Master limited partnerships (MLPs) that shuttle oil and gas around the country have sold off sharply in the past year; however, most of them are “midstream” pipeline operators with multi-year contracts at fixed rates with big refiners and utility companies, which may mitigate the effects of near-term gyrations in energy prices.

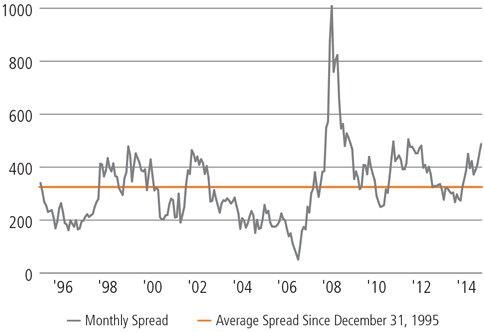

Distributions by most pipeline operators have been unaffected, but prices are significantly lower, translating into yields on MLPs that are now more than five percentage points above the 10-year Treasury yield, compared to an average premium of 3.5 percentage points over the past 10 years. What’s more, with MLPs currently trading at steep discounts to historical valuations and revenue holding steady or trending higher in many cases, we believe the group may offer opportunity for investors to earn attractive yields from consistent cash generators in the midstream pipeline business.

MLP Key Terms And Concepts

Midstream: The largest of the three MLP segments (upstream, midstream and downstream), midstream typically refers to the infrastructure or logistics segment that connects oil and gas supply to end-use markets.

General Partner (GP): The General Partner manages the MLP, usually has a percentage equity interest in the MLP and typically owns incentive distribution rights (IDRs). The IDR entitles the GP to receive a disproportionate share of its MLP’s incremental cash flow.

Limited Partner (LP): MLP limited partners provide the MLP capital and receive cash distributions.

Natural Gas Liquids (NGLs): When natural gas is extracted it typically contains a liquids stream that is separated at the wellhead. The natural gas liquids are later fractionated into their components (e.g., ethane, propane and butane).

Wet Gas vs. Dry Gas: Methane is the chief component of dry gas, which is mostly used for heating, cooling, electric power generation and, when compressed, vehicle fuel. Wet gas contains a higher percentage of valuable NGLs. Many midstream MLPs earn their margins on processing wet gas to separate these NGLs.

The Appeal of MLPs

In an era of extremely low interest rates, investors seeking higher yields are looking beyond traditional bonds to other non-traditional sources of income further out on the risk-return spectrum, such as real estate investment trusts (REITs) and MLPs. Just as REITs are “pass-through” entities for collecting rent checks from real estate, MLPs offer a similar kind of exposure to pipelines and other energy infrastructure assets that earn income from handling oil, gas and a wide spectrum of refined products.

MLPs do not pay income tax at the corporate level as long as profits are paid out as distributions to limited partners who hold “units” in the partnership and pay tax on their share of income. MLP distributions come with tax advantages, since partners also share in significant non-cash expenses that are used to reduce taxable income.

The popularity of MLPs surged over the past decade with the number of exchange-traded partnerships skyrocketing from fewer than 30 in 2000 to approximately 130 in 2015. Market returns attracted more investors. The Alerian MLP Index has produced a total return of 172% in the past 15 years, as of September 15, 2015, nearly five times the 37% gain for the S&P 500 Index over the same period.

Spread Versus Treasury Suggests Yield Opportunity

Alerian MLP Index Yield vs U.S. 10-Year Treasury Yield

Basis Point Spread: December 31, 1995 – August 31, 2015

Source: www.alerian.com; www.federalreserve.gov.

Indexes are unmanaged and are not available for direct investment. Investing entails risks, including possible loss of principal. Past performance is no guarantee of future results.

MLPs Swept up in Energy Selloff

Until recently, MLPs had not been through a prolonged period of low energy prices since 2000, so it was uncertain how returns would correlate with the cost of a barrel of crude oil during that period. Recent performance has shown a high correlation. Rough times for MLP investors commenced with the collapse in crude oil prices that began in September 2014. Since then, crude oil prices have tumbled more than 60%, and the Alerian MLP Index is lower by 30%.

MLPs prospered as U.S. oil production boomed with the use of hydraulic fracturing and other advanced drilling techniques. In our view, the market’s fear is that U.S. oil production will decline as drillers who cannot cover their costs at depressed prices will shut down production, reducing the amount of oil and gas flowing through pipelines. Over the long term, MLP revenues have had fairly low correlation to energy prices but, in the short-term, sentiment and fear relating to the weakness of upstream companies and decline in pipeline delivery have severely impacted the market value of the overall group.

