Key Points

▪ Evidence suggests that the U.S. economy is strong enough that the Fed will raise rates later this month.

▪ Financial markets appear poised to undergo several important changes next year.

▪ There is a clear bearish case to be made, but we believe equities are more likely to advance than decline in the coming year.

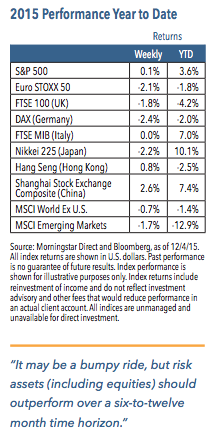

Equity markets were volatile last week, losing ground early before rebounding. Sentiment soured over a more modest easing announcement than expected by the European Central Bank (ECB). OPEC’s decision to leave oil production unchanged triggered a drop in energy prices, which also acted as a drag on equities. Additionally, a weak manufacturing report contributed to the gloomy tone. However, a strong jobs report on Friday seemed to pave the way for the Fed to raise rates this month and allowed equity prices to rally strongly. For the week, the S&P 500 Index was up 0.1%, with technology posting strong results and the energy sector lagging.1

Weekly Top Themes

1. The November jobs report provided further evidence that the U.S. economy is strong enough to bear higher rates. The data showed 211,000 new jobs were created last month.2 Although wage growth remains slow, we believe the Fed has enough information to make a rate increase later this month an easy decision.

2. U.S. manufacturing continues to lag the broader economic improvement. In November, the ISM Manufacturing Index came in at 48.6, significantly less than the six-month average of 51 and marking the first time in several years that the index fell below the break-even level of 50.3 It seems puzzling that manufacturing is weak when employment is growing, and we expect manufacturing will pick up in the coming year. But for now, it remains a decidedly weak spot.

3. The ECB extended its easing program, but less than expected. The central bank announced a six-month continuation of its quantitative easing program and cut the deposit rate by 10 basis points. Investors had been anticipating a more aggressive increase in the pace of purchases, as well as a deeper rate cut.

A Bullish Scenario Is More Likely than a Bearish One

Financial markets have been beset by an assortment of issues in 2015. The manufacturing sector slowed, Chinese growth weakened, commodity prices fell, deflation concerns persisted and geopolitical risks grew. Given this backdrop, it would hardly be surprising to see equities and other risk assets lagging, but they are not. There have been enough counterbalancing factors (including low inflation, decent U.S. economic growth and supportive monetary policy) to allow U.S. equity markets post modest gains so far this year.

But how long will this continue? We believe the investment landscape is poised to undergo significant changes next year. The effects of the long-term rise of the value of the U.S. dollar and corresponding decline in commodity prices should begin to fade. At the same time, headline inflation should begin to advance as the global economy gains some momentum. And, of course, the Federal Reserve is likely to be at the start of a tightening phase. Although we expect rate increases to be slow and modest, it is important to remember that it has been nearly a decade since the Fed raised rates. As such, it will likely take some time for investors to determine how to respond, which could contribute to volatility

Given these changes, it is fairly easy to make a bearish argument for U.S. equities: U.S. financial conditions are tightening and corporate profits are struggling. Many companies are starting to see lower levels of free cash flow, which could mean reduced corporate buybacks. And without repurchasing activity, higher revenues and sales would be required to produce earnings gains. Yet, the revenue outlook is troubled, thanks to the ongoing strength of the U.S. dollar.

We think this view is overly negative. The risks of a global recession appear low, and we think the world economy is more likely to accelerate rather than slow next year. The pockets of economic weakness that occurred in 2015 were concentrated in manufacturing and in emerging markets, which were linked with the collapse in oil prices. Our moderately constructive outlook is predicated on our expectations for a continued acceleration in U.S. growth, a recovery in the eurozone and stabilizing growth in China. We expect such an environment will mean increases in both equity prices and government bond yields. As such, we expect equities will outperform bonds over the next six to twelve months, although the ride is likely to be bumpy.

1 Source: Morningstar Direct, as of 12/4/15

2 Source: Bureau of Labor Statistics

3 Source: Institute of Supply Management

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

©2015 Nuveen Investments, Inc. All rights reserved.