The S&P 500 finished November largely unchanged, but not without oscillation along the way as markets absorbed information of higher-than-expected jobs data and its implications for a December rate hike.

INVESTORS TOOK NOVEMBER TO SURVEY THE LANDSCAPE AHEAD OF FED’S DECEMBER MEETING

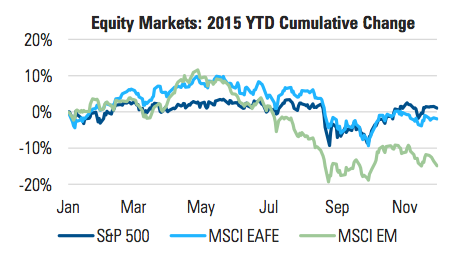

After rising 1.5% in the first two days of the month, the S&P 500 took a two-week tumble of more than 4% as strong employment data raised the prospects for the Fed to begin a long-anticipated tightening process:

Figure 1

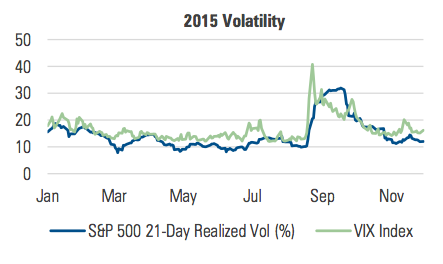

Volatility increased through mid-November only to revert back to levels at the start of the month. Implied volatility as measured by the VIX Index increased more than the realized volatility of the S&P 500:

Figure 2

MANAGED VOLATILITY PORTFOLIOS

During November, we estimate that a typical 80/20, globally- diversified, managed volatility growth portfolio saw its net equity exposure decline to 60% by mid-month before gradually reverting back to 80%. Market volatility increased moderately during the middle of the month, but was generally in line with the levels experienced throughout most of 2015.

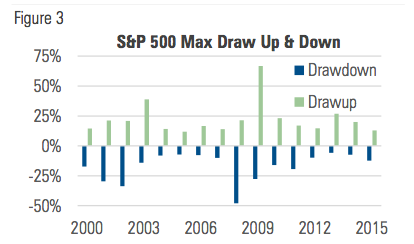

Within the financial industry, investors’ attention is often drawn to max drawdown, the largest decline in value over a given time period. Its inverse, max drawup, however, seems to get less attention. The fact that investors appear to be more interested in drawdown than drawup suggests an intuitive understanding about the importance of mitigating losses.

From 2000 – 2015, the average calendar year max drawup on the S&P 500 has been 22.2%, while the average max drawdown has been -17.1%. If an investor had been fortunate enough to capture only the drawups over the period, his investment would have grown by nearly 2500%. If an investor had been unlucky enough to capture only the drawdowns, he would be left with less than 5% of his starting investment.

In reality no investor captures solely just one or the other. The concept, however, helps to illuminate the devastating effects of compounded losses and by extension the importance of ongoing risk management.

MARKET COMMENTARY

After one of the stronger Octobers on recent record, equity markets paused to evaluate incoming economic data and its implications for monetary policy. During the first week of November, private and nonfarm payrolls came in 59% and 46% higher than expected, respectively. Markets sold off in response,

interpreting the data to mean a greater likelihood of a Fed rate hike at its December 16 meeting. Equities in the U.S. gradually reversed course and finished the month flat, while international markets finished the month lower:

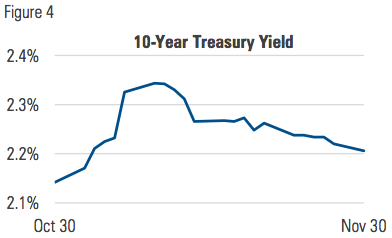

A relatively stable 10-year Treasury yield in October gave way to a sharp increase in November; likely also in anticipation of a Fed rate hike in December:

OIL STICKING BELOW $45/BARREL

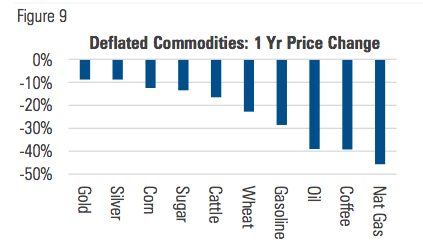

After breaking out above $50 in October, crude oil dropped below $42 by the end of November. There is currently no shortage of supply and that seems unlikely to change anytime soon. As the largest producer of oil in the Middle East, Saudi Arabia is thought to be maintaining high levels of production in order to preserve or even grow its market share by pushing out other producers, such as U.S. shale drillers who cannot bring oil to market as profitably at these lower prices.

