KEY TAKEAWAYS

· European earnings have disappointed relative to expectations and may suggest tempering near-term expectations for European stocks.

· While we are encouraged by Japan’s economic progress, its earnings season has also fallen short of expectations.

· We recommend suitable investors focus equity allocations in the U.S., while maintaining modest developed international equity exposure.

Earnings overseas have generally not kept up with the U.S. We spend a lot of time dissecting earnings season in the U.S. because we believe earnings are the single biggest driver of stock prices over the long run. But earnings are not just important for U.S. stocks, they are also important for stocks overseas. This week we provide an earnings update in Europe and Japan, where results thus far have mostly fallen short of those in the U.S. While we continue to focus our equity allocations in the U.S., we still recommend modest developed international equity exposure for suitable investors, despite third quarter 2015 earnings shortfalls overseas. Prospects for international earnings to improve over the rest of 2015 and into 2016, and for additional monetary stimulus, are supportive.

The Source:

Earnings figures may vary depending on the source (Thomson, FactSet, Bloomberg, etc.). Data providers have different methodologies for calculating earnings, and different interpretations of what constitutes operating earnings as compared with reported (GAAP) earnings. In general, we favor the Thomson data series’ long history in the U.S., but view FactSet as a reliable source of international earnings data.

U.S. EARNINGS SEASON TRACKING ACCORDING TO PLAN

We wrote about third quarter 2015 earnings season in the U.S. in our recent Weekly Market Commentary, “Corporate Beige Book,” where we compared the number of positive words relative to the number of negative words in earnings conference call transcripts to assess the mood of management teams discussing results. Despite the challenging environment, particularly for global companies impacted by the strong U.S. dollar and companies tied to commodities, moods were generally positive. That exercise also highlighted the increased attention on China.

Earnings season in the U.S. is about 90% complete, ahead of Europe (51%) and Japan (73%), so we have a near final picture of where the numbers will end up. Results relative to expectations have been very good, with a 5% upside surprise thus far for S&P 500 earnings; and excluding the energy sector, earnings are on track to grow at a solid 6% pace. Excluding the drag from currency due to the strong U.S. dollar, earnings would be on track for a near 9% year-over-year increase, a very respectable figure for this stage of the economic cycle. U.S. earnings are poised to accelerate during the fourth quarter of 2015 and potentially return to mid- to high-single-digit growth rates within the next several quarters.

