Labradoodles combine the friendly temperament of the Labrador retriever with the dander-free hair of a poodle—a win-win for dog-lovers who have allergies! Russell Investments sees multi-manager investing in a similar way. By combining skilled, often concentrated, managers, it is possible to capture the benefit of excess returns while reducing deviations from market returns that cause investors an allergic reaction.

Russell Investments’ Senior Portfolio Manager Jon Eggins, an aficionado of both labradoodles and multi-manager investing, shared in a recent blog how the popularity of active share1, a portfolio metric, has been misinterpreted in the context of multi-manager portfolios. Jon and I teamed up recently to demonstrate some of the properties of active share—and how lowering active share can be a positive thing. Here is our conversation:

Jon: So Leola, in the prior post I discussed the simple math of combining active manager: high + high = low. What happens to active share in multi-manager portfolios?

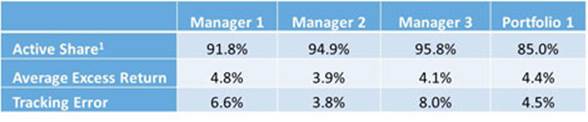

Leola: Let’s start with an illustrative example of three high active share global equity managers representative of our global equity manager universe as we look at performance from March 2009 to March 2015. In the table below, we show the average active share scores over the past 5 years, ranged from 91.8 to 95.8. These scores indicate the extent to which an active manager is different from its benchmark.

For illustrative purposes only. Not representative of an actual portfolio. Past performance is not indicative of future results. As measured against the MSCI World Index for benchmark purposes.

Now look at the active share for Portfolio 1, which is an equally weighted combination of all three managers. You will see that it is lower than all three managers separately, with a score at 85.0. Portfolio 1 active share is calculated at the security level, not a simple weighted average. For example, Manager 1 may have an overweight to a specific security while Manager 2 is underweight the same security, thereby negating any active share for that specific holding in Portfolio 1. This number illustrates how combining concentrated managers that diversify each other reduces active share1, 2 and this result a principal that is not tied to ups and downs of market performance.

Jon: Diversification is a good thing, but what about returns? What can active share help to tell us about returns?

Leola: In the same table we show strong excess returns (ranging from 3.9% to 4.8% over the MSCI World Index return) for Managers 1, 2 and 3. These managers also have high tracking errors, also defined as the volatility of excess returns over time.3 In this hypothetical example, when we put those three managers together in Portfolio 1, we retain the excess return level, 4.4% while tracking error, or the volatility of this excess return over time, declines dramatically. This reduction in tracking error is the direct result of diverse security selection processes among these managers.

Jon: And in this example, how did it look over each of those five years?

Leola: We show the cumulative total returns of the three managers, a composite of those three managers, as Portfolio 1, and the benchmark in the chart below. In this example, we observe that the three selected managers and Portfolio 1 had cumulative returns that were squarely above the benchmark and the margin above the benchmark grew over time. We also note that Portfolio 1 outperformed two of the three managers on a cumulative basis.

For illustrative purposes only. Not representative of an actual portfolio. Past performance is not indicative of future results. Source: Russell Investments as of December 2015.

Jon: Combining the table above with this chart, your analysis demonstrates that returns were not “diversified away” when combined into a composite portfolio, however the volatility was reduced. And how does this link back to active share?

Leola: As mentioned, the math of active share is that high + high = low. This math is the same as for other risk measures like tracking error. Yet, generally the math of returns is that high + high = high. That is to say, a manager returning 2% and a manager returning 3% when averaged in a portfolio will always result a combined return greater than one of the managers alone. By contrast, as active share demonstrates, multi-manager investing is something like the labradoodle—combining managers lowers active share but preserves the potential for excess returns.

Ultimately, like seeking out dog breeds that bring families all the benefits they desire, Russell Investments seeks out skilled active managers (see Jon’s recent post to learn more about what we mean when we talk about skilled active managers.). When we combine skilled managers, our goal is to retain excess return. In doing so we also seek to lower the volatility… and active share! Rather than being a negative, lower active share may actually be indicative of a well-diversified portfolio.

1 Active share, also known as active money and/or commonality, is defined as the proportion of stock holdings in a mutual fund’s composition that is different from the composition found in its benchmark. The greater the difference between the asset composition of the fund and its benchmark, the greater the active share. For example, a mutual fund with an active-share percentage of 75% indicates that 75% of its assets differ from its benchmark, while the remaining 25% mirror the benchmark. In this table, Active share is the average March 2009 to March 2015, quarterly data in this case measured against the MSCI World Index as a benchmark.

2 For multi-manager portfolios, the upper bound of active share is the average active share of underlying managers. If there are any diversifying bets in combined portfolios, the active share of the multi-manager portfolio will be lower than this average of underlying managers.

3 Tracking Error is the volatility of excess return over time.

Disclosures

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type.

The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional. The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

The MSCI World Index represents large and mid-cap equity performance across 23 developed markets countries, covering approximately 85% of the free float-adjusted market capitalization in each. This index offers a broad global equity benchmark, without emerging markets exposure.

Russell Investments is the owner of the trademarks, service marks and copyrights related to its indexes.

Russell Investments is a trade name and registered trademark of Frank Russell Company, a Washington USA corporation, which operates through subsidiaries worldwide and is a subsidiary of London Stock Exchange Group.

Copyright © Russell Investments 2016. All rights reserved.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

UNI – 10703