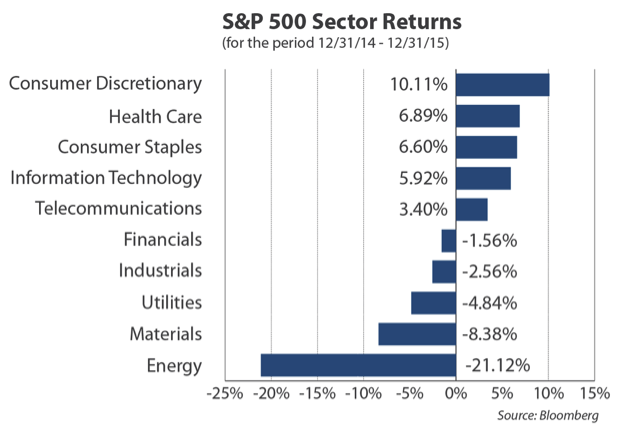

The Consumer Staples sector logged solid stock market performance in 2015, outpacing the S&P 500 Index. Intra-sector performance, however, varied widely, even among companies we might consider similar blue chips. Clorox enjoyed double-digit appreciation, while Procter & Gamble saw a double-digit share price decline, and Church & Dwight came in between the two. Changes to the market landscape are forcing Home and Personal Care companies to evaluate past practices and develop new strategies to address the evolution of consumer preferences and purchasing behavior.

At the risk of stating the painfully obvious, the internet factors dominantly in the changes taking place in Home and Personal Care and has dramatically affected the way consumers compare, shop for, and receive products. Perhaps the least appreciated of these is the last one — distribution. Of course, there's the ubiquitous brown cardboard box with the Amazon logo on the side, but most people receive only one-off items: a book, some electronic gear, a toy, etc. Recently we have entered an era in which direct-to-your-door distribution has widened to encompass more prosaic goods, such as pet food, razors, and toothbrushes, replenished on a regular delivery schedule. Before long many more of us may switch from retrieving our consumer staples products at the supermarket or big box store to receiving them at our homes. This has significant implications for the businesses of many old-line consumer blue chip companies. Let's examine the most successful example to date of a new distribution model establishing a beachhead on long protected shores: the razor.

For years disposable razor cartridges have been one of the great business success stories. We even speak of "The Razor Blade Model" as shorthand for a business that generates consistent sales and supernormal margins by supplying a consumable (cartridges) that the customer purchases because of sunk costs in a system (the razor handle). Constant "innovation" such as more blades, an aloe strip, vibration, etc., justifies the cartridge's steep price and leads to unique profitability. So valuable was the model that in 2005 Procter & Gamble paid $57 billion in stock to purchase Gillette. Today P&G's grooming division stands as its most profitable. A fundamental rule of capitalism proclaims that if you make a large enough profit on your business, eventually somebody will attack it. But, in this example, the attack couldn't come until the internet transformed consumer shopping habits, corporate marketing tactics, and distribution channels.

The attack arrived in 2012 with the launch of Dollar Shave Club (DSC). Today, DSC has over two million subscribers who purchase a razor handle and pay a modest monthly fee to receive a set of cartridges. DSC also provides shaving cream and other products. The razors are less complex than Gillette's, but they cost less. DSC never advertised during the Super Bowl or blitzed the airwaves during sweeps week, and you won't hear about it on drive time radio. Instead, DSC posted an entertaining YouTube ad that has pulled 21.5 million views. The products arrive at your door, so no more asking a sales associate at Walgreens to unlock the razor cabinet.

Meanwhile, another company has entered the fray. Harry's provides a slightly more upscale product, courtesy of the fact that the founders used part of their venture capital to buy a century-old razor blade factory in Germany. That makes the company unique in the industry as the only completely end-to-end supplier. At least it was until P&G finally realized what was happening and launched its own shave club, which isn't surprising considering that its grooming sales in the most recent quarter dropped -14%. In fact, P&G has now gone so far as to sue DSC for razor blade patent infringement. Suffice it to say "The Razor Blade Model" won't look the same going forward. Clearly DSC does not bear responsibility for P&G's quandary, but the fact remains that P&G's share price declined -12.82% in 2015. While those of us who have been paying egregious prices for razor blade cartridges may engage in a bit of schadenfreude at Gillette's expense, the key point is that the disruption could not have taken place absent a few technological and cultural shifts. DSC and Harry's needed a way to reach millions of consumers without spending much money (YouTube and website ads), an audience accustomed to ordering things online, and an inexpensive distribution system to get their products to customers cheaply and reliably (thanks to Amazon for forcing FedEx and UPS to invest).

If your product is used on a regular schedule and your customers are taken aback by its replacement cost, your profit is at risk.

Where might the new model strike next? Perhaps Quip has the answer; the question being, "Why did I pay $100 for an electric toothbrush and charger and then pay $30 for a set of two replacement toothbrush heads?" As with DSC, Quip offers a simplified product (electric toothbrush) and regular brush head replacements for a substantially lower price than one would typically find in Bed Bath & Beyond. Since Quip received its venture funding in early 2015, the company has yet to gain significant traction, but DSC's two million subscribers didn't arrive overnight either.