EUROPE DISAPPOINTS

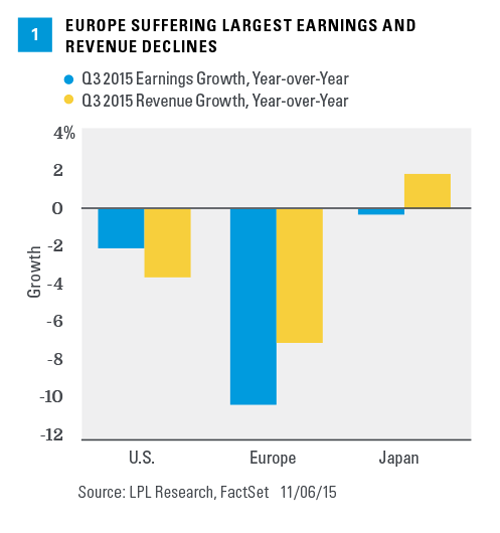

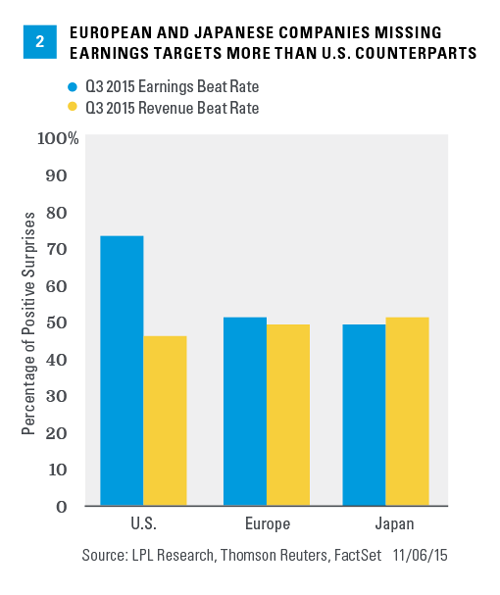

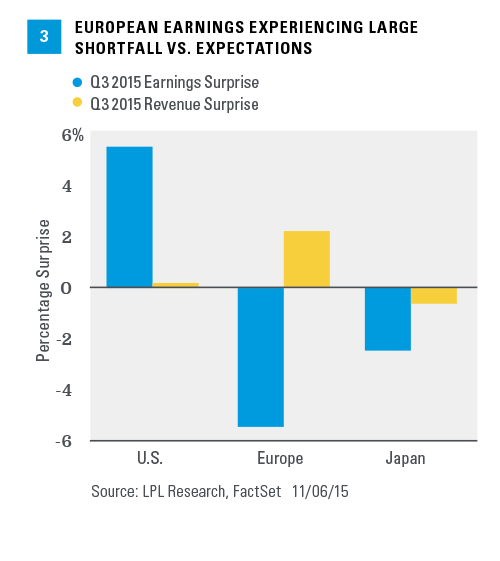

In Europe, where the third quarter 2015 reporting season is only about halfway complete, results thus far have been disappointing on a variety of metrics. First, based on MSCI indexes, Europe has suffered the biggest year-over-year decline in earnings and revenue compared with the U.S. and Japan [Figure 1]. The story is no different if the sharp declines in energy sector profits are excluded. Second, the earnings beat rate (percent of companies beating earnings estimates) at 50% is significantly lower than the 70%-plus rate in the U.S. (and in-line with Japan’s rate) [Figure 2]. And third, the earnings surprise, at a 5% shortfall, is far worse than the 5% upside surprise to earnings in the U.S. thus far and worse than the 2% shortfall in Japan [Figure 3]. The only metric in which Europe compares favorably to the U.S. and Japan is the revenue surprise (+2%), which is better than the U.S. result and Japan’s 1% shortfall.

These results are discouraging for several reasons. For one, Europe has a currency advantage relative to the U.S. The drag from a strong U.S. dollar that U.S.-based multinationals are experiencing benefits European multinationals selling into the U.S. Second, European economic data have been consistent with steady growth in recent months, providing a backdrop for revenue and earnings gains. Third, the earnings weakness has left European valuations less attractive, weakening a key support for European stocks. Based on FactSet consensus estimates, since June 30, 2015, expected European earnings growth for 2016 has been cut in half to below 8%, a larger reduction than the U.S. (14% to 9%) and Japan (13% to 11%) during the same time frame. Lower European earnings estimates have lifted the forward price-to-earnings ratios (PE), leaving Europe at an 8% discount to the U.S., about in-line with its long-term average.

After warming up to European stocks during the early part of 2015, disappointing earnings results and mixed recent performance for these markets may suggest tempering near-term enthusiasm. Still, in general we recommend modest allocations to the region for suitable investors, with a preference for currency-hedged exposure when possible, due to the risk of further U.S. dollar gains as the Federal Reserve (Fed) likely begins to hike rates in December. We continue to see potential additional stimulus by the European Central Bank (ECB) as a positive catalyst, as discussed in this week’s Weekly Economic Commentary, and expect European earnings growth to potentially improve in the coming quarters as benefits of low oil prices and cheaper currencies continue.