Another less obvious (if not more interesting) theory is that Saudi Arabia is keeping prices low in an effort to thwart the ability of ISIS (which also follows Wahhabi Islam and may represent a political threat to the house of Saud) to finance itself through its newly acquired oil-rich territories in Iraq and Syria.

Whatever its motivation, in the absence of any changes to its own and the rest of OPEC’s production levels, endogenous supply constraints do not appear to be a likely catalyst for higher oil prices in the near term. This dynamic is keeping a lid on inflation.

FED SEEMS INTENT ON RAISING RATES. BUT WHY?

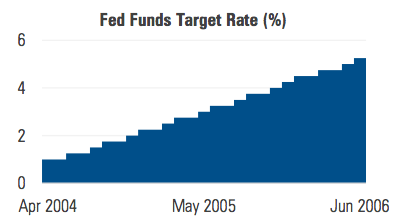

The last time the Fed changed its fed funds target rate was in December 2008, when it reduced it from 1% to 0%. The last time it raised the target rate was in June 2006, lifting it from 5% to 5.25%, marking the last of 17 consecutive 0.25% increases dating back to June 2004:

Figure 5

Today as the Fed again contemplates raising the target rate, it continues to articulate that any increases will be done at a gradual pace. The increases may not be as frequent as during the 2004-2006 cycle, but the increments could look similar. In some ways the build up to the December meeting feels a bit like 2004. In other important ways, however, it’s altogether different.

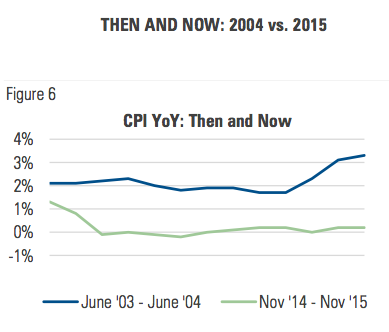

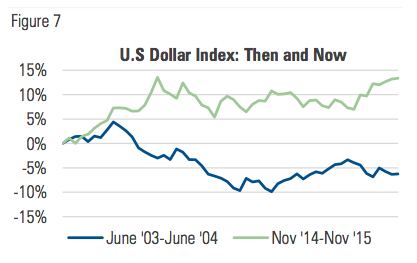

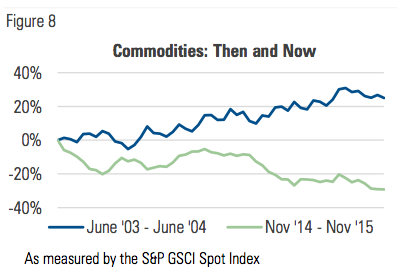

In the 12 months leading up to June 2004, the world economy grew by more than 3% and U.S economy expanded by 4.2%. Inflation in the U.S. had hovered around 2% and had begun to rise in the spring of 2004. The U.S. dollar index was down 6.3% and commodity prices were significantly higher.

Fast forward to 2015. Heading into December, U.S. GDP has grown by about 2%, even as growth in China and much of the rest of the global economy has declined. Inflation is non-existent, the U.S. dollar is sharply higher and commodity prices have fallen.

Figures 6, 7 and 8 compare inflation, the USD and commodity prices during the 12 months leading up to the first rate hike in June 2004 and the 12 months ended on November 30, 2015. The potential similarity of the Fed’s policy moves makes the contrast in the charts all the more striking:

It is against this backdrop that the eighth and final FOMC meeting of 2015 approaches.

TALKING ABOUT DOING IS NOT THE SAME AS DOING

There’s a quote that goes something like this: “Don’t tell me what you believe. Tell me what you do and I’ll tell you what you believe.” Not exactly the wisdom of the ages, but it does convey the basic truth that talking about doing something is indeed quite different from actually doing something.

Similarly, the Fed’s practice of talking about its mandate of seeking price stability is something quite different from actually using policy tools to foster price stability. Nevertheless, as its next meeting draws closer, the Fed seems intent on saying one thing and potentially doing another.

