KEY TAKEAWAYS

· Widening high-yield bond spreads preceded the start of the stock market downturns in 2000 and 2008, causing many

to ask if the latest bout of high-yield weakness portends another downturn.

· While that is certainly possible, we see the odds as low, in large part because of the differences between the high-yield bond market and the stock market.

· We will continue to watch the high-yield market, oil, our favorite leading indicators, and corporate America for signs of a potential significant stock market downturn.

High-yield bond weakness has led investors to fear that a recession or bear market may be forthcoming. Widening of high-yield bond spreads (the spread between yields on high-yield bonds and comparable U.S. Treasuries) preceded the start of the stock market downturns in 2000 and 2008, causing many to ask if the latest bout of high-yield weakness portends another downturn. Here we try to answer that question by looking at characteristics unique to the high-yield bond market and prior periods of similar high-yield weakness.

HIGH-YIELD DISTINCTIONS

High-yield bonds had a difficult week, with the Barclays High Yield Bond Index losing 1.1% on Friday, December 11, 2015, bringing 2015 year-to-date losses for the index to 4.5%. That year-to-date loss compares to a 1.2% gain for the high-quality bond benchmark (Barclays Aggregate Bond Index), and the S&P 500’s marginal 0.3% loss. Last week’s volatility was driven by another leg down in oil, which tumbled 11% to below $36 per barrel, and news that a prominent high-yield strategy would block investors from pulling money out as it liquidates.

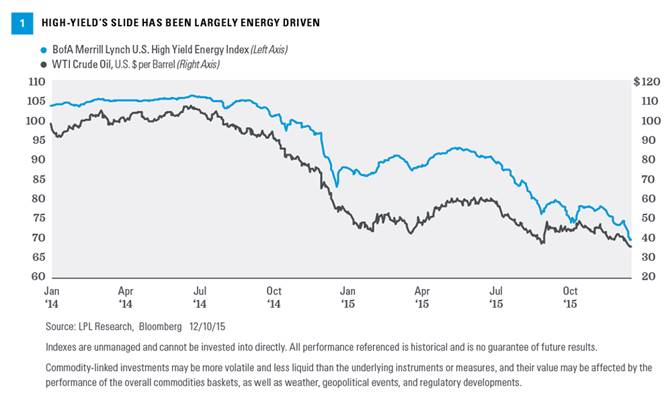

Some have suggested that this latest weakness in high-yield bonds is a sign that stocks may be on the verge of a bear market. While that is certainly possible, we see the odds as low, in large part because of the differences between the high-yield bond market and the stock market. For one, much of the deterioration in high-yield has been driven by the energy sector, which impacts high-yield more than the stock market. Energy as a percentage of the fixed income benchmark (Barclays Aggregate Bond Index) at roughly 15% is much higher than the energy sector’s weighting in the S&P 500 (6.6% as of December 10, 2015). High-yield spreads started to widen at the same time that oil prices began their sharp descent [Figure 1]. (See our Bond Market Perspectives, “High-Yield Oil Slick”.)

Because of its narrow focus, specialty sector investing, such as healthcare, financials, or energy, will be subject to greater volatility than investing more broadly across many sectors and companies.

Liquidity is another key difference between high-yield bonds and large cap stocks, like those found in the S&P 500 Index. In financial markets, prices are determined by the point at which buyers and sellers come together. Regardless of what fair value for an asset may be, if few (or no) buyers step up to buy in a market where many are headed for the exits, prices may overshoot to the downside. High-profile institutions halting redemptions to protect against selling at fire sale prices is a logical response to a wave of outflows in an illiquid market. Large cap stocks are far more liquid and are often the destination for funds seeking liquidity. Liquidity becomes an even bigger problem as the year-end holidays approach and market participants begin to close the books on the year.

Credit quality is another key difference between these two markets. The high-quality S&P 500 Index has an average credit rating of A, based on Moody’s ratings. The much lower-quality Barclays High Yield Index has an average rating of BB-/B+, seven to eight notches below the S&P 500. When credit conditions tighten up as they have recently, the turbulence is felt by high-yield issuers more acutely than the large cap stocks that make up the S&P 500.

A LOOK BACK AT PAST CYCLES

With that background, let’s look at whether high-yield weakness can provide a helpful signal of stock market downturns. Although there are not many cycles to analyze, given data on the high-yield bond market only goes back to the late 1980s, we believe a look back at history is instructive.

We analyzed credit spread data back to 1987 and the relationship with future stock market returns. Figure 2 shows this high-yield spread history charted against S&P 500 performance over the subsequent 12 months. You can see that there have only been two periods of credit weakness that preceded significant stock market losses, both corresponding with recessions (2000 – 02, 2008 – 09). Other periods of weakness, such as 1998 and 2011, turned out to be false alarms; and losses in 1990 turned out to be manageable, despite the recession that began that year and extended into early 1991.

We show seven unique periods of spread volatility in Figure 3, defined by spreads widening by more than one standard deviation* (approximately 150 basis points or 1.5%) over a trailing three-month period. Of these seven periods, only two preceded periods of significant market downturns:

*A measure of dispersion of a data series relative to its mean.

· Internet bubble (2000). In the three months ending November 2000, credit spreads widened by 247 basis points (2.47%) and remained volatile for nearly two years. The stock market sell-off extended well into 2002 amid the accounting scandals that followed the bursting of the internet bubble in 2000. Although high-yield did provide a warning in this instance, we do not see the excessive stock market valuations today that existed then, and accounting reliability has improved.

· Financial crisis (2008). A spike in credit spreads began with the three months ending July 2007, giving advance warning of the stock market peak in October 2007 and the eventual financial crisis. Spreads widened by 156 basis points (1.56%) during that period and remained volatile through the beginning of 2009. We do not see the type of housing speculation or widespread excessive borrowing today that would portend another financial crisis like this one.

