At our most recent (fourth-quarter) Asset Allocation Committee meeting, perhaps the single most important issue we considered was whether the then-fresh decline of risk assets indicated a needed bull market correction, or something far more serious. Our analysis suggested short-term weakness, but for a while, the noise around China’s devaluation, Federal Reserve policy and concern about emerging markets and commodity prices had many investors very worried.

The beginning of the fourth quarter has seen a rebound in equities and corporate bonds, perhaps due in part to the sense that things were overdone, but also in light of soft data suggesting potential delay by the Fed in hiking rates, along with fresh easing in China and Mario Draghi’s statement reiterating the ECB’s commitment to bond purchases in Europe.

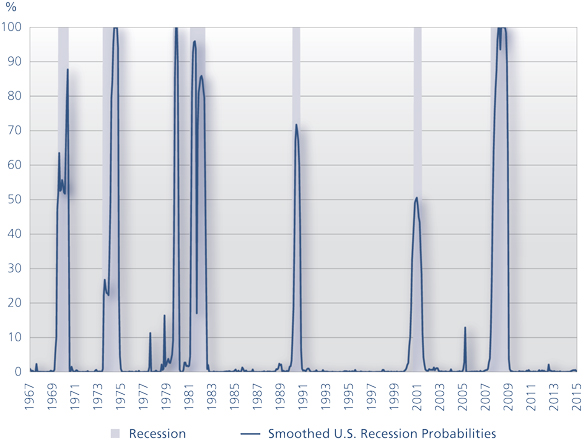

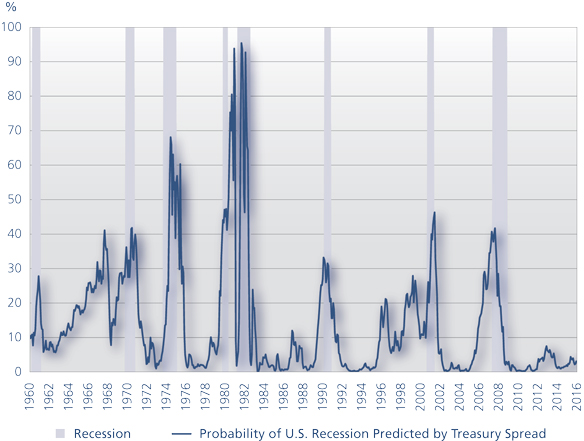

Where do we find ourselves, after some time for reflection? Essentially, in the same place: We still believe that growth trends are favorable enough to avoid recession in the developed markets and potentially lend support to equities for the next 12 months. Measures closely followed by the St. Louis Fed (combining four leading indicators) and the New York Fed (the shape of the Treasury yield curve) support our perspective.

Despite Market Volatility, U.S. Recession Seems a Distant Worry

Smoothed U.S. Recession Probabilities

Source: Federal Reserve Bank of St. Louis, as of September 30, 2015. Probabilities are obtained from a dynamic-factor Markov-switching model applied to four monthly coincident variables: non-farm payroll employment, the index of industrial production, real personal income excluding transfer payments, and real manufacturing and trade sales.

Probability of U.S. Recession Predicted by Treasury Spread

Source: Federal Reserve Bank of New York, as of September 30, 2015. This model uses the difference between 10-year and 3-month Treasury rates to calculate the probability of a recession in the United States 12 months ahead.

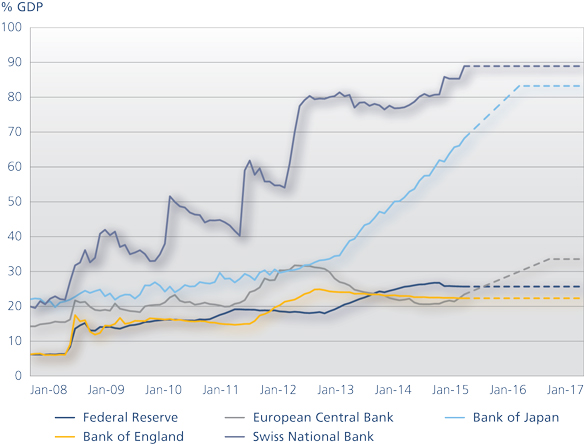

A key to this outlook is the behavior of central banks. Even as the Fed moves to tighten, we believe this will be a dovish tightening cycle, and that the overall monetary environment, powered by the ECB, Bank of Japan, Central Bank of China and others, will remain highly stimulated and encourage growth in the developed world. In our view, this has the potential to not only help extend the current business cycle in the U.S. but keep the budding European recovery intact.

