Life in a No Growth World and the Impact on Interest Rates

The recent Fed decision seems to provide no more clarity: they left the opening for a December hike but didn’t specifically commit to making a move then. So the question remains, when will the Fed begin raising rates and by how much? It is clear they want to start increasing rates in order to give themselves some flexibility if they need it down the road, all the while fulfilling their dual mandate. However, it seems the “data” for our “data dependent” Fed isn’t getting better globally.

What has become apparent to markets over the past few months is that we are in a no growth world. China is slowing, Europe continues to muddle along with Germany most recently showing signs of strain while various emerging markets are deteriorating, acerbated by the collapse in commodity prices. It seems that the US is the only engine that is firing to any extent, and even here we aren’t firing on all engines. Looking at data, be it the ISM number or jobs report more recently, the global weakness is having an impact here domestically, especially given this economic cycle has already been characterized by a very lackluster recovery to begin with. While we don’t expect this will trigger a recession here at home, the reality we all must face is that we are in a no growth world. So what does that mean for interest rates?

Even before the recent bout of data weakness, we have been big believers that any move the Fed makes on the interest rate front will be slow and moderate. While we feel the ultimate start date is irrelevant, markets are split as to whether that is December or is pushed out to 2016. No matter when they start, for various reasons we don’t foresee a spike in the 5- and 10-year Treasury rates, the more relevant rates for markets (rather than the Federal Funds Rate that the Fed actually controls).

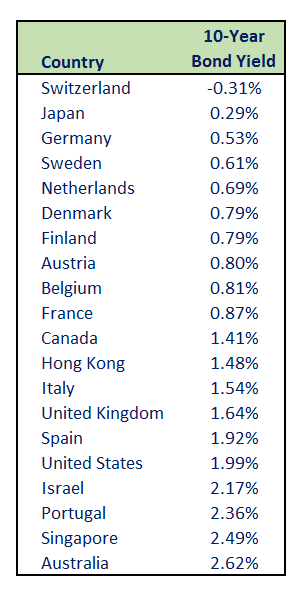

Above and beyond the fact we are mired in a no growth world, inflation is another data point the Fed continually cites and so far has seemed to be a factor in delaying their move. With the recent decline in oil and many other commodities, we don’t see any near-term inflation pressures. Because of this, along with a generally weak demand for products, we expect the Fed will be hard-pressed to get to their target inflation number of 2%, even in the “medium term” as they discussed in the recent statement. With the lack of inflation globally, 10-year sovereign bond rates across the globe are exceedingly low.

The US is an outlier with our 10-year at just over 2%. Even countries that were on the precipice not too long ago, like Italy and Spain, have 10-year bond yields about the same or under that of the US.1 We see this as yet another reason that even if the Fed starts increasing the Federal Funds Rate, we don’t see that translating to big moves in the 5- and 10-year Treasury rates, as we would expect buyers to step in, constraining rates on US Treasuries.

Some additional factors to keep in mind as we assess the likelihood of a spike in rates:

- Unemployment—while the headline unemployment number has improved, workforce participation has not, and we know this is something the Fed pays attention to based on previous comments.

- Wages—we are also not seeing any meaningful improvement in wages, which will hamper growth in consumer spending.

- Consumer spending—approximately two-thirds of economic activity is consumer driven. With nearly 50% of Americans now on some form of government assistance and the massive number of people that have fallen out of the job market, there is much less spending power today than a decade ago. Many have said that the energy cost savings will spur consumer spending but that just isn’t playing out as money is being used to shore up other cost increases.

- Dollar—the strong dollar continues to cut into corporate profits, manufacturing, and exports, as witnessed by the recent ISM data and reported corporate earnings by the large multinationals.

Given the large portion of under-employed/people dropping out of the workforce, curtailed consumer spending, and an appreciating dollar, we believe expectations to get back to a 4% – 5% growth rate are unrealistic, and with a lack of strong economic growth, we believe the Fed will be hindered in how aggressive they can be in raising rates.

