In 2015, we saw significant bifurcation between the haves and have-nots (within asset classes, across asset classes and among economies), as well as high volatility. We expect bifurcation and volatility to remain dominant themes in 2016, making positioning especially important. The causes of investor apprehension have been well documented: global growth concerns, low commodity prices, sectarian turmoil in the Middle East, and of course, a lack of visibility surrounding the U.S. presidential election. Also, although the Fed has signaled plans for moderate rate tightening throughout 2016, the European Central Bank, the People’s Bank of China, and the Bank of Japan are more accommodative. This global central bank policy divergence is likely to contribute to market rotations throughout the year.

The year has gotten off to a rocky start, but we believe 2016 ultimately will prove to be a low-return environment. We expect elevated volatility as market participants grapple with a range of unknowns. While this isn’t a market we would choose, we are confident in the choices that we have made to navigate it, and we believe there are a range of opportunities across asset classes.

Outlook and Positioning

U.S Equities. While we do not believe a recession in the U.S. is imminent, U.S. economic growth will be slow in 2016, supported by favorable trends in employment, consumer confidence and housing. Although the recent budget deal marked a slight shift in a favorable direction, fiscal policy and political uncertainty remain formidable headwinds to more robust growth. Against this backdrop and in light of global growth concerns, the Fed may not carry through with as many rate increases in 2016 as it has indicated. At this point, we believe two increases in 2016 as being more probable than four. Additionally, our view is that long-term rates are unlikely to move significantly unless the economy accelerates in a meaningful way.

Source: Bloomberg

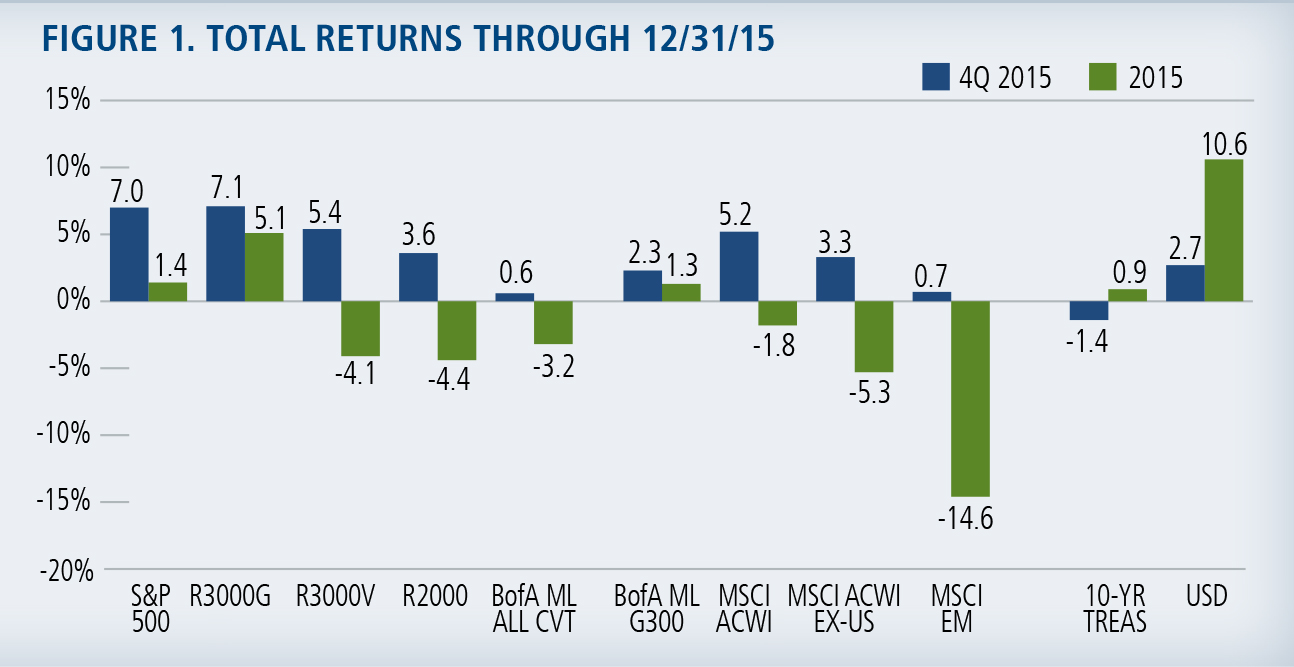

Market Review: Equity indexes rebounded in the fourth quarter but returns ranged from lackluster to disappointing for 2015 (Figure 1). Pulled up by a small group of stocks, the S&P 500 eked out a return of 1.4% on a market-cap weighted basis. On an equal-weighted basis, the index returned -2.2%. Growth outperformed value globally. Global convertibles advanced, but the U.S. convertible market ended the year down, due in large measure to the performance of mid-cap convertible issues during the third quarter (see our October outlook).

