for a weekly trip on Wednesday. Tadas always has first-rate links for investors in this special edition. As always, there are several great links, but I especially liked this explanation of why you should keep stock market apps off your phone. Hint: Frequent monitoring is likely to reduce your performance via “myopic loss aversion.”

There is a reason why brokerage firms make trading easy and accessible. And you are not really going to get a visit from Kevin Spacey.

Are you a baby boomer? Kate Davidson at the WSJ has a good explanation of the savings gap facing potential retirees. This chart tells the basic story.

Value Investing

Eddy Elfenbein comments on the continuing lag in the value investing approach. With a bow to some academic opinion, he suggests that a lingering 2008 effect on financial index may be spilling over to many of these names. If so, a rising interest rate regime may be positive for these names.

Alpha Architect takes up a similar theme, citing (as usual) some good academic work and concrete examples. Hint: In the long run, three years of lagging performance from a strong method means little. For investor, especially those getting older, it causes them to lose confidence.

Economic Outlook

Neil Irwin (The Upshot at the NYT) conducts an interesting debate – with himself! He raises and responds to the important current economic arguments. He acknowledges and responds to the key worries. Whether you agree or not, it is a good summary of the issues.

Market Outlook

Cullen Roche opines that the bull market is built upon fears of another financial crisis:

What we had early this summer was an environment in which a lot of people were convinced that 2008 was occurring all over again and sold, sold, sold. Meanwhile, the macro data in the USA wasn’t really changing all that much. Yes, many multinationals are seeing hits to their earnings thanks to weak foreign sales and the rising dollar, but much of this is an energy story. While blended earnings are down 2.2% year over year, the exclusion of energy from the S&P 500 results in a 5% increase in year over year earnings. And the energy story is hardly surprising to anyone at this point. It was priced into energy stocks as oil prices cratered last year.

Callum Thomas charts the story.

Final Thoughts

Friday’s trading provides some clues to the likely reaction of various markets. Here are my (tentative) conclusions.

- The impact on the overall market averages will be modest and perhaps positive. (JP Morgan via MarketWatch)

- Bonds will (finally) weaken.

- Sector impacts will be significant – bad for utilities, modestly bad for other “dividend” stocks, modestly negative for biotechs and story stocks, and good for banks.

- U.S. companies heavily reliant on exports will be hurt by a stronger dollar. So will companies making much of their revenue in foreign currencies. The question is whether the dollar will stabilize or continue to strengthen.

- Emerging markets will have slightly more competition for investments.

But we should not get carried away. There were significant market reactions on Friday, and the path of increases is likely to be long and shallow. There is plenty of time to adjust positions.

Two weeks ago I stated my contrarian opinion that a December policy shift was still possible, but not important for long-term investors. I expected more of a knee-jerk negative reaction, but the market seems to have been prepared.

Investment Ideas

Rates will increase gradually and in line with economic strength. This suggests banks (I prefer the regional banks versus money center names), technology stocks with reasonable growth, and cyclical stocks priced as if a recession is imminent. Homebuilders will eventually be affected by higher rates, but the prices allow plenty of room to run.

We own stocks in all of these sectors.