Global CIO Commentary by Scott Minerd

Charles Dickens once advised: “Reflect upon your present blessings—of which every man has many—not on your past misfortunes, of which all men have some.” This is a wonderful mantra for life in general, but it specifically applies to the sentiment of many investors. It has been a tumultuous, difficult year for most benchmarks. It is certainly not the financial crisis, nor is it the bond market crash of 1994, or the credit crunch of 1989, but it has certainly been tough.

As the United States prepares for its Thanksgiving holiday (or what is now affectionately referred to as the day before Black Friday), there are reasons for tired and weary benchmark investors to be grateful. We are now in a season where past misfortunes are behind us and risk assets—particularly high-yield bonds and bank loans—are well positioned to enjoy a prosperous road ahead.

In the United States markets, my optimism draws from the fundamental strength of the U.S. economy, seasonal factors that continue to kick in support for equity prices, and my expectation that the holiday retail season will be a good one. Abroad, I believe investors should have more faith in the willingness and ability of central bankers to print money. In Europe and Japan, bad news is good news, and with any real signs of weakness I expect the policymakers will respond with further accommodation. In emerging markets, there remain plenty of headwinds and challenges, but valuations are such that opportunities for long-term investors are starting to look attractive, although it still may be too early for the faint of heart.

Going back to the strength of the U.S. economy, positive economic signals continue to outweigh negative ones. On the laundry list of recent positives, the consumer price index rose by 0.2 percent in October after two months of declines, and has begun to accelerate in year-over-year terms due to positive base effects. The Empire State Manufacturing Survey posted its strongest growth since July, and September job openings of 5.52 million beat expectations. Although October retail sales growth of just 0.1 percent was disappointing, consumer sentiment rebounded in October and November, and the outlook for consumer spending is bright. Historically, weak retail sales combined with strong job and wage growth results in a substantial pickup in economic growth in the ensuing six months.

Another economic positive is the weather. As the massive El Niño weather pattern gains strength, it should actually become a boon to the U.S. economy, potentially adding 1.5 percent to gross domestic product (GDP) in the first quarter. This is an intriguing and broadly overlooked fact that our Macroeconomic and Investment Research team has uncovered, but is not widely incorporated in economic forecasts.

Finally, we are now in the all-important retail holiday season, where approximately 20 percent of all retail sales occur. Higher equity prices tend to correlate with strong holiday retail sales, and the recent 10-plus percent rally in U.S. equity prices bodes well for fourth-quarter consumption. Add to that retailers’ eagerness to discount still-heavy inventories, and it seems that the holidays will be cheerful for the U.S. market.

All this positive data makes a December rate hike by the Federal Reserve virtually a foregone conclusion. Historically, the period when the Fed begins to tighten leads to an initial sell-off in the bond market as investors brace themselves for the ill-effects of restrictive monetary policy on the economy. Then as investors realize the Fed is raising rates because the economy is strong, the fear of defaults diminishes and credit spreads tighten again. If we consider the end of quantitative easing to be the beginning of Fed tightening, then the spread widening seen since October 2014 has now reached levels similar to the initial moves in previous tightening cycles. Even with a rate hike in December, the U.S. credit markets are predominately prepared, having already priced in a lot of bad news. Given the recent backup in spreads, I believe now is an opportune time to increase allocations to bank loans and high-yield bonds.

Turning to equities, in the United States, valuations are approaching highs not seen since the internet bubble, based on the historical relationship of total market cap to GDP relative to interest rates. But, I often remind people that valuation is a poor timing tool—just because as things get expensive doesn’t mean they won’t get more expensive. Meanwhile, equity valuations in Europe look reasonable, and valuations in certain emerging markets such as Brazil look downright cheap. I am not ready to declare the end of the bear market in emerging markets just yet because the growth in dollar-denominated private sector debt to GDP is nothing short of startling, and downward pressure on commodities and a rising dollar are significant headwinds. While the other shoe has still to drop, the good news is that emerging markets appear to be nearing a bottom, and valuations in some countries look attractive for long-term investors.

So even with the Fed’s first rate hike in seven years imminent, the tailwinds of positive economic data, accommodative global central banks, and positive seasonal forces are bolstering market resilience and reaffirming a positive environment backdrop for risk assets. I believe this environment will continue through the holidays and into the first quarter.