Past performance is no guarantee of future results.

Past performance is no guarantee of future results.

Past performance is no guarantee of future results.

Source: Empirical Research Partners Analysis.

1Excluding years with negative returns for the S&P 500

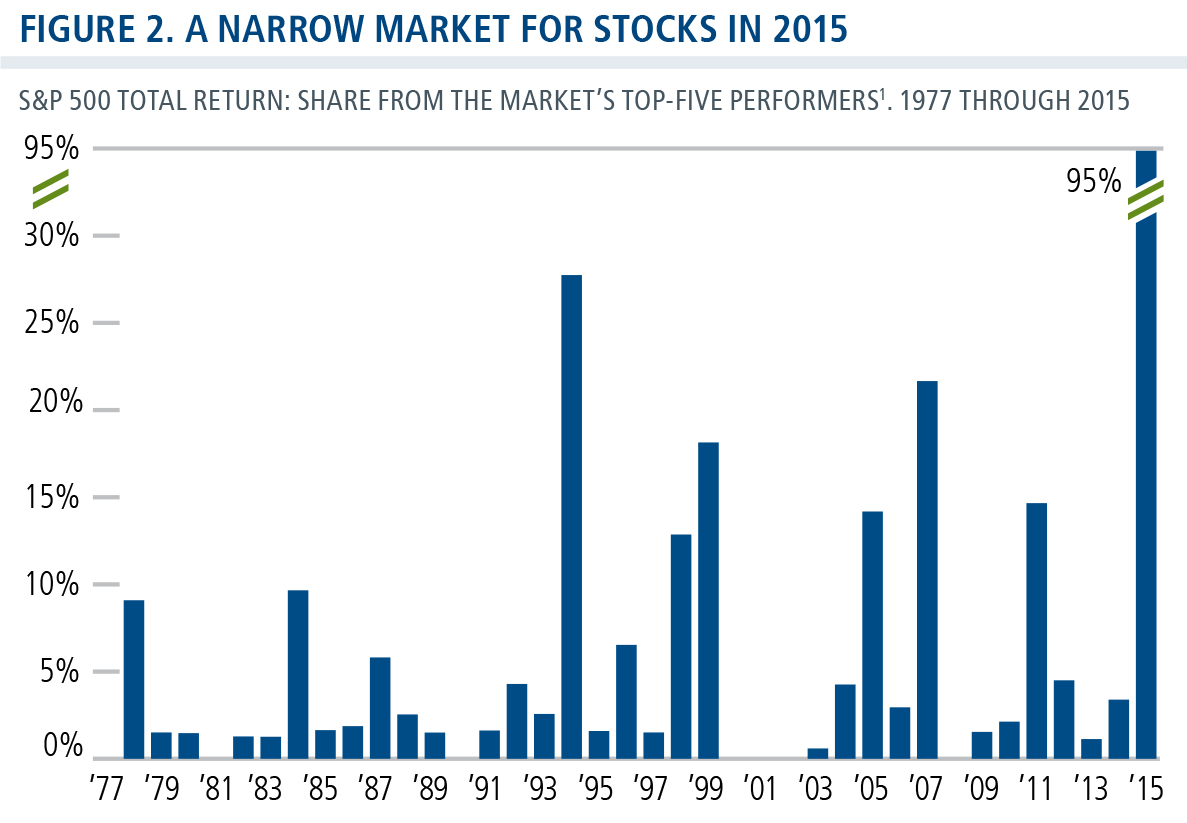

Our positioning in the U.S. equity market is cautious but not defensive. Although U.S. equity valuations are somewhat above average on the whole, the bifurcation in valuations is high and only a handful of names drove returns in the U.S. equity market in 2015. As Figure 2 shows, 95% of the S&P 500’s return was attributable to the top five performing names. Moreover, the elevated expectations we see in some areas of the market suggest a degree of complacency has set in. Because complacency typically gives way to volatility when negative news occurs, we are maintaining a cautious valuation approach. We are positioned to avoid the crowded trade, reducing exposure to valuation risk in favor of names that are not trading at extreme prices.

