Executive Summary

· A mismatch between supply and demand is making for a stubborn bear market in Energy

· Tighter lending standards may create a solution to oversupply

· Low costs, greater efficiency, and strong balance sheets are likely to be make or break factors for Energy companies

More than 12 months into the oil slump, the picture for Energy remains unsettled. Reactions to each new supply and demand data point result in swift, outsized swings in stock prices. Volatility is affecting strong and weak companies alike. For every debt-ridden, poorly managed company that has seen its share price drop by double digits, there has been a well-managed, stable firm that has fallen in sympathy.

Now, a year into the correction, the current situation begs the question why does the struggle continue? The supply and demand imbalance that started the rout in the second half of 2014, has proven hard to fix, as illustrated. Domestic drillers have tried to rein in production by idling wells, but OPEC continues to keep bringing supply to the surface in an effort to maintain market share. Similarly, when crude prices edged higher earlier this year, U.S. producers brought some capacity back online and oversupply returned as a headwind.

Bankers May Hold the Key

With producers unwilling to make meaningful cuts in supply, and prospects for a sharp uptick in demand dim in the near-term, we believe rationality for the industry may return only after some weaker companies are forced to sell or go bankrupt.

Lenders have enabled the situation to go on but may force some discipline on the market. Approximately every six months, companies go through a so-called redetermination with their creditors where oil and gas reserves used for collateral are assigned a value as part of the process of renewing lines of credit. During the round that took place this fall, valuations were left unchanged from April. The move gave many exploration and production (E&P) companies a financial lifeline, but we believe the process may be more difficult. If companies that are already late on their loan payments start to default on loans due to depressed energy prices, banks are likely to use more conservative valuations in determining future credit lines.

The Approach We’re Taking

The tenuous financial condition for the Sector has led us to put a greater emphasis on balance sheet analysis when examining stocks in the space.

With a challenging lending environment likely on the horizon, we believe low-debt companies will be better positioned to maintain operations. Additionally, as debt funding becomes more difficult for highly levered players, cash-rich companies could make acquisitions of assets at significant discounts from those in need of capital to survive.

Location Matters

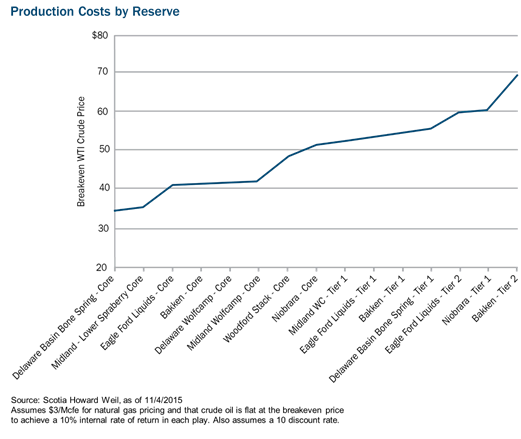

With supply projected to outpace demand until at least the second half of 2016, a sustained recovery in the price of crude may not take place for several months or more. To mitigate the impact of a soft market, we’re focusing our efforts on low cost producers. One of the factors we consider is the location of a company’s reserves. Reserves from the Eagle Ford basin, as illustrated, can be brought to market at lower costs than elsewhere. For natural gas, production is less expensive from the Marcellus and Utica reserves. The differential among energy fields can be a make or break factor when oil is hovering in the $40-plus range and natural gas is just above $2.00 per British Thermal Unit.

Beyond Production

We’ve attempted to diversify some of our risk by holding names that are less tied to prices of the underlying commodity. Scorpio Tankers Inc. (STNG), is an example of our effort to mitigate the volatility within Energy by limiting direct exposure to pricing of the underlying commodity. Because its revenues are based on shipping day rates, its prospects are more directly related to tanker capacity and transporting.

Cost Effective and Efficient

Equipment and Services names may also provide some insulation from the fluctuations in energy prices. When companies eventually ease back into the role of increasing supply, they are likely to pursue the sources of production that can be tapped at the lowest cost. In many cases, that will be wells that are already drilled but not yet producing crude. Other companies in the space are focused on improving efficiency of production.

This year we initiated a position in a producer of ceramic coated particles that are used to stimulate production in newly created wells. The company is financially sound with low debt, is attractively valued and we view the management team as a strength. Its products allow for greater volume to be pumped out of a reserve. Until the sell-off in Energy, we were unable to buy the stock due to the premium it commanded. As emotion started to take hold and shares sold off, we were able to buy a stake in what we believe will be a long-term success story.

Cause for Optimism

As bottom-up stock pickers we are not in the business of calling floors or ceilings to any market or commodity. However, the nature of the current downturn and production dynamics of shale drilling give us confidence that volatility is likely to give way to a recovery that will benefit some of the types of companies we own.

As previously noted, supply has been the source for economic imbalance and a driving force in falling prices. After domestic production bottomed in 2005 at just more than 4 million barrels per day, it has steadily climbed and stood at nearly 10 million barrels by the end of 2014. With production outpacing demand growth, fears of a glut quickly emerged.

