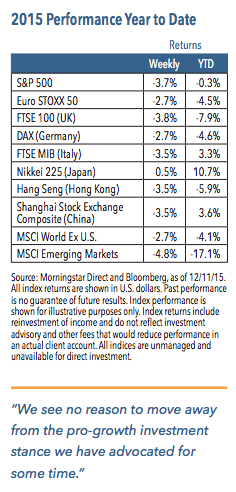

U.S. equities fell sharply last week, with the S&P 500 Index declining 3.7%.1 This was its largest loss since August and the second-largest downturn of the year.1 A sharp sell-off in oil prices was the main cause, along with credit and liquidity concerns within the high yield market. The energy sector was the worst performer last week and financials also took a hit.1 In contrast, more defensive areas such as utilities, consumer staples and health care held up better.1

Key Points

▪ The sharp drop in oil prices has roiled financial markets, but we do not expect to see widespread contagion.

▪ The Fed is on course to raise rates this week, and should emphasize that future increases will be gradual and measured.

▪ Investors will continue to face risks in the coming year, but we expect equity markets should weather any storms.

Weekly Top Themes

1. We expect the Federal Reserve will raise rates this week, but do not anticipate significant market reaction. At this point, it seems a foregone conclusion that the Fed will enact a 25 basis point rate increase, although we expect policymakers to stress that future increases will be gradual and measured. Over the next year, it seems reasonable to expect perhaps two additional rate increases.

2. Despite high-profile credit woes within the energy sector, we do not anticipate any sort of broad credit crisis. Last week’s move by Kinder Morgan (the country’s largest oil and gas pipeline operator) to cut its dividend by 75%2 alarmed investors and raised the question of whether this marks the start of credit contagion similar to what we saw during the subprime mortgage industry collapse. We doubt this will be the case. From what we are seeing, unlike the mortgage boom or previous energy booms, the banking system remains largely insulated from energy financing, which should help prevent contagion.

3. The collapse in commodity prices has both negative and positive effects. The near-term focus relates to questions over the strength of the global economy and on damage being done to commodity producers. Over time, however, lower prices should help commodity users and consumers, while controlling inflation and allowing central banks to stay accommodative.

4. Consumer spending levels should pick up. Strong jobs growth, an uptick in wages and low gasoline prices are a powerful combination that should promote increased spending. In particular, the drop in energy prices acts as a de-facto tax cut that should be particularly welcome to lower-income households.

5. Weak corporate profit margins may continue to drag on equities into next year. Companies have been struggling to improve profits and earnings in 2015, and this trend may persist. Falling unemployment and rising wages are putting a tremendous amount of pressure on companies, given that 60% of S&P 500 corporate costs are related to compensation.3 Absent a recession, we don’t expect margins to collapse, but they are likely to remain under pressure.

The Economy and Equity Markets Should Weather Risks that Lie Ahead in 2016

With good reason, investors are highly focused on this week’s Fed meeting. If the Fed doesn’t act, it would create widespread confusion and cause significant uncertainty. Some are arguing that the oil price collapse could spread into other asset classes (such as energy-related corporate bonds), which may give the Fed pause, but we don’t foresee a delay in action. When the Fed ended its quantitative easing program, there was little lasting market or economic impact. We expect the same after the Fed finally raises interest rates.

Regarding oil prices, volatility should continue, but we also think oil is in the midst of a bottoming process. There is clearly a supply glut, which will keep prices from rising significantly, but we also believe demand levels will increase given improving growth in the United States and a stabilizing economy in Europe. For the time being, oil prices are likely to remain range-bound.

Since the Great Recession ended, investors have seen a number of negative shocks. Although sentiment has remained depressed, the economy has accelerated and risk assets have remained resilient. We expect the coming year will bring more of the same. Issues such as falling oil prices, the strong U.S. dollar, weak manufacturing and a shift in Fed policy can all cause some angst, yet we believe factors such as the improving labor market and rising consumer spending levels should counterbalance the negatives. Additionally, even when the Fed starts raising rates, policy will remain equity-friendly. As such, we see no reason to move away from the pro-growth, pro-risk-asset investment stance we have advocated for some time.

1 Source: Morningstar Direct, as of 12/11/15

2 Source: Kinder Morgan 2016 Outlook

3 Source: Citi Research

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

©2015 Nuveen Investments, Inc. All rights reserved.