On a final note, it is important to recognize the recent activity in Treasury prices. The Treasury markets aren’t reacting to the rising rate talk, with the 10-year going from 2.35% to 2.06% during the third quarter2 and down a full percent since early 2014, and only popped to 2.10% following the Fed’s comments that seemingly opened the door for a December hike3. 3-month T-Bills were recently issued at a 0% yield. It seems these buyers have no expectation of a near-term spike in rates. The Treasury markets are telling us something: the world is weak and the Fed will do very little, if anything. With the data like the recent jobs number, we wouldn’t be surprised to see the 10-year revisit the 2015 lows.

Even if we don’t expect the Fed to aggressively raise rates, like it or not, the prospect of higher interest rates is on the mind of many investors. The talking heads in the financial media keep jumping to the conclusion that if interest rates are going up, this is bad for bonds, including high yield bonds. For much of the “bond” market, such as longer duration municipal or investment grade bonds, this will likely be true; however, for the high yield bond market this assumption is perplexing, given that the high yield market’s history tells us a different story. Looking back at over 30 years of data, the high yield market has performed well in periods of rising rates, especially relative to other fixed income asset classes:4

Not only has the high yield market posted an average return of 13.6% in the 15 calendar years during which we saw rates rise over the annual period since 1980, but it has had only one down year over this time frame. Rates generally go up during periods of economic growth which is generally favorable for corporate credit. So what happens if we are wrong and the economy strengthens significantly, and rates along with it? Well history would indicate high yield investors are in one of the better asset classes for that scenario.

The Federal Reserve may start raising rates this year or next to get the ball rolling, and may move rates up a quarter of a point a few times over the next year, but we expect their move to be fairly minimal and largely be irrelevant for the high yield market. We may even see the financial markets move up on an actual rate move as it removes the uncertainty. For all of the talk of a hit to high yield, we don’t expect a moderate rate move to have a meaningful impact. For rates to really accelerate, we need to see much stronger global growth, which again would be a positive for corporate credit in terms of lowering the already low default rate risk as income and cash flow improved.

Anyone who is avoiding the high yield asset class due to a potential rate increase or waiting until we see what the Fed does, or even attempting to time a bottom, is missing what we see as a great opportunity to generate yield. With many now expecting that we don’t see a rate move until March of 2016, almost six months away, and a high yield index now yielding around 8%5, you would miss about 4% of income, irrespective of any pricing upside, by sitting on the sidelines waiting for a tiny 25 bps move by the Fed.

We believe the rising rate concerns for the high yield market are overblown by the financial media and that the current spread levels offered by the space are well compensating investors for this uncertainty. For those sitting on the sidelines “waiting and seeing,” you may well miss the very attractive, tangible yield we see currently offered by the high yield debt market. For more on our thoughts about rates and the value in today’s high yield market, see our piece “Making Sense of Markets.”

1 Data as of 10/29/15, sourced from Bloomberg.

2 Daily Treasury Yield Curve Rate, source U.S. Department of Treasury, for the period 6/30/15 to 9/30/15.’

3 Daily Treasury Yield Curve Rate, source U.S. Department of Treasury, for 10/28/15.

4 High yield and investment grade data sourced from: Acciavatti, Peter Tony Linares, Nelson R. Jantzen, CFA, Rahul Sharma, and Chuanxin Li. “2008 High Yield-Annual Review,” J.P. Morgan North American High Yield Research, December 2008, p. 113; “High-Yield Market Monitor,” J.P. Morgan, January 5, 2015, p. 3; and “2014 High-Yield Annual Review,” J.P. Morgan, December 29, 2014, p. 292. Treasury data sourced from Bloomberg (US Generic Govt 5 Yr). The J.P. Morgan High Yield bond index is designed to mirror the investible universe of US dollar high-yield corporate debt market, including domestic and international issues. The J.P. Morgan Investment Grade Corporate bond index represents the investment grade US dollar denominated corporate bond market, focusing on bullet maturities paying a non-zero coupon. S&P 500 data sourced from Bloomberg. Barclays Municipal Bond Index covers the long-term, tax-exempt bond market (source Barclays Capital).

5 Acciavatti, Peter Tony Linares, Nelson Jantzen, CFA, Rahul Sharma, and Chuanxin Li. “Credit Strategy Weekly Update,” J.P. Morgan North American High Yield Research, October 2, 2015, p. 29.