Shortly after the cost of a barrel of crude fell below the $50 mark, domestic producers pivoted to a defensive posture and mothballed hundreds of rigs in a matter of weeks. As the chart below illustrates, this dropped the number in operation to the lowest level in over five years and points to a decrease in supply in the months ahead.

Adding to the likelihood that crude surplus will continue to shrink is the profile of many of the wells in the U.S. Decline rates vary by drill site and even among rigs tapping into the same deposit, but a commonly used rule of thumb is that barrels produced at a given well at a shale reservoir can drop by as much as 70% in the first year alone and decline 30% during the second year. The upshot is that as energy producers stand on the sidelines waiting out the recent surge in reserves, the amount of barrels produced by each existing well will continue to decline and the supply imbalance could narrow.

Making an Investment—Not a Call

We are well aware that resurgence in energy prices is not a foregone conclusion and risks, ranging from geopolitical to an unanticipated shock to demand, exist. We also acknowledge it’s unclear how long it will take for Energy to regain its footing, even in light of some of the developments that have taken place among suppliers.

Our focus has primarily been on names with exceptional balance sheets that will help them weather a prolonged deterioration in the market. We believe cash-rich firms will also be well positioned to meet growth needs when prices and production eventually ramp up.

Instead of venturing to predict the bottom in the oil market or what the price of a barrel will be next week or next year, we are focusing our bottom-up stock research on identifying well-managed, undervalued companies that should benefit the most when improved energy prices take hold—whether it be in six months or longer. By applying our 10 Principles of Value Investing™ to equities in a variety of industries, we believe we can find these companies before their value is fully recognized.

Disclosure:

Past performance does not guarantee future results.

Investing involves risk, including the potential loss of principal. Value investments are subject to the risk that their intrinsic values may not be recognized by the broad market.

Economic predictions are based on estimates and are subject to change.

The statements and opinions expressed in this article are those of the author. Any discussion of investments and investment strategies represents the portfolio managers’ views when presented, and are subject to change without notice. The opinions expressed are for general information only and are not intended to provide specific advice or recommendations for any individual.

The specific securities discussed, which are intended to illustrate the adviser’s investment style, do not represent all of the securities purchased, sold, or recommended by the adviser for client accounts and the reader should not assume that an investment in these securities was or would be profitable in the future. Certain security valuations and forward estimates are based on Heartland Advisors’ calculations. Any forecasts may not prove to be true.

As of September 30, 2015, Heartland Advisors on behalf of its clients held approximately 1.35% of the total shares outstanding of Scorpio Tankers, Inc. Statements regarding securities are not recommendations to buy or sell. Portfolio holdings are subject to change. Current and future holdings are subject to risk.

Sector and Industry classifications as determined by Heartland Advisors may reference data from sources such as FactSet Research Systems, Inc. or the Global Industry Classification Codes (GICS) developed by Standard & Poor’s and Morgan Stanley Capital International.

Definitions: 10 Principles of Value Investing™ consist of the following criteria for selecting securities: (1) catalyst for recognition; (2) low price in relation to earnings; (3) low price in relation to cash flow; (4) low price in relation to book value; (5) financial soundness; (6) positive earnings dynamics; (7) sound business strategy; (8) capable management and insider ownership; (9) value of company; and (10) positive technical analysis. Baker Hughes Rotary Rig Count: includes only those rigs that are significant consumers of oil field services and supplies and does not include cable tool rigs, very small truck mounted rigs or rigs that can operate without a permit. Non-rotary rigs may be included in the count based on how they are employed. To be counted as active a rig must be on location and be drilling. A rig is considered active from the moment the well is “spudded” until it reaches target depth. Rigs that are in transit from one location to another, rigging up, or being used in other non-drilling activities are not counted as active. Bbl: is an abbreviation for oilfield barrel, a volume of 42 U.S. gallons. Discount rate: has a specific meaning in the realm of the Energy sector. It is used to convert future values to present values in calculations of the value of oil and gas reserves. Mcfe: is an abbreviation for 1,000 cubic feet equivalent. It is determined using the ratio of six Mcf of natural gas to one Bbl of crude oil, condensate, or natural gas liquids. British Thermal Unit: is a standard unit of energy. It is the amount of thermal energy necessary to raise the temperature of one pound of pure liquid water by one degree Fahrenheit. Cushing Spot Price: is the current price at which a barrel of West Texas Intermediate oil for delivery at the energy hub in Cushing, Oklahoma can be bought or sold. Spot Price: is the current price at which a particular security can be bought or sold at a specified time and place. A security's spot price is regarded as the explicit value of the security at any given time in the marketplace. Western Texas Intermediate (WTI): is a type of crude oil used as a common benchmark in U.S. oil pricing. All indices are unmanaged. It is not possible to invest directly in an index.

©2015 Heartland Advisors

heartlandadvisors.com

2015528