Is the Selloff in High-Yield Bonds Warranted?

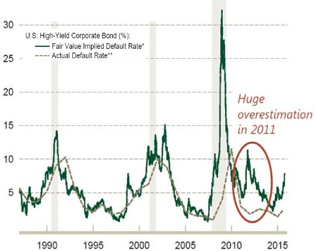

It’s been a familiar pattern over the past several years. A global growth scare leads investors to flee the high-yield bond asset class in droves, resulting in a spread widening, negative short-term returns and an overestimation of default risk. Looking back at 2011, during the third quarter high-yield bonds (BofA Merrill Lynch U.S. High Yield Master II index) posted a total return of -6.3% on fears of a double dip recession in Europe and the possibility of a technical default by the U.S. government facing a shutdown. Spreads widened to 800 basis points, implying default rates over 10%. When reality set in and worst-case scenarios faded, defaults averaged less than 3%, spreads compressed and high-yield bonds finished at +4.4% in 2011 (+6.2% in the fourth quarter) and +15.6% in 2012.

Investors Have Overestimated Default Risk Since The Crisis

*Assumes a 2% risk premium and recovery rate of 40%; sources: BofA Merrill Lynch and MRB calculations **Sources; Standard & Poor’s series shown thereafter

Note: Shaded for NBER (National Bureau of Economic Research) - designated recessions

Fast forward to 2015 and fears of a global growth scare are here again, led by China and a bear market in commodities. Again, outflows have followed as high-yield bond ETFs (exchange-traded fund) and mutual funds shed $3.9 billion over the last 13 weeks. This has resulted in the spread widening to 600 basis points, third-quarter returns of -4.9% and implied default rates in the 6%–7% range for ex-energy issues. Default rates of this magnitude would likely imply a recession, though in our view the U.S. economy is a long way from signaling one is on the horizon. Default rates have picked up recently, but rose to just 2.6% (annualized) in September.

This selloff leaves the broad high-yield market with a yield of 8%, which masks the bifurcation between commodity-linked sectors yielding 9%–14% and the broader asset class yielding 7%. This yield looks attractive when compared to Treasurys, particularly with a looming Federal Reserve rate hike. A hike would signal an economy strong enough to handle policy normalization, muted defaults and spread narrowing. Treasurys currently offer only a small income cushion given near-record-low starting yields. In contrast, high-yield bonds have averaged about 6% in annualized returns over the past five years, and that type of return is still possible looking out over the next couple years.

The spread between high-yield bonds and Treasurys has widened by more than 1% in the last quarter. Collecting income at a rate four times that of Treasurys should reward patient, value-focused investors over the next 12 to 18 months.

Unless otherwise noted, all data is as of the date of publication.

BMO Asset Management Corp. is the investment advisor to the BMO Funds. BMO Investment Distributors, LLC is the distributor. Member FINRA/SIPC. Past performance does not guarantee future results.

BMO Global Asset Management is the brand name for various affiliated entities of BMO Financial Group that provide investment management and trust and custody services. Certain of the products and services offered under the brand name BMO Global Asset Management are designed specifically for various categories of investors in a number of different countries and regions and may not be available to all investors. Those products and services are only offered to such investors in those countries and regions in accordance with applicable laws and regulations. BMO Financial Group is a service mark of Bank of Montreal (BMO).

BMO Asset Management Corp., BMO Investment Distributors, LLC, BMO Private Bank, BMO Harris Bank N.A. and BMO Harris Financial Advisors, Inc. are affiliated companies. BMO Private Bank is a brand name used in the United States by BMO Harris Bank N.A. BMO Harris Financial Advisors, Inc. is a member FINRA/SIPC, an SEC registered investment adviser and offers investments, advisory services and insurance products. Not all products and services are available in every state and/or location.

This is not intended to serve as a complete analysis of every material fact regarding any company, industry or security. The opinions expressed here reflect our judgment at this date and are subject to change. Information has been obtained from sources we consider to be reliable, but we cannot guarantee the accuracy. This publication is prepared for general information only. This material does not constitute investment advice and is not intended as an endorsement of any specific investment. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. Investors should seek advice regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investment involves risk. Market conditions and trends will fluctuate. The value of an investment as well as income associated with investments may rise or fall. Accordingly, investors may receive back less than originally invested. Past performance is not necessarily a guide to future performance.

Securities, investment advisory and insurance products are: NOT FDIC INSURED — NO BANK GUARANTEE — MAY LOSE VALUE.

© 2015 BMO Financial Corp.