Given our outlook for muted growth, we are favoring quality growth names over cyclicals. We have sought to increase the balance sheet strength of the companies in which we are investing, continuing to seek out names with high returns on invested capital. From a thematic and sector perspective, we see opportunities in the technology sector, consumer companies tied to middle class spending, and companies positioned to benefit from improving fundamentals in Europe. We’re more cautious about companies that are vulnerable to regulatory headwinds (such as pharmaceuticals) and companies that are more exposed to the U.S. cap-ex cycle.

Emerging Markets. Although China’s recent manufacturing data and equity market turmoil have roiled the global markets, we believe a hard landing is unlikely. China has many tools at its disposal as it charts a multi-decade course to a more balanced economy. Over recent months, the government has announced fiscal measures to combat slowing growth but, as we have noted, these will take time to make their way through the economy. Within this context, the present weakness in manufacturing PMI is not entirely unexpected, while relatively stronger PMI for the services sector (still indicative of expansionary levels) and retail sales data support a more constructive longer-term outlook.

In regard to our positioning more broadly within the emerging markets, we remain extremely selective. Without a significant global cyclical pick-up and corresponding improvement in global trade, we expect many EMs will remain under pressure. However, there are still opportunities. From a top-down perspective, we are emphasizing countries that are net commodity importers, those that are pursuing economic reforms, and/or have stronger consumers, reduced current account deficits, and are benefiting from secular themes. Our most favored EM countries include the Philippines, India, Vietnam, Mexico and China. From a bottom-up perspective, we believe companies with strong balance sheets and high or accelerating return on invested capital (ROIC) are most likely to outperform in this environment.

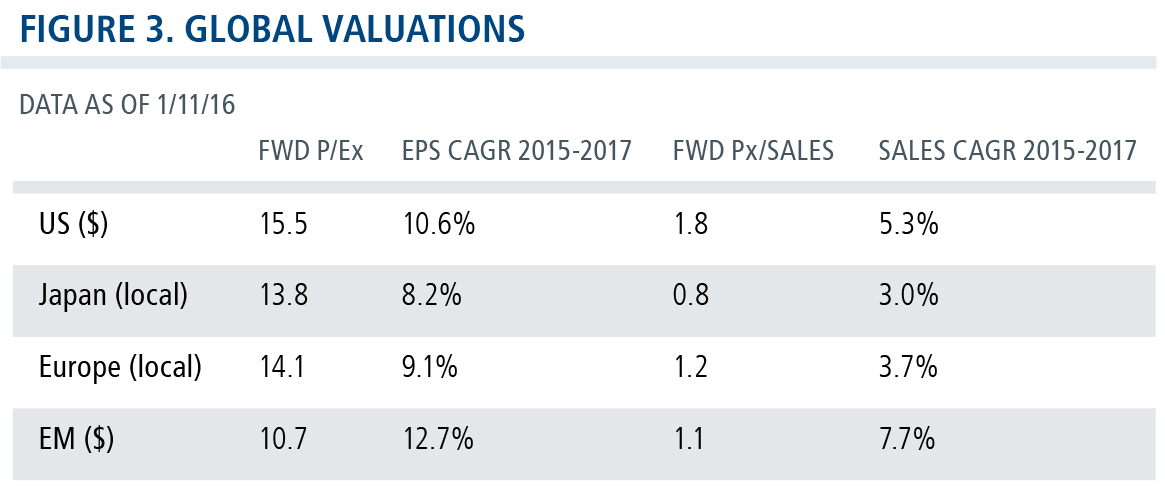

Europe and Japan. Our view on opportunities in Europe is positive, particularly as the European Central Bank looks set to take the baton from the Bank of Japan as the most accommodative central bank in the world. We are seeing strong momentum, resilient-to-improving economic fundamentals, as well as attractive valuations relative to other regions (Figure 3) and a positive liquidity environment. These factors, as well as a weakened euro and the ECB’s quantitative easing have led us to overweight Europe in our global and international strategies. We maintain a focus on growth-oriented companies, including beneficiaries of asset reflation and export opportunities afforded by a weaker euro.