In the spirit of the upcoming holidays, I conclude by wishing everyone a wonderful Black Friday. But in all seriousness, when you step back and get a grasp of the bigger picture, we all have a lot to be grateful for. In the spirit of Thanksgiving, I am grateful to my Maker for all the many blessings and opportunities I have been afforded, and I want to wish everyone in the United States a very happy Thanksgiving holiday. I hope you and your loved ones enjoy a time of rest and reflection, celebrating your precious freedoms and giving thanks for the many blessings in your lives. To our clients around the world, may you know how grateful we are at Guggenheim for our relationship. It has been a tough environment, but another great year, thankfully. Thank you for the opportunity to continue to serve you with all the excellence, fidelity, and strength we can muster. It is a privilege to navigate the challenges of investing together. Happy Thanksgiving to all.

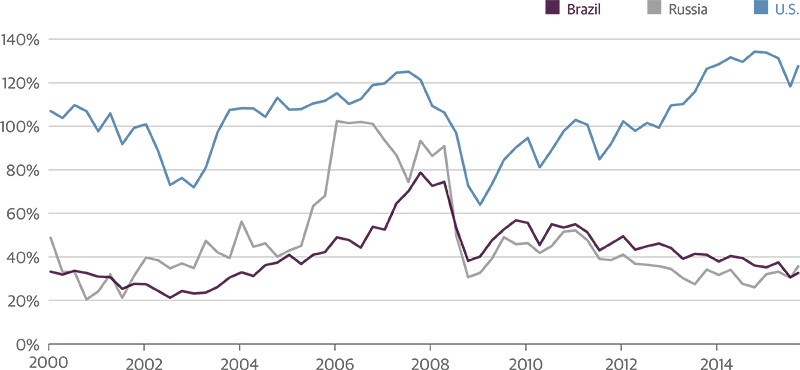

Emerging Market Valuations Look Attractive, but Risks Remain

While U.S. equities likely have near-term upside, the fact is that valuations are near historically rich levels. Meanwhile, after suffering a difficult several years of returns, emerging market equities are nearing attractive valuations that are hard to ignore. Though a variety of risks remain, including tighter Fed policy, further commodity price declines, and a significant debt buildup, long-term value-oriented investors should consider wading back into select emerging markets.

Market Capitalization, % of GDP*

Source: Bloomberg, Haver. Data as of 11/20/2015. *Note: market capitalization is measured against one year forward GDP.

Economic Data Releases

Leading Economic Index Strengthens as Housing Data Disappoints

- The Conference Board’s Leading Economic Index rose 0.6 percent in October. Stock prices, rate spreads and building permits all drove the increase.

- November’s preliminary U.S. manufacturing purchasing managers’ index came in at 52.6, the lowest level in 25 months.

- The November Empire Manufacturing Index inched up a reading of -10.7 from -11.4 in October. Economists had forecast a reading of -6.5.

- In the 12 months through October, the Consumer Price Index advanced 0.2 percent after being unchanged in September. Economists had forecast an increase of 0.1 percent.

- Existing home sales fell 3.4 percent to a 5.36 million rate in October. A 2.7 percent decline was expected.

- Housing starts fell to a seven-month low in October, declining 11 percent on the previous month.

- Building permits increased 4.1 percent to a 1.15 million-unit rate. Economists had forecast a 3.8 percent increase.

Euro Zone PMIs Indicate Fourth Quarter Pick-up

- A preliminary November reading showed a 54-month high in the Euro Zone Composite PMI index. The solid rise from 53.9 to 54.4 suggests that the region’s recovery may gain some pace in the fourth quarter.

- Germany’s ZEW index of current economic sentiment produced a reading of 54.4 for November from 55.2. The future expectations index rose to 10.4 from 1.9 in October.

- The European Commission’s flash estimate of November Euro Zone consumer sentiment was -6.0, a rise of 1.6 from a revised -7.6 in October.

- U.K. inflation remained below zero for a second consecutive month in October, extending the longest run of flat consumer prices in the modern U.K. era.

- U.K. retail sales declined at the fastest pace in a year in October, falling 0.9 percent month over month.

- Japanese exports were down 2.1 percent from a year ago, after rising half a percent in September. Economists had forecast a 2 percent decline.

Important Notices and Disclosures

This article is distributed for informational purposes only and should not be considered as investing advice or a recommendation of any particular security, strategy or investment product. This article contains opinions of the author but not necessarily those of Guggenheim Partners or its subsidiaries. The author’s opinions are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC. ©2015, Guggenheim Partners. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information.