Loose Policy Has Been a Key Support for Global Growth

Balance Sheets of the Major Central Banks

(Dotted lines represent NB forecasts)

Source: Bloomberg, Neuberger Berman calculations. Data as of September 30, 2015. Assumptions: Bank of Japan expands their balance sheet by JPY 80 trillion per annum until Japanese year-end 2015 (March 2016). ECB continues to expand their balance sheet by EUR 60 billion per month and reaches EUR 3 trillion in September 2016. Total balance sheet expansion is EUR 1,140 billion. The Federal Reserve, the Bank of England and the Swiss National bank do not wind down their balance sheets over the forecast horizon. Projected USD values assume unchanged exchanges rates against the U.S. dollar from the as-of date. Forecasts do not include GDP growth.

Importantly, this growth is coming without much inflation. Although there has been progress across the developed markets on unemployment, there remains little wage pressure, while low commodity prices have also been a factor. We do see some signs of a pickup but, in our view, the risk of elevated inflation seems extremely remote.

Positive Outlook for U.S. Equities

With this in mind, we continue to favor equities, particularly in the U.S., where the recovery has been accelerating. For the near term, the market may be hindered by reported earnings, which look to decline modestly year-over-year. However, the current consensus for 2016 is for close to 10% growth in S&P 500 earnings, aided by more stability in the energy sector and the reduced impact of dollar strength on earnings comparisons. In terms of debt, we believe that investors aren’t being sufficiently compensated to invest in government bonds but that the recent risk-off period has opened up opportunities in corporate credits. We are wary of emerging markets equity and debt given their sensitivity to Chinese growth, structural challenges and the impact of commodity weakness.

In terms of risks, China is front and center but, importantly, market concerns appear to be easing. China’s third-quarter GDP release, though viewed skeptically by many, still came in at a better-than-expected 6.9%. Moreover, even after six cuts to interest rates and four reductions in bank reserve requirements since November, the country has extensive policy options at its disposal that can potentially help soften its rocky transition to a more balanced economy. We will keep a close eye on real-time indicators such as purchasing manager indices to assess whether China—and the global economy more broadly—are becoming more stable. This could help extend the current economic cycle and contribute to a more benign backdrop for risk assets overall.

View the Asset Allocation Committee Report

This material is provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. This material is not intended as a formal research report and should not be relied upon as a basis for making an investment decision. The firm, its employees and advisory clients may hold positions of companies within sectors discussed. Specific securities identified and described do not represent all of the securities purchased, sold or recommended for advisory clients. It should not be assumed that any investments in securities identified and described were or will be profitable. Any views or opinions expressed may not reflect those of the firm as a whole. Information presented may include estimates, outlooks, projections and other “forward looking statements.” Due to a variety of factors, actual events may differ significantly from those presented. Neuberger Berman products and services may not be available in all jurisdictions or to all client types. Investing entails risks, including possible loss of principal. Investments in hedge funds and private equity are speculative and involve a higher degree of risk than more traditional investments. Investments in hedge funds and private equity are intended for sophisticated investors only. Unless otherwise indicated returns shown reflect reinvestment of dividends and distributions. Indexes are unmanaged and are not available for direct investment. Past performance is no guarantee of future results.

The views expressed herein may include those of those of Neuberger Berman’s Asset Allocation Committee which comprises professionals across multiple disciplines, including equity and fixed income strategists and portfolio managers. The Asset Allocation Committee reviews and sets long-term asset allocation models and establishes preferred near-term tactical asset class allocations. The views of the Asset Allocation Committee may not reflect the views of the firm as a whole and Neuberger Berman advisers and portfolio managers may recommend or take contrary positions to the views of the Asset Allocation Committee. The Asset Allocation Committee views do not constitute a prediction or projection of future events or future market behavior.

This material is being issued on a limited basis through various global subsidiaries and affiliates of Neuberger Berman Group LLC. Please visit www.nb.com/disclosure-global-communications for the specific entities and jurisdictional limitations and restrictions.

The “Neuberger Berman” name and logo are registered service marks of Neuberger Berman Group LLC.