While Japan’s economy remains lackluster, we continue to identify a number of bottom-up opportunities. Japanese valuations are not as compelling as they were a year ago, but given our expectation that we will see an improvement in ROIC for many companies we are investing in, we are finding better relative value. In many instances, this improvement is coming both from an improvement in margins and more efficient use of capital—both of which are creating intrinsic value for shareholders.

Convertible Securities. We are constructive on the convertible market as we enter 2016. Convertibles have historically performed well during rising rate regimes, and even if the Fed pursues rate increases at a more tempered pace, we anticipate a positive backdrop for the asset class. Our positioning reflects a growth bias, as we continue to emphasize opportunities within information technology, including cloud computing, data center disruption and consumer-related services. We also favor the consumer discretionary sector, including companies disrupting the traditional auto market and those positioned to benefit from a healthy U.S. consumer. We have become more selective within health care, particularly among companies that may be especially vulnerable to increasing regulatory and political pressures as the U.S. election nears. We are also highly cautious about cyclical sectors as fundamentals continue to weaken.

Source: Bloomberg

Similar to the broader equity markets, we see a bifurcation in the underlying convertible equity valuations with portions more richly valued than others. We are maintaining our focus on convertibles with more balanced equity and fixed income characteristics, given the high level of market volatility we anticipate. In regard to more credit sensitive structures, we are favoring higher quality balance sheets and/or companies that we believe are positioned to improve their credit profiles.

Globally, new issuance for 2015 was healthy, ending the year at just above $80 billion. Issues came to market with generally favorable terms and we saw strong representation from the technology and health care sectors. In the U.S., approximately half of the new issuance came in the form of mandatory convertible structures, which was higher than in the recent past. Because mandatory structures do not provide as much downside protection as traditional convertible bonds, we have been selective in our participation, particularly within cyclical sectors such as energy where fundamentals continue to weaken.

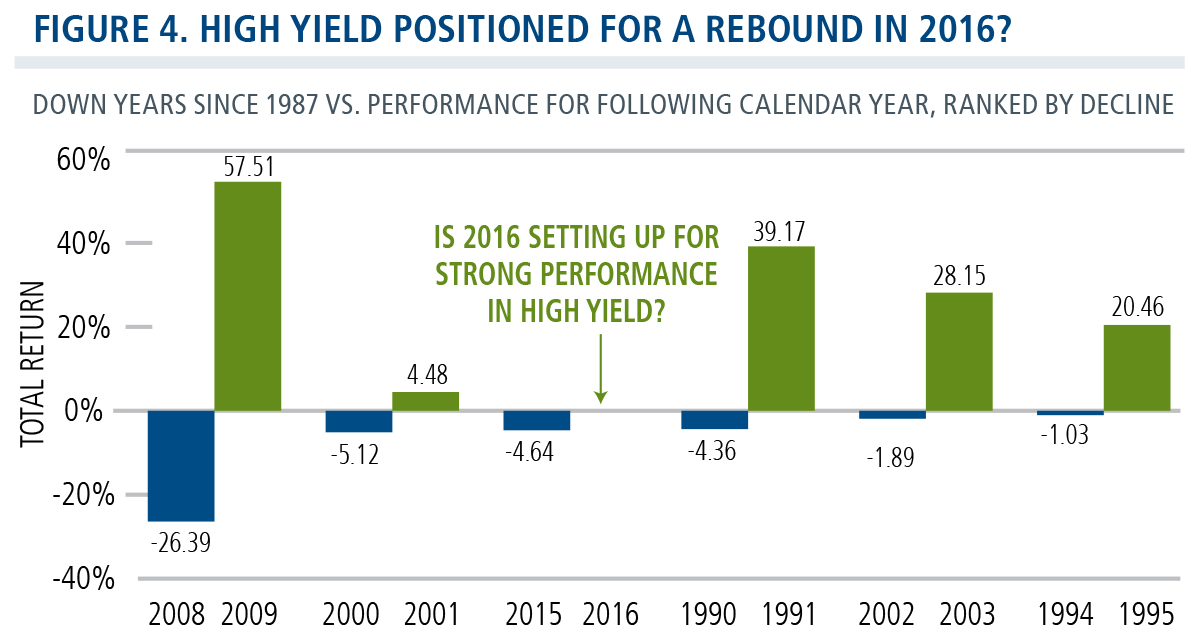

High Yield. Having benefited greatly from quantitative easing, the credit markets have faced formidable headwinds as monetary policy has become less accommodative. As the carry trade unwinds and market conditions normalize, high yield spreads have widened dramatically. We believe that absent a recession—which we don’t believe is imminent—the high yield market offers attractive value at current levels for risk-tolerant investors. While history does not always repeat, the high yield asset class has historically performed well during the years following its steepest declines (Figure 4).