The message is clear: Companies that have enjoyed quasi-monopoly positions and supernormal profitability on daily use items should expect challenges, and successful challenges will affect the incumbent's sales, margins, and, for listed companies, share prices. If your product is used on a regular schedule and your customers are taken aback by its replacement cost, your profit is at risk.

Nor is this phenomenon restricted to the US, which we often think of as being at the forefront of the internet economy. Ever since the introduction of the iPhone, e-commerce has been migrating from the desktop to the palms of our hands through smartphones. In this instance, China leads the way. According to the US Census Bureau e-commerce accounted for 5.8% of total US retail sales in 2013, while the figure for China was 8.3%. Mobile or m-commerce alone held a 4.7% share in China in 2014. With less developed fixed-line, DSL, and cable infrastructure than in the US, Chinese consumers use their mobile devices as their primary source of internet access. As a result, e/m-commerce has boomed, and China has birthed such internet behemoths as search engine Baidu (market cap $68 billion), online gaming and instant messaging leader Tencent (market cap $182 billion), and online marketplace Alibaba (market cap $208 billion). Arguably, China's high population density will favor even more development of e-commerce and home delivery services for a wide variety of products.

In short, the internet not only offers a convenient way to seek out and review a wide variety of products, it presents a significant threat to traditional companies that fail to anticipate or adapt to its potential. The internet also offers a means for start-ups to inexpensively broadcast their message and contributes to the development of distribution models that make it economical to receive regular, small volume packages. If there's another message, it's that consumers appear to be getting really tired of paying $30 for a set of five razor cartridges or two toothbrush heads.

Security weightings are shown as a percentage of a Fund's total net assets. Amana Participation, Idaho Tax-Exempt, Saturna Sustainable Bond, Sextant Bond Income, Sextant Global High Income, Sextant International, and Sextant Short-Term Bond Funds did not own any securities of the companies mentioned.

Copyright 2015 Saturna Capital Corporation and/or its affiliates. All rights reserved. Vol. 9 · No. 7

Important Disclaimers and Disclosures

This report is intended only for the information of the reader and is not to be used for or considered as an offer or the solicitation of an offer to sell or buy any securities or other financial instruments of any kind, including without limitation, any mutual fund or other product offered, sponsored, created, or managed by Saturna Capital Corporation or its subsidiaries or affiliates ("Saturna"). This report is not intended for distribution to, or use by, any person or entity who is a citizen or resident of, or located in, any locality, state, country, or other jurisdiction in which such distribution, publication, availability, or use would be contrary to law or regulation or which would subject Saturna to any registration or licensing requirement within such jurisdiction.

This document should not be considered as providing investment advice or services, or any other service offered by Saturna. Saturna may not have taken any steps to ensure that the securities referred to in this report are suitable for any particular investor. Saturna will not treat recipients as its customers by virtue of their reading or receiving the report.

Nothing in this report constitutes investment, legal, accounting, or tax advice or a representation that any investment or strategy is suitable or appropriate to a particular investor's circumstances or otherwise constitutes a personal recommendation to any investor. Saturna does not offer advice on the tax consequences of any investment.

All material presented in this report, unless specifically indicated otherwise, is under copyright to Saturna. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied, or distributed to any other party without the prior express written permission of Saturna. Unless otherwise indicated, all trademarks, service marks, and logos used in this report are trademarks or service marks of Saturna.

The information in this report was obtained from sources Saturna believes to be reliable, and Saturna believes the information and opinions in the material are accurate and complete as of the date of this material. However, information and opinions contained herein will change over time and without notice. Saturna has no obligation to update or amend any information or opinions at any time. Saturna makes no representations as to the accuracy or completeness of this material, nor does it have any responsibility to ensure that any other materials, including any containing materially different information, are brought to the attention of any recipient of this report.

Under no circumstances shall Saturna, its employees, or any affiliate be responsible for any investment decision by any recipient. This material is distributed on condition that it will not form the sole basis or a sufficient basis for any investment decision by any recipient. Any recipient who is not a market professional or institutional investor should seek the advice of an independent financial adviser prior to making any investment based on this report or for any necessary explanation of its contents.

Saturna does not provide tax, legal, or accounting advice. Investors should consult their own tax, legal, and accounting advisers before engaging in any transaction. In compliance with IRS requirements, recipients are notified that any discussion of US federal tax issues contained or referred to herein is not intended or written to be used for the purpose of (A) avoiding penalties that may be imposed under the Internal Revenue Code; nor (B) promoting, marketing, or recommending to another party any transaction or matter discussed herein.

The S&P 500 is an index comprised of 500 widely held common stocks considered to be representative of the US stock market in general. Each sub sector index comprises only those stocks listed by S&P in that sector.

Past performance does not imply or guarantee future performance, and no representation or warranty, express or implied, is made regarding future performance. The price for, value of, and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of foreign securities and financial instruments is subject to exchange rate fluctuations that may have a positive or negative effect on the price or income of such securities or financial instruments. Investors in securities such as American Depositary Receipts — the values of which are influenced by currency volatility — effectively assume this risk.