JAPAN ALSO TAKES A STEP BACK

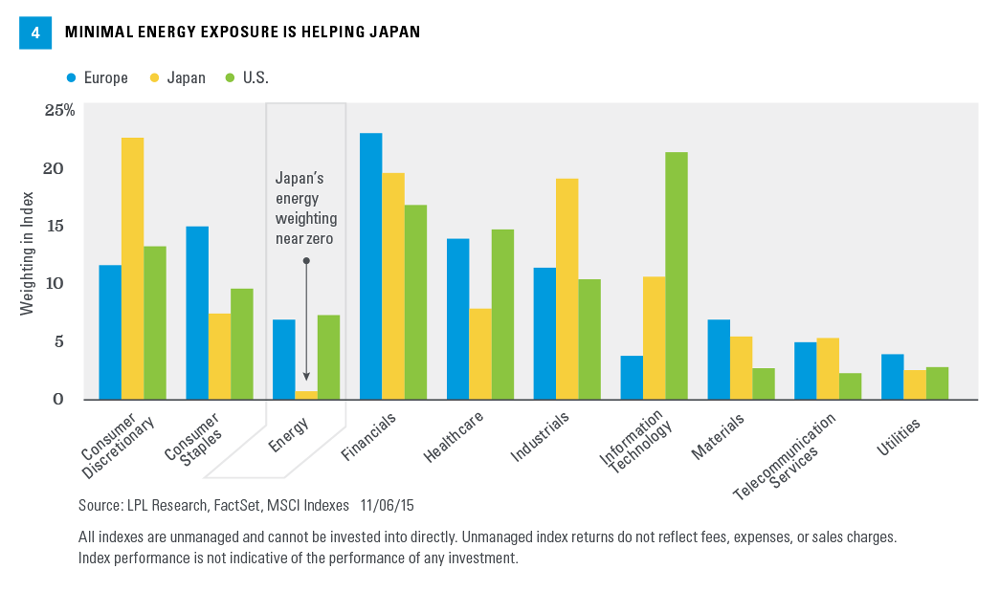

Japan’s third quarter 2015 results also took a step back from prior quarters and have mostly disappointed relative to expectations as shown in Figures 2 and 3. The good news for Japan right now is its market’s limited energy exposure at less than 1% of the MSCI Japan Index [Figure 4], because Japan is a big fuel importer and not a producer. The absence of an energy drag has enabled Japanese companies to produce flat earnings year over year — very respectable relative to the U.S. and Europe — and actually grow revenue at about a 2% clip. Still, the beat rates have been disappointing and overall results have fallen short of expectations, leading to downward revisions in Japan, though smaller than those in the U.S. and Europe.

As in Europe, Japanese companies should benefit from a weaker currency (partly a result of stimulus enacted by the Bank of Japan), but those benefits have not been readily apparent. Low fuel prices should provide a nice boost to the Japanese economy. But economic growth in Japan has been intermittent, leading to speculation that more stimulus is forthcoming. And although the MSCI Japan Index has virtually no energy companies, its heavy weighting in industrials carries indirect commodity exposure, 19% of its exports go to China — more than double the U.S., and its materials sector weighting, at 5.5%, is larger than that of the S&P 500.

We have been encouraged by recent progress in Japan. Monetary policy stimulus — with more likely on the way — is supportive of the Japanese stock market. A weaker yen currency should help Japanese exporters, which are a bigger driver of the Japanese economy and a bigger component of its stock market than in the U.S. And low fuel prices are especially helpful for corporate Japan. Although economic growth has been choppy and earnings have fallen short of expectations during the third quarter, we continue to see brightening prospects for Japanese earnings and Japanese stocks over the rest of 2015 and into 2016.

CONCLUSION

Third quarter earnings season has generally met expectations in the U.S. but fallen short in Europe and Japan. After warming up to European stocks during the early part of 2015, disappointing earnings results and mixed recent performance for these markets may suggest tempering near-term enthusiasm. In Japan, although economic growth has been choppy and earnings have fallen short of expectations during the third quarter, we continue to see brightening prospects for Japanese earnings and stocks. We recommend suitable investors focus equity allocations in the U.S. while maintaining modest developed international equity allocations where appropriate.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

All investing involves risk including loss of principal.

Investing in foreign and emerging markets securities involves special additional risks. These risks include, but are not limited to, currency risk, geopolitical risk, and risk associated with varying accounting standards. Investing in emerging markets may accentuate these risks.

Because of its narrow focus, specialty sector investing, such as healthcare, financials, or energy, will be subject to greater volatility than investing more broadly across many sectors and companies.

Currency risk is a form of risk that arises from the change in price of one currency against another. Whenever investors or companies have assets or business operations across national borders, they face currency risk if their positions are not hedged.

Commodity-linked investments may be more volatile and less liquid than the underlying instruments or measures, and their value may be affected by the performance of the overall commodities baskets as well as weather, geopolitical events, and regulatory developments.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The MSCI Japan Index is a free float-adjusted, market capitalization-weighted index that is designed to track the equity market performance of Japanese securities listed on Tokyo Stock Exchange, Osaka Stock Exchange, JASDAQ, and Nagoya Stock Exchange.

DEFINITIONS

Forward price-to-earnings is a measure of the price-to-earnings ratio (PE) using forecasted earnings for the PE calculation. While the earnings used are just an estimate and are not as reliable as current earnings data, there is still benefit in estimated PE analysis. The forecasted earnings used in the formula can either be for the next 12 months or for the next full-year fiscal period.

(c) LPL Financial