Past performance is no guarantee of future results. High yield bonds are represented by BofA Merill Lynch U.S. High Yield Index. Performance shown since first full year since index inception.

Source: BofA Merrill Lynch and Bloomberg

Still, with defaults likely to rise (though remaining below long-term averages) and given the likely impact of low commodity prices on energy issuers, there will be winners and losers. In this environment, we have found opportunities to increase exposure to BB issues, while remaining selective regarding the most speculative credits. We are particularly focused on identifying “rising stars” (high yield issuers with the best potential for an upgrade to investment grade), given the significant spread compression that accompanies such moves. From a sector perspective, we have a more constructive outlook for services, consumer goods, autos and health care, while underweighting financials, media, telecommunication services, energy and commodities.

Lower-volatility equity and alternative strategies. We also believe that this is an environment where investors will be well served by maintaining sufficient diversification in their portfolios, including through less traditional approaches. Given the crosscurrents we see in the global market (equity market volatility, rising rates in the U.S., slow global growth), we believe the case is compelling for lower volatility equity strategies that combine equities and convertibles, as well as for select alternative strategies.

Conclusion

Many are likely to find this volatile environment frustrating and possibly even scary. However, having invested through volatile markets before, we encourage investors to resist the temptation to chase the herd or panic out of the market. We believe strongly both that there are opportunities in 2016 and also that we are positioned to capitalize upon them through a selective and research-driven approach.

JOHN P. CALAMOS, SR.

CEO and Global Co-CIO

INVESTMENT COMMITTEE CONTRIBUTORS

John Hillenbrand, CPA

Co-CIO and Senior Co-Portfolio Manager

David Kalis, CFA

Co-CIO and Senior Co-Portfolio Manager

Nick Niziolek, CFA

Co-CIO and Senior Co-Portfolio Manager

Eli Pars, CFA

Co-CIO and Senior Co-Portfolio Manager

Jeremy Hughes, CFA

SVP and Co-Portfolio Manager

Indexes are unmanaged, not available for direct investment and do not include fees and expenses. The U.S. Dollar Index measures the value of the U.S. dollar relative to a basket of foreign currencies, including Euro Area, Canada, Japan, United Kingdom, Switzerland, Australia, and Sweden. The S&P 500 Index is considered generally representative of the U.S. equity market. The MSCI All Country ex US Index represents the performance of global equities, excluding the U.S. The MSCI Emerging Markets Index is a measure of the performance of emerging market equities. The BofA Merrill Lynch U.S. High Yield Index is an unmanaged index of U.S. high yield debt securities. The BofA Merrill Lynch All U.S. Convertible Index (VXA0) is a measure of the U.S. convertible market. The BofA Merrill Lynch G300 Index measures the performance of 300 global convertibles. The Russell 3000 Growth Index and Russell 3000 Value Index are measures of the U.S. growth equity and value equity markets, respectively. The Russell 2000 Index measures U.S. small-cap stocks.

Purchasing Managers Index (PMI) measures the strength of the manufacturing sector. Earnings per share (EPS) is a company’s profit divided by its number of common outstanding shares. Price-to-earnings ratio (P/E) is a valuation ratio of a company’s current share price compared to its per-share earnings. Forward P/Es are based on forecasted earnings. Quantitative easing refers to central bank bond buying activities. ROIC (return on invested capital) measures how effectively a company uses the money invested in its operations, calculated as a company’s net income minus any dividends divided by the company’s total capital. This material is distributed for informational purposes only. The information contained herein is based on internal research derived from various sources and does not purport to be statements of all material facts relating to the information mentioned, and while not guaranteed as to the accuracy or completeness, has been obtained from sources we believe to be reliable.

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be suitable for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

OUTLKCOM 18142 0116OC