Higher Rates Pose Additional Risk

MLPs have a demonstrated sensitivity to energy prices, and they are also sensitive to interest rates. Similar to other high-yielding securities like utilities, stocks and REITs, higher interest rates tend to have a negative impact on MLP prices, given that a rise in rates results in distributions being discounted at steeper rates.

Yields on the 10-year Treasury note this year rose from below 1.7% in February to as high as 2.5% in late June, a period during which the Alerian MLP Index fell by 10%. Crude oil prices actually rallied nearly 20% during this same time, illustrating the potential negative impact of higher interest rates. As rates retreated from summertime highs, crude oil began to slide again, dragging MLP indices to four-year lows.

Seek Quality and Value

Pared valuations support the idea that there could be value in the wreckage, if those cheap valuations are not an indication of deteriorating earnings. Earnings and distributions from many midstream MLPs continue to grow around 5% a year and we believe they are likely to continue. The midstream group has avoided large-scale cuts in distributions which, in our view, may demonstrate that fundamentals remain sound.

While it appears that conservatively financed pipeline operators may offer a mix of value and yield, energy prices and interest rates do pose risks. Commodity prices will likely remain volatile and rates are expected to move higher. A climb in yields that is stable and not precipitous could minimize the impact on MLPs, but if rates jump too quickly, the group could face pressure. Historically, MLPs have performed poorly at the start of a rate-hiking cycle, but returns have often improved once the hikes are under way.

MLPs: Perception Vs. Reality

Douglas A. Rachlin, Senior Portfolio Manager—The Rachlin Group

Yves C. Seigel, CFA, Portfolio Manager—The Rachlin GroupMLP prices have suffered of late due in large part to investor perception of the impact of a number of external factors. We believe these perceptions don’t align with reality—particularly in the midstream energy MLPs where we focus.

Drop in crude oil prices: Midstream energy MLP cash flow can be relatively predictable due to their “take or pay” contracts and minimum volume commitments. Further, we believe investor focus on the drop in supply (production) misses the impact of lower prices on increasing demand, as well as the anticipated growth in natural gas consumption (25% through the end of the decade).

Impact of rising rates: MLPs have the ability to outperform when rates rise; following the June 2004 rate hike, for example, the Alerian Index outperformed the S&P 500 for the remainder of the year. Our outlook is that interest rates will rise gradually and reflect a strengthening U.S. economy. While a global economic slowdown has negative implications for commodity prices and energy consumption on the margin, in our view, the U.S. economy appears resilient and secular U.S. natural gas demand growth is highly visible.

Access to capital: Concerns have been rising regarding MLPs’ ability to access capital to finance infrastructure investment opportunities. MLPs traditionally finance growth projects with both debt and equity. Unlike in 2008, the debt market remains open and the cost of debt is still relatively low. The equity market is challenging, but not closed. We believe the blended cost of capital, while higher than a year ago, can still support good projects that generate attractive returns for well-capitalized MLPs.

We view the current market malaise as temporary, albeit painful and, as in 2008 – 2009, we anticipate a healthy—and perhaps quick—recovery when it happens. Further, we think sentiment is overly bearish and long-term investors seeking income and growth are likely to be rewarded by staying the course.

Master Limited Partnerships (MLPs) are limited partnerships that are publicly traded and which have the tax benefits of a limited partnership and the liquidity of a publicly traded company. As an income-producing investment, MLPs could be affected by increases in interest rates and inflation. This material is not intended as tax advice. The tax situation of each client is unique and a client should consult his/her own tax advisors for the specifics of his/her tax treatment.

This material is provided for informational purposes only. Nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. The views expressed herein are generally those of Neuberger Berman’s Investment Strategy Group (ISG), which analyzes market and economic indicators to develop asset allocation strategies. ISG consists of investment professionals who consult regularly with portfolio managers and investment officers across the firm. This material may include estimates, outlooks, projections and other “forward-looking statements.” Due to a variety of factors, actual events may differ significantly from those presented.

Any views or opinions expressed may not reflect those of the firm as a whole. Information is obtained from sources deemed reliable, but there is no representation or warranty as to its accuracy, completeness or reliability. All information is current as of the date of this material and is subject to change without notice. Third-party economic or market estimates discussed herein may or may not be realized and no opinion or representation is being given regarding such estimates. Certain products and services may not be available in all jurisdictions or to all client types. Indexes are unmanaged and are not available for direct investment. Unless otherwise indicated, returns shown reflect reinvestment of any dividends and distributions. Investing entails risks, including possible loss of principal. Past performance is no guarantee of future results.

This material is being issued on a limited basis through various global subsidiaries and affiliates of Neuberger Berman Group LLC. Please visit www.nb.com/disclosure-global-communications for the specific entities and jurisdictional limitations and restrictions.

The “Neuberger Berman” name and logo are registered service marks of Neuberger Berman Group LLC.