Among the other five periods of spread volatility, the only instance when the S&P 500 fell over the following 12 months was November 1989 (-7%), a period following a string of Federal Reserve (Fed) rate hikes. The other periods proved to be good entry points for the stock market:

· October 1987. This period saw similarly depressed oil prices, but excessive leverage drove the stock market crash. Stocks recovered losses within a year and the bull market still had nearly three more years to go.

· September 1990. High-yield weakness in late 1990 coincided with the mild recession that began in July 1990 and lasted through March 1991 after the Gulf War had caused a jump in oil prices. Note that September 1990 turned out to be a great time to buy stocks ahead of a 26% gain in the S&P 500 in 1991.

· August 1998. Coinciding with the collapse of investment firm Long Term Capital Management due to excessive borrowing, this period also closely followed Asian and Russian financial crises and a period of sharp oil price declines. Stocks performed very well during this period marked by the technology boom, although the bull market peak was less than two years away at that point.

· August 2011. The European debt crisis and U.S. government debt downgrade drove weakness in high-yield bonds during this period. After nearly entering a bear market, stocks rallied 11% in the fourth quarter of 2011 and another 13% during 2012. Although this period was earlier in the business cycle, we believe the economy is generally in better shape now.

Bottom line, more of these periods of high-yield bond weakness ended up being buying opportunities for stocks rather than signals of a big sell-off. We believe today looks more like these benign periods than like 2000 or 2008.

WHAT WE ARE WATCHING

We will continue to watch the high-yield market closely, as well as oil, because of its impacts on the economy and markets. But we are watching many other factors to help give us some advance warning as to when a major stock market downturn may

be coming.

· Signs of excesses. Bear markets and recessions generally occur when excesses build up in the economy. Excess confidence drove the bear market in 2000, while excess borrowing was mostly to blame in 2008. We do not see excesses on this scale that would put the market at risk.

· Leading indicators. The Conference Board’s Leading Economic Index (LEI) is up 3.5% year over year based on the latest reading for November 2015, which has historically been consistent with a 10 – 15% chance of recession over the next 12 to 18 months. Although not all bear markets are associated with recessions, the large majority of them are.

· The yield curve. The yield curve, measured by the difference between short-term Treasury yields and intermediate-term Treasury yields, has historically been a good predictor of recessions and bear markets. The curve remains quite steep and is likely to remain steep even after the Fed starts to hike rates.

· Earnings momentum. We expect the pressures from falling oil prices and a strong U.S. dollar to abate next year, setting the stage for earnings growth to accelerate. The dip in the Institute for Supply Management (ISM) Manufacturing Index, one of our favorite earnings indicators, to below 50 — the breakpoint between expansion and contraction — has been driven largely by energy weakness and the strong dollar and is not atypical of the middle part of economic cycles.

· Corporate guidance. We will be listening closely to corporate management teams and what they have to say about the macro environment during the upcoming fourth quarter 2015 earnings season. We do not expect to hear widespread reports of companies pulling back that might suggest economic contraction.

CONCLUSION

We do not believe the latest sell-off in high-yield is a sign that a bear market is coming, but rather typical market volatility for this point in the economic cycle. The high-yield bond market is quite distinct from the stock market, as it is less liquid and more energy sensitive, and has a mixed record of anticipating stock market downturns. Higher volatility is normal for this point in the economic cycle. We will continue to watch the high-yield market, oil, our favorite leading indicators, and corporate America for signs of a potential significant stock market downturn.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values and yields will decline as interest rates rise, and bonds are subject to availability and change in price.

Government bonds and Treasury bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

High-yield/junk bonds are not investment-grade securities, involve substantial risks, and generally should be part of the diversified portfolio of sophisticated investors.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

All investing involves risk including loss of principal.

DEFINITIONS

Different agencies employ different rating scales for credit quality. Standard & Poor’s (S&P) and Fitch both use scales from AAA (highest) through AA, A, BBB, BB, B, CCC, CC, C to D (lowest). Moody’s uses a scale from Aaa (highest) through Aa, A, Baa, Ba, B, Caa, Ca to C (lowest).

The Leading Economic Indicators (LEI) Index is a measure of economic variables, such as private-sector wages, that tends to show the direction of future

economic activity.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Institute for Supply Management (ISM) Index is based on surveys of more than 300 manufacturing firms by the Institute of Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders, and supplier deliveries. A composite diffusion index is created that monitors conditions in national manufacturing based on the data from these surveys.

The Barclays U.S. Aggregate Bond Index is a broad-based flagship benchmark that measures the investment-grade, U.S. dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS, and CMBS (agency and non-agency).

The Barclays Capital High Yield Index covers the universe of publicly issued debt obligations rated below investment grade. Bonds must be rated below investment grade or high yield (Ba1/BB+ or lower), by at least two of the following ratings agencies: Moody’s, S&P, and Fitch. Bonds must also have at least one year to maturity, have at least $150 million in par value outstanding, and must be U.S. dollar denominated and nonconvertible. Bonds issued by countries designated as emerging markets are excluded.

The BofA Merrill Lynch High Yield Index tracks the performance of USD-denominated, below-investment-grade corporate debt publicly issued in the U.S. domestic market. Qualifying securities must have a below-investment-grade rating (based on an average of Moody’s, S&P, and Fitch), at least 18 months to final maturity at

the time of issuance, at least one year remaining term to final maturity as of the rebalancing date, a fixed coupon schedule, and a minimum amount outstanding of $100 million.

The BofA Merrill Lynch U.S. High Yield Energy Index is a subset of the BofA Merrill Lynch U.S. High Yield Index including all securities of energy issuers.