Without exception, the second paragraph of each of the seven FOMC statements in 2015 opens with the same boilerplate sentence:

“Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability.”

While there is still evidence of slack in the labor market, there is little question that the employment picture has improved markedly. But employment makes up just one (arguably less important) part of the Fed’s mandate.

With respect to the price-stability part of the mandate, it is hard to reconcile how a dollar-supporting rate increase can be deemed appropriate, when the dollar’s persistent strength has been such a significant contributor to lower prices. Prices are falling, but the Fed is talking about hiking. A strengthening dollar is arguably creating downside price instability, yet the Fed seems intent on throwing fuel on the fire.

In Europe, where inflation is similar to that in the US, the ECB is adding additional stimulus. Japan has had two consecutive quarters of negative real GDP growth and is showing no signs of becoming less accommodative. In Canada inflation is running at 1% and the probability of a near-term rate cut is higher than the probability of a rate hike.

OPEC appears to have no interest in making any meaningful cuts in production. Sanctions on Iran are scheduled to be lifted by the end of 2015, after which Iran is expected to begin injecting at least another 500k barrels/day into the market.

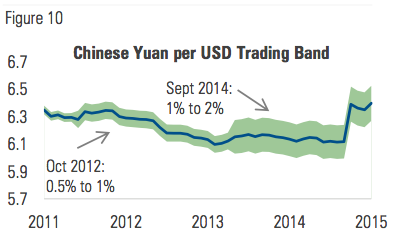

China may again widen the trading band around the yuan after its recent inclusion as an IMF reserve currency. This would further increase the potential for the yuan to weaken against the dollar, putting downward pressure on the price of Chinese imports:

Each of these items alone lends strength to the dollar. In combination with a Fed rate hike, they make up two sides of the same deflationary coin.

There is certainly more that could be said to make the case against raising the target rate in December. The point, however, is that the Fed’s insistence on carrying through with it in the face of so many seemingly opposing factors raises the specter of uncertainty. Moreover, the Fed will enter uncharted waters when it begins to raise the target rate while holding more than $2.5 trillion in excess reserves.

That backdrop of uncertainty contributes to the prospect for higher volatility as markets work to understand the implications. Accordingly, risk management remains a critical component to portfolio management in the weeks and months ahead.

Creating transformational improvement in the retirement savings industry.

Milliman Financial Risk Management LLC is a global leader in financial risk management to the retirement savings industry. Milliman Financial Risk Management (FRM) provides investment advisory, hedging, and consulting services on $190 billion in global assets (as of July 1, 2015).

Established in 1998, the practice includes over 130 professionals operating from three trading platforms around the world (Chicago, London, and Sydney). Milliman FRM is a subsidiary of Milliman, Inc.

Milliman, Inc. (Milliman) is one of the world’s largest independent actuarial and consulting firms. Founded in Seattle in 1947, Milliman has 55 offices in key locations worldwide that are home to over 2,600 professionals, including more than 1,300 qualified consultants and actuaries.

for more information:

MILLIMAN.COM/FRM

+1 855 645 5462

FOR INVESTMENT PROFESSIONAL USE ONLY

Recipients must make their own independent decisions regarding any strategies or securities or financial instruments mentioned herein.

The products or services described or referenced herein may not be suitable or appropriate for the recipient. Many of the products and services described or referenced herein involve significant risks, and the recipient should not make any decision or enter into any transaction unless the recipient has fully understood all such risks and has independently determined that such decisions or transactions are appropriate for the recipient.

Any discussion of risks contained herein with respect to any product or service should not be considered to be a disclosure of all risks or a complete discussion of the risks involved.

The recipient should not construe any of the material contained herein as investment, hedging, trading, legal, regulatory, tax, accounting or other advice. The recipient should not act on any information in this document without consulting its investment, hedging, trading, legal, regulatory, tax, accounting and other advisors.

The materials in this document represent the opinion of the authors and are not representative of the views of Milliman, Inc. Milliman does not certify the information, nor does it guarantee the accuracy and completeness of such information. Use of such information is voluntary and should not be relied upon unless an independent review of its accuracy and completeness has been performed. Materials may not be reproduced without the express consent of Milliman.

MIL_COM_1 12/15_12/16 © 2015 Milliman Financial Risk Management LLC